Navigating the landscape of homeownership can be an exciting yet complex journey, particularly when seeking financing options that cater to a specific demographic. The U.S. Department of Agriculture (USDA) Rural Development program offers a valuable pathway to homeownership for individuals and families in eligible rural and suburban areas, often with attractive benefits like zero down payment options. However, not every property qualifies for this specialized loan. Understanding the criteria that can disqualify a home is crucial for potential buyers to avoid disappointment and wasted effort. This article will delve into the key factors that determine a home’s eligibility for USDA financing, ensuring you are well-informed throughout your home-buying process.

Understanding USDA Loan Eligibility: Beyond Borrower Creditworthiness

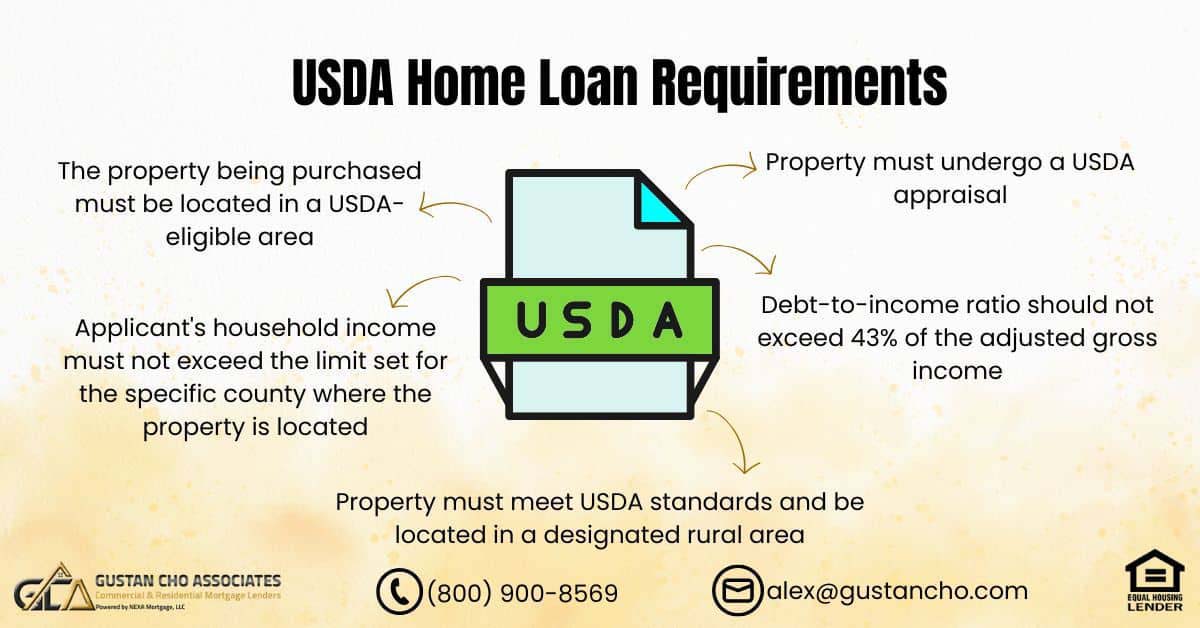

While a borrower’s financial health, including credit score, income, and debt-to-income ratio, is paramount for any loan approval, USDA financing extends its scrutiny to the property itself. The program is designed to promote development and stability in rural communities, and as such, the properties financed must align with this objective. This means that the physical condition, location, and intended use of the home are all subject to USDA guidelines. Ignoring these property-specific requirements can lead to a loan denial, even if the borrower is otherwise a strong candidate.

Location, Location, Location: The USDA’s Definition of Rural

The most fundamental requirement for USDA financing is that the property must be located in an eligible rural or suburban area. The USDA has a specific definition of what constitutes “rural” for its loan programs. This definition is not static and is based on population density and proximity to urban centers.

Eligible Geographic Areas

The USDA maintains an interactive map on its website where prospective borrowers and agents can verify the eligibility of a specific address. Generally, areas with populations under 35,000 are often considered eligible, but there are nuances. Some larger towns and cities may have specific zones within them that are deemed eligible, while smaller, more isolated areas might be excluded if they don’t fit the program’s broader development goals. It is imperative to use the official USDA eligibility tool to confirm a property’s location. Relying on assumptions or outdated information can be a significant misstep.

Properties in Urban Centers

Properties situated within densely populated urban centers or their immediate, highly developed suburbs are typically disqualified. The USDA’s mission is to foster growth in less populated regions, and therefore, financing for homes in major metropolitan areas is not permitted under this program. This includes the core areas of large cities and their surrounding, well-established commuter towns.

Property Type and Condition: Ensuring Livability and Durability

Beyond location, the physical characteristics and condition of the home play a significant role in its eligibility for USDA financing. The loan is intended for habitable, primary residences, and the property must meet certain standards to ensure its safety, soundness, and suitability for long-term occupancy.

Primary Residence Requirement

USDA loans are strictly for primary residences. This means the borrower must intend to occupy the home as their main dwelling. Properties intended for investment, vacation homes, or rental purposes are not eligible for USDA financing. The loan is designed to support individual and family homeownership, not to facilitate real estate investment portfolios.

Minimum Property Requirements (MPRs)

The USDA has established Minimum Property Requirements (MPRs) that all financed homes must meet. These MPRs are designed to ensure the property is safe, sanitary, and structurally sound. Key areas of concern include:

- Structural Integrity: The home must have a sound foundation, walls, and roof. Any significant structural defects, such as sagging floors, major cracks in the foundation, or a deteriorating roof, will likely disqualify the property. The appraiser will assess these elements carefully.

- Plumbing and Electrical Systems: The plumbing and electrical systems must be in good working order and meet current safety codes. Issues like faulty wiring, outdated fuse boxes, or leaking pipes can lead to disqualification.

- Sanitary Conditions: The property must be free from hazards that could compromise the health and safety of its occupants. This includes issues like mold, pest infestations, or inadequate waste disposal systems. Septic systems and wells, if present, will also be inspected to ensure they are functioning properly.

- Adequate Heating and Cooling: The home must have a functional heating system adequate for the climate. While central air conditioning is not always mandatory, the property must be generally habitable and provide a reasonable level of comfort.

- Access and Utilities: The property must have safe and reliable access, typically via a paved or graveled road that is maintained by a public entity. Essential utilities, such as electricity, water, and sewage (or a compliant septic system), must be available and functional.

Properties Undergoing Significant Renovation

While the USDA aims to revitalize rural areas, it generally does not finance homes that require extensive rehabilitation or are considered uninhabitable in their current state. Properties that are severely damaged, have significant structural issues, or are essentially shells requiring a complete rebuild will typically not qualify. However, the USDA does offer a section 504 loan, which can be used for repairs and improvements on existing homes in eligible rural areas, but this is a different program than the standard home loan. The standard home loan focuses on properties that are already in a livable condition.

Property Usage and Exceptions: Navigating Specific Scenarios

The intended use of the property and certain unique circumstances can also impact its eligibility for USDA financing. Understanding these nuances is key to avoiding unexpected hurdles.

Manufactured Homes

Manufactured homes can be eligible for USDA financing, but they must meet specific requirements. These homes must be built on a permanent foundation, have a minimum of 400 square feet of living space, and be on a single chassis. They must also be affixed to the land they are situated on, and the land must be owned by the borrower. Older manufactured homes or those that do not meet these stringent criteria may not be eligible.

Agricultural Land and Usage

While the USDA’s mission is rooted in rural development, homes with a significant portion of their acreage dedicated to commercial agricultural operations may not qualify for the standard single-family home loan. The primary purpose of the loan is for a dwelling, not for supporting a large-scale farming enterprise. However, a home with a modest amount of land for personal use, such as a garden or a few animals for personal consumption, is generally acceptable as long as it meets all other requirements. If the primary purpose of the property is commercial agriculture, other USDA programs or conventional financing might be more appropriate.

In-Law Suites or Accessory Dwelling Units (ADUs)

Properties that include a separate in-law suite or ADU that could be considered an independent living space might face scrutiny. The USDA loan is intended for a single-family dwelling. If the ADU is designed or used as a completely separate residence, it could disqualify the property. However, if it’s an integrated part of the main home, such as a basement apartment or a connected in-law unit that doesn’t have a separate kitchen or entrance, it might be acceptable. Each case is reviewed individually based on its specific configuration and intended use.

Properties with Commercial Use

Homes that are mixed-use, meaning they have a significant commercial component alongside the residential space, are generally not eligible. For example, a property that is primarily a retail store with a small apartment above it would likely be disqualified. The focus of the USDA loan program is on single-family owner-occupied residences.

By thoroughly understanding these disqualifying factors, prospective homebuyers can proactively identify suitable properties and navigate the USDA financing process with greater confidence. Consulting with a USDA-approved lender early in your search is highly recommended, as they can provide expert guidance and help you avoid common pitfalls. With diligent research and proper planning, the dream of homeownership in a USDA-eligible area can become a tangible reality.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.