The term “small business” is often used colloquially to describe the corner coffee shop, a boutique creative agency, or a local hardware store. However, from a financial and regulatory perspective, the classification of a small business is far more nuanced. It is not merely a matter of physical size or community presence; rather, it is a strictly defined category based on specific economic metrics, industry standards, and ownership structures.

For entrepreneurs, investors, and financial advisors, understanding what classifies a small business is critical. This classification dictates eligibility for government contracts, access to specialized financial tools, tax obligations, and the ability to secure Small Business Administration (SBA) loans. In the world of business finance, being “small” is often a strategic advantage that allows for fiscal flexibility and targeted growth opportunities.

The Quantitative Metrics: Revenue and Headcount Standards

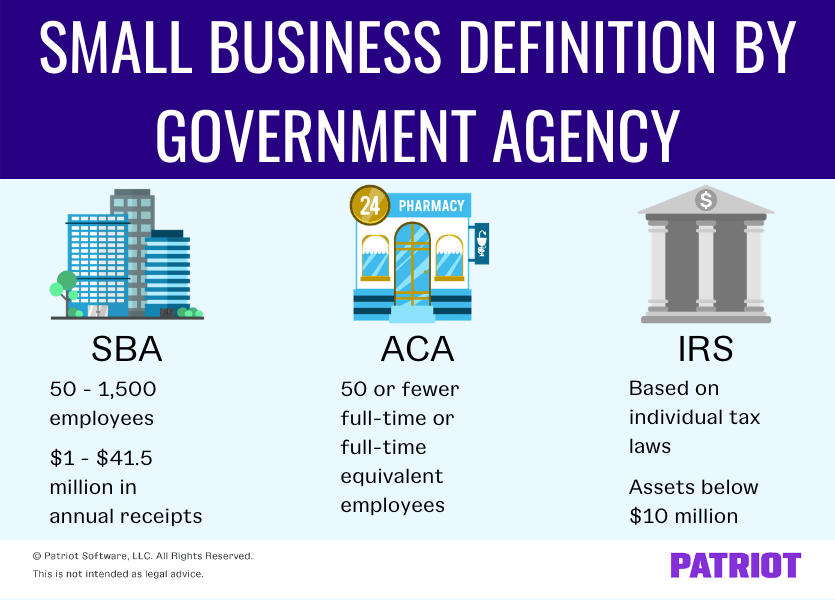

At the federal level in the United States, the primary authority on this classification is the Small Business Administration (SBA). The SBA does not use a one-size-fits-all approach. Instead, it utilizes “Size Standards” that vary significantly depending on the industry in which a company operates. These standards are primarily measured by two quantitative factors: annual receipts and the average number of employees.

The Role of NAICS Codes in Financial Benchmarking

Every business is categorized under the North American Industry Classification System (NAICS). The SBA assigns a size standard to each of these codes. For example, a manufacturing firm might be considered “small” even if it has 1,500 employees, whereas a retail business might lose its “small” status if it exceeds $30 million in annual revenue.

From a financial planning perspective, knowing your NAICS code is the first step in determining your status. It provides a benchmark for how your business is viewed by lenders and government agencies. If your firm’s revenue is approaching the ceiling for its industry, it may trigger a need for a shift in financial strategy, as certain “small business only” benefits may soon be phased out.

Revenue-Based vs. Employee-Based Thresholds

Generally, service-based and retail industries are evaluated based on their average annual receipts over a three-year or five-year period. This revenue-based approach ensures that companies with high profit margins but low overhead are categorized fairly. Conversely, manufacturing, mining, and wholesale trade industries are typically evaluated based on their headcount.

In these sectors, “small” usually means fewer than 500 employees, though this can climb higher in capital-intensive industries. For a business owner, monitoring these numbers is a key part of fiscal oversight. Exceeding these limits by even a small margin can result in the loss of “set-aside” contract opportunities, which are often the lifeblood of specialized firms.

Financial Implications: Access to Capital and Government Incentives

The primary reason classification matters is the financial door it opens—or closes. Small businesses have access to a unique ecosystem of capital that is unavailable to larger corporations. This ecosystem is designed to offset the inherent risks that smaller entities face when competing against established market leaders.

The Power of SBA-Backed Loans

One of the most significant advantages of being classified as a small business is the ability to qualify for SBA loans, such as the 7(a) and 504 programs. These are not loans directly from the government; rather, the SBA guarantees a portion of the loan provided by private lenders.

This guarantee reduces the risk for the bank, often resulting in lower interest rates, longer repayment terms, and smaller down payments. For a growing business, this access to affordable capital is the difference between stagnation and expansion. However, to secure these funds, the business must prove it meets the size standards and demonstrates “need”—a financial prerequisite that ensures the capital is going to entities that cannot otherwise obtain credit on reasonable terms.

Government Contract Set-Asides

The federal government is the world’s largest buyer of goods and services, and by law, it must funnel a specific percentage of its spending—currently around 23%—toward small businesses. These “set-asides” are a massive revenue stream for companies in sectors like construction, IT services, and defense.

Financially, winning a set-aside contract can provide a small business with long-term revenue stability and the “past performance” record needed to compete for even larger projects. To maintain this advantage, a company must certify its size status annually, ensuring its financial growth hasn’t pushed it into the “large” category.

Tax Structures and the Small Business Framework

Classification isn’t just about how much money you make; it’s about how that money is handled by the tax authorities. Small businesses in the U.S. often operate under specific legal structures that offer distinct financial advantages over C-corporations.

Pass-Through Entities and Fiscal Efficiency

Most small businesses are organized as “pass-through” entities, such as Sole Proprietorships, Partnerships, LLCs, or S-Corporations. In these structures, the business itself does not pay corporate income tax. Instead, the profits and losses “pass through” to the owners’ personal tax returns.

This structure is highly beneficial for small-scale operations because it avoids the “double taxation” that hits C-corps (where profits are taxed at the corporate level and again as dividends to shareholders). From a cash flow perspective, pass-through taxation allows small business owners to retain more capital within the business for reinvestment or personal income.

Section 179 Deductions and Capital Expenditures

The tax code also provides specific incentives for small businesses to invest in themselves. Under Section 179 of the IRS code, small businesses can often deduct the full purchase price of qualifying equipment or software purchased during the tax year.

For a large corporation, these assets might have to be depreciated over several years. For a small business, the ability to write off the entire expense in year one provides an immediate financial cushion and reduces the overall tax liability. This makes the classification of “small” an essential part of a company’s tax-mitigation strategy.

The Operational Framework: Ownership and Control

Beyond the balance sheet, the classification of a small business depends heavily on its organizational structure. To be legally recognized as a small business, an entity must be “independently owned and operated.” This means the financial and operational strings cannot be pulled by a larger parent company.

The Independent Ownership Requirement

If a large corporation owns more than 50% of a smaller company, that smaller company generally loses its small business status. This is known as the “Affiliation Rule.” The SBA looks at who has the power to control the business, whether through ownership, management, or previous relationships.

Financially, this prevents large firms from creating “shell” small businesses to unfairly capture government contracts or low-interest loans. For entrepreneurs looking for an exit strategy, selling a majority stake to a private equity firm or a larger competitor is a major financial milestone, but it also marks the end of the company’s life as a small business.

Small Business vs. Startup: A Financial Distinction

While “small business” and “startup” are often used interchangeably, they are different financial animals. A traditional small business is typically focused on long-term profitability and sustainable growth within a local or regional market. A startup, however, is often designed for rapid scale, fueled by venture capital (VC) or angel investment.

In many cases, a high-growth startup may meet the headcount and revenue requirements to be “small,” but its financial goals are vastly different. While a small business manages its cash flow to maintain stability, a startup might burn through millions in capital to capture market share. Understanding which path a business is on is vital for determining the right financial tools—whether that means a traditional bank line of credit or a Series A funding round.

The Strategic Value of Remaining “Small”

In the journey of enterprise, growth is usually the goal. However, there is a “sweet spot” in business finance where a company is large enough to be highly profitable but still small enough to qualify for the benefits of small business classification.

Strategic business owners often monitor their metrics closely as they approach the SBA limits. Some may choose to slow expansion or spin off certain divisions to maintain their “small” status and the competitive financial advantages that come with it. By staying within these classifications, businesses can leverage tax incentives, favorable lending, and exclusive contract opportunities to build a robust financial foundation.

Ultimately, what classifies a small business is a combination of its industry-specific revenue, its headcount, its independent structure, and its legal tax framework. By mastering these definitions, business owners can navigate the complex world of finance with greater precision, ensuring they utilize every available resource to drive their vision forward.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.