The question, “What credit card is the CBNA?”, frequently surfaces in online searches, indicating a common point of confusion for consumers navigating the complex landscape of credit card issuers and their affiliations. This inquiry isn’t about a specific, standalone credit card product known as “CBNA.” Instead, it’s a query that often arises from encountering the abbreviation “CBNA” on statements, promotional materials, or during customer service interactions, leading individuals to seek clarity on the entity behind their credit card. This article aims to demystify the CBNA, explaining its origins, its relationship with a major financial institution, and what it signifies for cardholders.

Understanding the Origin of the CBNA Abbreviation

The seemingly enigmatic “CBNA” is not a credit card brand in itself, but rather an abbreviation that has historically represented a significant entity within the credit card processing and issuance industry. Unpacking its etymology reveals its roots and helps to contextualize its presence.

The Evolution of “CBNA” in Financial Services

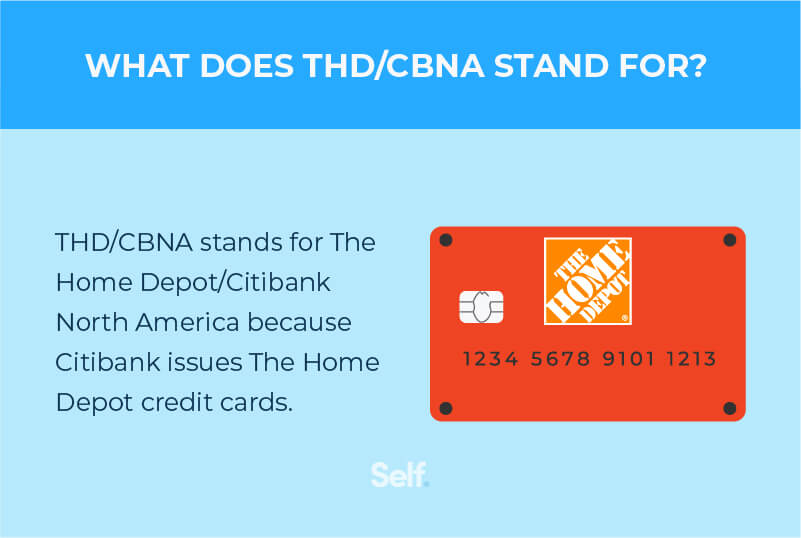

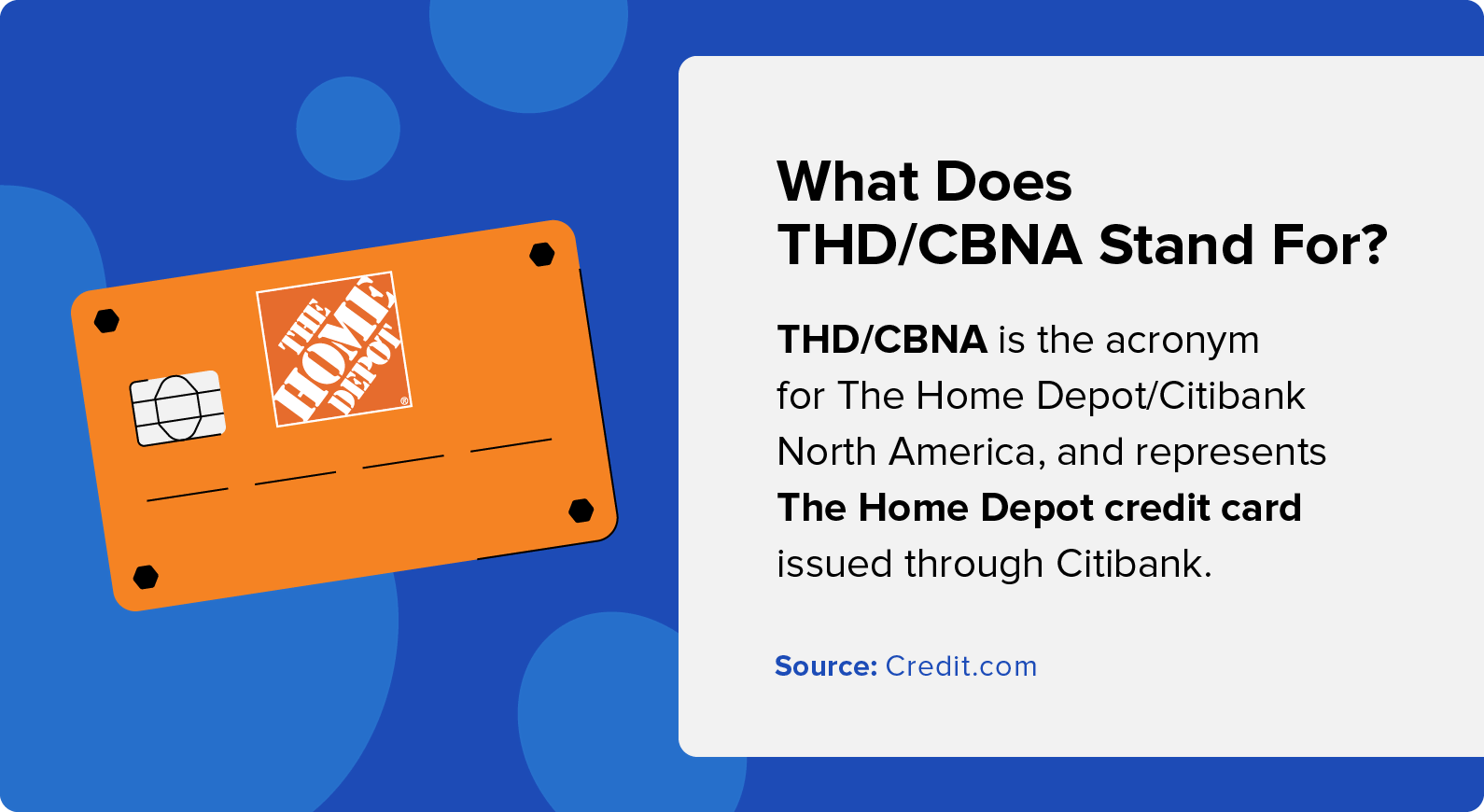

For many years, “CBNA” stood for “Citibank, N.A.” N.A. in this context signifies “National Association,” a legal designation for banks that are chartered under federal law. Citibank, of course, is a globally recognized financial institution and a major issuer of credit cards. Therefore, when individuals saw “CBNA” on their credit card statements, they were often looking at transactions or account information related to a Citibank-issued card.

The use of “CBNA” was particularly prevalent in the early days of electronic banking and card processing. It served as a concise identifier for the bank on transaction logs and billing statements. Over time, as banking and credit card industries evolved, the direct use of “CBNA” as a primary identifier for consumers has become less common. However, its legacy persists, and it can still appear in various contexts, leading to ongoing confusion.

Why the Confusion?

The persistence of this question stems from several factors:

- Legacy Systems and Statements: Older transaction data, archived statements, or even certain legacy systems within financial institutions might still use “CBNA” as a shorthand.

- Third-Party Processors: Sometimes, transactions might be processed through intermediary entities that retain older identifiers, leading to “CBNA” appearing on a statement even if the card is directly associated with a more modern branding.

- Customer Service Interactions: When calling customer service for a card that was originally issued by Citibank, representatives might refer to the account using the historical “CBNA” designation.

- Misinterpretation: Without a clear understanding of banking abbreviations, “CBNA” can easily be mistaken for a specific card product or a competitor to major issuers.

Essentially, the confusion arises from “CBNA” being an internal or historical identifier for a well-known issuer, rather than a consumer-facing brand.

Citibank’s Role as a Major Credit Card Issuer

To fully understand what “CBNA” represents, it’s crucial to delve into the role of Citibank as one of the world’s largest credit card issuers and how its operations connect to this abbreviation.

A Global Financial Powerhouse

Citibank, part of Citigroup, has a long and storied history in the financial services sector. It is renowned for its extensive network, diverse product offerings, and significant presence in both retail and institutional banking. In the realm of credit cards, Citibank has been a dominant force for decades, issuing a wide array of credit cards catering to various consumer needs, from rewards-focused travel cards to cashback options and balance transfer solutions.

Their credit card portfolio includes popular products that are recognized by their brand names, such as the Citi® Double Cash Card, Citi® Premier Card, and various co-branded cards. These are the names consumers typically associate with their credit cards. However, behind the scenes, the legal entity responsible for issuing and managing these accounts is often a Citibank-affiliated national bank.

How “CBNA” Fits into Citibank’s Structure

The “CBNA” abbreviation is intrinsically linked to the legal structure of Citibank. When a bank operates as a “National Association” (N.A.), it signifies a federal charter. This means that Citibank, as Citibank, N.A., is a federally chartered entity. For a long time, and sometimes still today in specific internal or historical contexts, this national banking association was the entity that legally issued and managed the credit cards. Therefore, seeing “CBNA” on a statement or during an inquiry was a direct reference to a transaction or account handled by Citibank, National Association.

This is similar to how other large banks operate. For instance, you might see “Bank of America, N.A.” or “JPMorgan Chase Bank, N.A.” as the legal entity behind your credit card or bank account, even if you primarily interact with the “Bank of America” or “Chase” brand. The N.A. designation is a legal and regulatory requirement for national banks, and the abbreviation “CBNA” was simply a convenient shorthand for this entity.

Identifying Your Credit Card When “CBNA” Appears

For consumers who encounter “CBNA” and are trying to pinpoint which credit card it relates to, a systematic approach can help clarify the situation. It’s about tracing the abbreviation back to its issuer.

Analyzing Your Statements

The most direct way to identify the card associated with “CBNA” is to carefully examine your credit card statements. Look for the following:

- Merchant Name: While “CBNA” might appear as the issuer or processor, the merchant where you made the transaction will be listed. This can help you recall the purchase.

- Transaction Date and Amount: Cross-referencing these details with your spending habits can jog your memory.

- Other Issuer Information: Often, even if “CBNA” is present, the statement will also clearly display the actual brand name of your credit card (e.g., Citi® Double Cash) and the issuing bank’s full name or logo. Look for the primary branding that you recognize.

- Customer Service Contact Information: Statements invariably include customer service phone numbers and websites. If you’re still unsure, these are your first points of contact.

Contacting Your Bank or Issuer

If you are still unable to definitively identify the card, the most reliable method is to contact the customer service department of the financial institution you believe issued the card.

- If you suspect it’s a Citibank card: Call the general Citibank customer service line. You can usually find this number on their official website or on other credit cards you may have from them. Be prepared to provide account details or personal information to verify your identity. Explain that you are seeing “CBNA” and need clarification. They will be able to trace the identifier to your specific card account.

- If you have other cards from different issuers: If you have credit cards from other major banks (e.g., Chase, American Express, Capital One), review your statements from those issuers as well. It’s possible that “CBNA” is appearing in an unexpected context, or perhaps it’s a different abbreviation altogether that you’ve mistaken.

Understanding the Shift in Branding

It’s important to note that over the years, financial institutions have updated their branding and how they present themselves to consumers. While “CBNA” was a functional identifier, the marketing and customer-facing presentation has shifted towards using more recognizable brand names like “Citibank” or the specific product names of their credit cards. This shift means that newer statements and communications are less likely to prominently feature “CBNA.” However, for historical records or certain backend processing, it can still surface.

The Broader Context: Credit Card Issuers and Identifiers

The “CBNA” inquiry is a microcosm of a larger phenomenon in the financial world: the often-obscure relationship between consumer-facing brands and the legal entities that issue financial products. Understanding this dynamic can empower consumers to navigate their financial lives with greater clarity.

The Role of Issuers vs. Networks

It’s crucial to distinguish between credit card issuers and credit card networks.

- Issuers: These are the financial institutions that actually provide the credit, manage the accounts, set the terms and conditions, and bear the risk of lending. Examples include Citibank, Chase, American Express, and Capital One. “CBNA” refers to one such issuer (Citibank).

- Networks: These are the companies that facilitate transactions between merchants and issuers. They provide the infrastructure for payments to occur. The major networks are Visa, Mastercard, American Express (which also acts as an issuer), and Discover. Your credit card will prominently display the logo of one of these networks. The network facilitates the transaction, but the issuer is the entity that provides the credit.

Why Identifiers Matter for Consumers

While it may seem like a minor detail, understanding who is behind your credit card has practical implications:

- Customer Service: Knowing your issuer helps you direct your inquiries and complaints to the right place.

- Benefits and Rewards: Different issuers have distinct loyalty programs, benefits, and rewards structures. Understanding your issuer is key to maximizing these.

- Fraud Protection and Disputes: When dealing with fraudulent charges or seeking to dispute a transaction, you’ll interact directly with your issuing bank.

- Financial Health: Your credit card activity is reported to credit bureaus by the issuer, impacting your credit score.

The “CBNA” question, while seemingly niche, highlights the importance of financial literacy. It reminds consumers that the name on their card is often a brand, while the underlying entity is a legally chartered financial institution, and sometimes, an abbreviation like “CBNA” is simply a historical or functional identifier for that institution. By understanding these distinctions, consumers can approach their credit card usage and management with greater confidence and control.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.