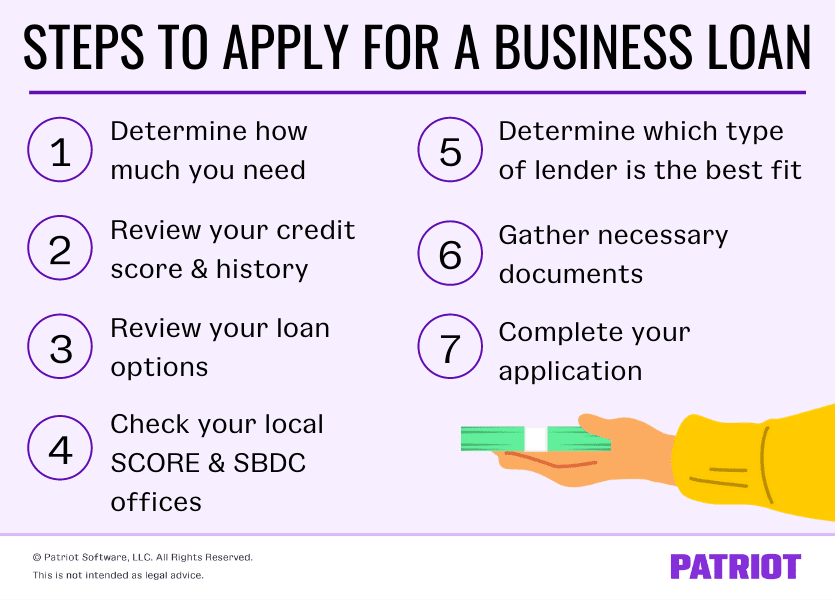

Securing a business loan can be a pivotal moment for any enterprise, whether it’s a fledgling startup seeking seed capital or an established firm looking to expand. The capital infusion can fuel growth, facilitate inventory purchases, fund marketing campaigns, or even provide crucial working capital to navigate lean periods. However, the path to obtaining a business loan is paved with requirements and scrutiny. Lenders, naturally risk-averse, want assurance that their investment will be repaid. Understanding precisely what they need from you is the first and most critical step towards a successful application. This guide will walk you through the essential components, documents, and considerations necessary to prepare a compelling case for financing.

Understanding the Business Loan Landscape

Before diving into the specifics of what you need, it’s beneficial to grasp the broader context of business lending. Knowing why lenders lend, what types of loans exist, and what their general expectations are will help you tailor your application effectively.

Why Businesses Seek Loans

Businesses pursue loans for a myriad of reasons, each dictating a different type of financing and requiring specific documentation. Common reasons include:

- Startup Costs: Covering initial expenses like equipment, rent, and legal fees for new ventures.

- Expansion: Funding new locations, increased production capacity, or market penetration.

- Working Capital: Bridging gaps in cash flow, covering operational expenses, or managing seasonal fluctuations.

- Equipment Purchase: Acquiring machinery, vehicles, or technology essential for operations.

- Inventory Financing: Purchasing goods for resale, especially for retail or manufacturing businesses.

- Debt Refinancing: Consolidating existing high-interest debts into a more manageable loan.

Each of these objectives will influence the type of loan you seek (e.g., term loan, line of credit, equipment financing) and, consequently, the specific information lenders will prioritize.

Types of Business Loans Available

The market offers a diverse array of business loan products, each designed for different purposes and business profiles. Understanding these can help you identify the best fit for your needs:

- Term Loans: A lump sum of money repaid over a fixed period with interest, suitable for large, one-time investments like equipment or expansion.

- Lines of Credit: Flexible financing that allows businesses to draw funds as needed, up to a certain limit, ideal for managing working capital fluctuations.

- SBA Loans (Small Business Administration): Government-backed loans offered through banks, often featuring lower down payments, flexible overhead requirements, and longer repayment terms, making them popular for small businesses.

- Equipment Financing: Loans specifically for purchasing new or used equipment, often with the equipment itself serving as collateral.

- Invoice Factoring/Financing: Selling your accounts receivable (invoices) to a third party at a discount to get immediate cash.

- Merchant Cash Advances: A lump sum payment exchanged for a percentage of future credit card sales. While quick, they often come with high effective interest rates.

- Commercial Real Estate Loans: Used to purchase, refinance, or develop commercial properties.

The type of loan you apply for will directly influence the lender’s specific document requests, as their risk assessment will be tailored to the nature of the financing.

Lender Expectations: A General Overview

Regardless of the loan type, lenders typically evaluate businesses based on what are often referred to as the “5 Cs of Credit”:

- Character: Your trustworthiness and reputation, often assessed through your credit history and business experience.

- Capacity: Your ability to repay the loan, demonstrated by your cash flow and financial statements.

- Capital: Your personal investment in the business, indicating your commitment and mitigating risk.

- Collateral: Assets you can pledge to secure the loan, providing the lender with recourse if you default.

- Conditions: The economic climate, industry trends, and the specific purpose of the loan, which can influence the risk profile.

Understanding these criteria is paramount, as every document you submit and every piece of information you provide should aim to positively address these five areas.

Essential Documents: The Financial Blueprint

The bedrock of any business loan application is a comprehensive set of financial documents. These provide lenders with a clear, objective picture of your business’s health, performance, and ability to repay the loan.

Business Plan: Your Roadmap to Success

While not strictly a financial document, a well-crafted business plan is indispensable. It articulates your vision, strategy, and operational details, convincing lenders that you have a viable business model and a clear path to profitability.

- Executive Summary: A concise overview of your business, its mission, products/services, market, and financial projections.

- Company Description: Details about your legal structure, history, and goals.

- Market Analysis: Research on your target market, industry trends, competition, and how your business fits in.

- Organization & Management: Information on your team, organizational structure, and key personnel.

- Service or Product Line: Detailed descriptions of what you offer and your unique selling proposition.

- Marketing & Sales Strategy: How you plan to attract and retain customers.

- Funding Request: A clear statement of how much money you need, how you’ll use it, and how it will contribute to profitability.

- Financial Projections: The most crucial section for lenders, including detailed forecasts.

Financial Statements: A Look Under the Hood

These are arguably the most critical documents, providing a historical and projected view of your business’s financial performance. For existing businesses, lenders will typically request statements from the last 2-3 years, plus year-to-date figures. Startups will need robust projections.

- Profit & Loss Statement (Income Statement): Shows your revenues, costs, and profits (or losses) over a period (e.g., a quarter or a year). It demonstrates your operational efficiency and profitability.

- Balance Sheet: A snapshot of your business’s financial health at a specific point in time, detailing assets (what you own), liabilities (what you owe), and equity (the owner’s stake). It reveals your company’s net worth and liquidity.

- Cash Flow Statement: Tracks the movement of cash into and out of your business over a period. This is vital because a profitable business can still run out of cash. Lenders look for consistent positive cash flow to ensure repayment capacity.

- Accounts Receivable/Payable Aging Reports: These reports provide details on money owed to your business and money your business owes to others, indicating liquidity and management effectiveness.

Bank Statements: Demonstrating Financial Health

Lenders will typically request the last 6-12 months of your business bank statements. These provide an unvarnished view of your cash flow, transaction history, and how you manage your operational funds. They confirm the financial figures presented in your formal statements and reveal any red flags like frequent overdrafts or inconsistent deposits.

Tax Returns: Verifying Financial Claims

Both business and personal tax returns (for the last 2-3 years) are essential.

- Business Tax Returns: Provide verifiable financial data that has been reported to the government. Lenders use these to cross-reference with your financial statements and ensure consistency.

- Personal Tax Returns: Especially for small business owners, personal tax returns are crucial as they show your individual financial situation, which often intertwines with the business, particularly for sole proprietorships or partnerships. They demonstrate your personal financial stability and capacity to support the business if needed.

The Business and Personal Profile

Beyond the numbers, lenders want to understand the entity they are lending to – both the business itself and the individuals behind it. This section covers legal documentation and personal financial commitments.

Business Legal Documents: Establishing Legitimacy

These documents confirm your business’s legal standing and operational authority.

- Business Registration & Licenses: Proof that your business is legally registered with the relevant authorities (state, county, city) and possesses all necessary operational licenses and permits.

- Articles of Incorporation/Organization: For corporations and LLCs, these documents outline the fundamental details of your business’s formation, structure, and initial directors/members.

- Employer Identification Number (EIN): Your business’s federal tax ID number, akin to a Social Security number for an individual.

- Operating Agreement (LLC) or Bylaws (Corporation): Internal documents detailing the ownership structure, management responsibilities, and decision-making processes.

- Commercial Leases/Deeds: Documentation for your business premises, whether owned or leased.

- Contracts & Agreements: Any significant contracts with suppliers, customers, or key employees that impact your business operations or financial outlook.

Personal Financial Information: Your Stake in the Game

For most small and medium-sized businesses, the owner’s personal financial health is inextricably linked to the business’s perceived risk.

- Personal Financial Statement: A comprehensive overview of your personal assets (e.g., real estate, investments, savings) and liabilities (e.g., mortgages, personal loans, credit card debt). This shows your net worth and ability to withstand financial shocks.

- Personal Tax Returns: As mentioned, these provide a verifiable history of your personal income and financial obligations, demonstrating your capacity to contribute to or support the business if needed.

- Credit Reports (Business & Personal): Lenders will pull both.

- Personal Credit Score: A high personal credit score (typically 680+) indicates a history of responsible financial behavior, which lenders often extrapolate to your business dealings.

- Business Credit Score: If your business has been operational for some time and has established credit, this score (e.g., from Dun & Bradstreet, Experian Business, Equifax Business) will reflect its payment history with vendors and lenders. A strong business credit profile is crucial for larger loans and better terms.

Collateral and Guarantees: Mitigating Lender Risk

Especially for larger loans or businesses perceived as higher risk, collateral and personal guarantees are often required to reduce the lender’s exposure.

- Types of Collateral: Assets pledged to secure the loan. If you default, the lender has the right to seize these assets. Common forms include:

- Real Estate (commercial or personal)

- Accounts Receivable

- Inventory

- Equipment

- Vehicles

- Savings Accounts/CDs

- Providing documentation of ownership and valuation for any proposed collateral is essential.

- Personal Guarantees: A promise from the business owner(s) to personally repay the business debt if the business defaults. This means your personal assets are at risk. Most small business loans, particularly SBA loans, require a personal guarantee from all owners with a significant stake in the company.

Crafting a Compelling Loan Application

Gathering the documents is one thing; presenting them in a clear, coherent, and persuasive manner is another. The way you package your application can significantly influence a lender’s decision.

The Importance of a Strong Narrative

Your application isn’t just a collection of papers; it’s a story about your business. Ensure that your business plan, financial projections, and accompanying cover letter tell a consistent, optimistic yet realistic story. Highlight your business’s strengths, competitive advantages, and how the loan will specifically contribute to its success and your ability to repay.

Due Diligence and Preparation

Start the process well in advance. Gathering all necessary documents, especially historical financial statements and tax returns, can take time. Ensure all information is accurate, up-to-date, and consistently presented across different documents. Discrepancies can raise red flags. Be proactive in asking your accountant for assistance in preparing professional-grade financial statements.

Professional Presentation

Organize your documents neatly, perhaps in a binder with clear tabs or as well-named digital files. A professional and organized presentation reflects positively on your business acumen and attention to detail. Prepare an executive summary or cover letter that succinctly outlines your request, the loan’s purpose, and why your business is a strong candidate for financing.

Post-Application: What to Expect and How to Maximize Your Chances

Submitting your application is just the beginning. The subsequent phase involves lender review and potential follow-up.

The Lender’s Review Process

Once submitted, your application will undergo thorough scrutiny. Lenders’ underwriters will meticulously review all provided documents, perform due diligence, conduct background checks, and assess the risk profile. This process can take anywhere from a few days for smaller online loans to several weeks or even months for larger, more complex traditional bank loans (like SBA loans).

Addressing Inquiries and Providing Additional Information

It’s common for lenders to have follow-up questions or request additional documentation. Respond promptly, thoroughly, and transparently. This demonstrates your professionalism and commitment. Be prepared to explain any anomalies in your financial statements or business plan.

Strategies for Loan Approval

To maximize your chances of approval:

- Build a Strong Relationship: If possible, establish a relationship with a business banker before you need a loan. They can offer guidance and insights.

- Know Your Numbers: Be intimately familiar with your financial statements, projections, and key performance indicators.

- Understand Your Credit: Check your personal and business credit scores well in advance and take steps to improve them if necessary.

- Be Realistic: Request a loan amount that is genuinely needed and justifiable by your business’s projected cash flow.

- Practice Your Pitch: Be ready to articulate your business case clearly and concisely to the lender.

In conclusion, securing a business loan is a rigorous process that demands meticulous preparation and a comprehensive understanding of lender expectations. By diligently gathering and presenting a complete set of financial, legal, and personal documents, coupled with a compelling business narrative, you significantly enhance your prospects of obtaining the capital needed to propel your business forward. It’s an investment in your future, and preparing thoroughly for it is the first step towards a successful outcome.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.