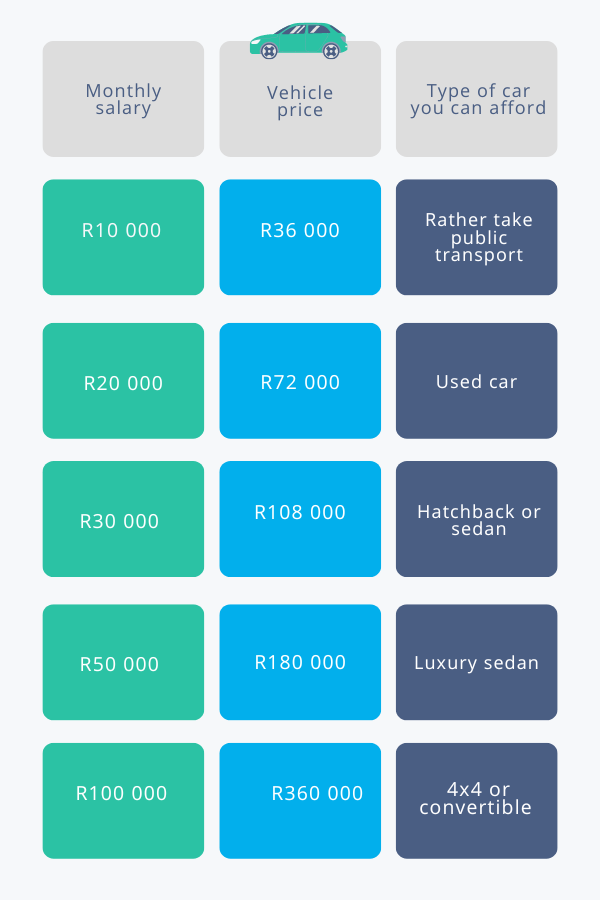

The allure of a new car – the sleek design, the scent of fresh upholstery, the promise of reliable journeys – is a powerful one. For many, a vehicle represents freedom, convenience, and a significant life investment. However, the excitement of car shopping often collides with the intricate reality of personal finance. Overestimating what one can truly afford can lead to financial strain, while underestimating might mean missing out on a car that perfectly fits one’s needs and budget. This is where the “What Car Can I Afford Calculator” emerges as an indispensable tool. Far more than just crunching numbers, it serves as a digital financial advisor, empowering individuals to make informed, confident decisions about one of their most substantial expenditures. This article will delve into the critical factors that define car affordability, elucidate how these calculators function, and outline strategic approaches to align your automotive aspirations with your financial reality.

Deconstructing Car Affordability: Beyond the Monthly Payment

Many prospective car buyers make the mistake of focusing solely on the monthly payment, overlooking the broader financial implications of vehicle ownership. True car affordability is a complex equation that encompasses a myriad of direct and indirect costs, all of which must be considered within the context of your personal financial health.

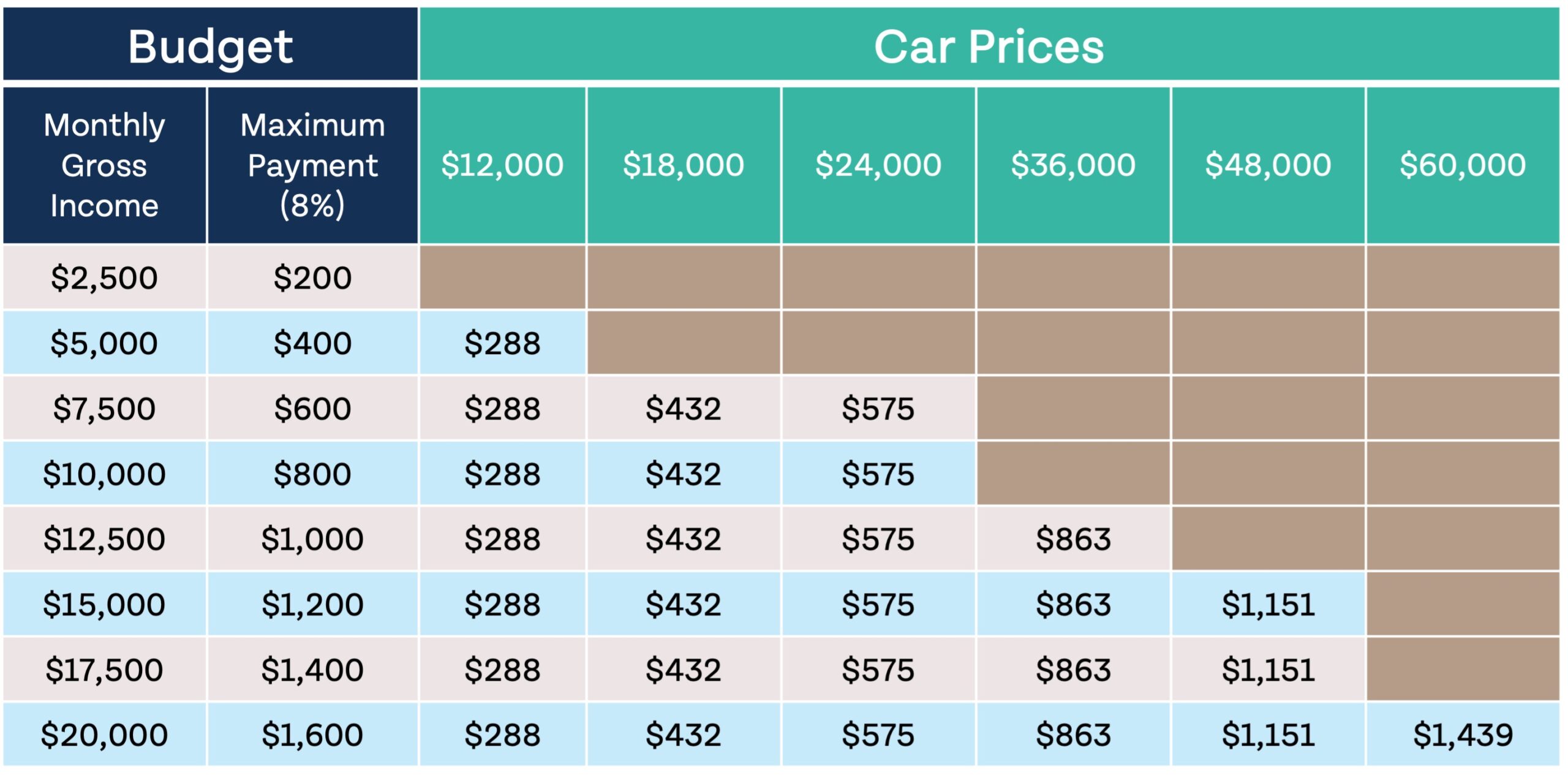

The 20/4/10 Rule and Its Limitations

A common heuristic in car buying is the “20/4/10 Rule.” This guideline suggests putting down at least 20% of the car’s purchase price, financing the car for no more than four years (48 months), and ensuring that total car expenses (loan payment, insurance, fuel, maintenance) do not exceed 10% of your gross monthly income. This rule serves as an excellent starting point, providing a conservative framework for responsible car ownership. A substantial down payment reduces your loan amount, lowering monthly payments and the total interest paid over the life of the loan. A shorter loan term means you pay off the car faster, reducing the risk of being “upside down” (owing more than the car is worth) and significantly cutting down on interest expenses. Finally, capping total car expenses at 10% of gross income helps ensure that your vehicle doesn’t become a financial burden, leaving room for other essential expenses and savings goals.

However, the 20/4/10 rule is a guideline, not an immutable law. Its applicability can vary based on individual circumstances. Someone with a high income, substantial savings, and minimal other debts might comfortably exceed the 10% income threshold without financial distress, especially if their other financial goals are well-funded. Conversely, individuals with lower incomes, significant existing debt, or a less stable financial footing might find even the 10% target too ambitious, needing to aim lower to maintain financial security. The rule should be viewed as a baseline to encourage thoughtful planning, rather than a rigid benchmark that dictates every purchasing decision.

Total Cost of Ownership (TCO) – The Unseen Expenses

The sticker price and monthly loan payment are just the tip of the iceberg when it comes to car ownership. The “Total Cost of Ownership” (TCO) reveals the full financial commitment and is a critical factor often overlooked. Understanding TCO is paramount for accurate affordability assessment:

- Insurance: Premiums vary wildly based on the car’s make, model, year, safety features, your driving record, age, location, and chosen coverage. A sportier, high-performance, or luxury vehicle will almost invariably incur higher insurance costs than a standard sedan or SUV.

- Fuel: Your daily commute, weekend adventures, and the car’s miles per gallon (MPG) rating will dictate your fuel expenditure. Hybrid and electric vehicles offer significant savings here, but often come with a higher initial purchase price.

- Maintenance and Repairs: While new cars typically come with warranties that cover initial repair costs, routine maintenance (oil changes, tire rotations, brake pads) is still required. Used cars, especially older ones, are more prone to unexpected repairs, which can be costly. Different brands and models also have varying reputations for reliability and parts costs.

- Registration, Taxes, and Fees: Depending on your state, these can include sales tax on the purchase, annual registration fees, license plate fees, and potential emissions testing fees. These upfront and recurring costs can add up significantly.

- Depreciation: This is arguably the largest “unseen” cost. Cars begin to depreciate the moment they leave the dealership lot, often losing 20-30% of their value in the first year alone. While you don’t write a check for depreciation, it directly impacts the car’s resale value and your financial equity in the vehicle.

By considering these TCO elements, buyers gain a much clearer picture of the true financial impact of their chosen vehicle, moving beyond the superficial monthly payment to a comprehensive understanding of their financial commitment.

Your Personal Financial Landscape

Ultimately, car affordability is deeply personal, rooted in your individual financial situation. A holistic assessment requires an honest look at your current and projected financial health:

- Income Stability and Job Security: A steady, reliable income stream provides the foundation for consistent loan payments. Any uncertainty in your employment situation should prompt a more conservative approach to car buying.

- Existing Debts: Your debt-to-income (DTI) ratio is a crucial metric for lenders and for your own financial well-being. High credit card balances, student loans, or mortgage payments will reduce the amount of disposable income available for a car loan, and can negatively impact your ability to secure favorable interest rates.

- Savings and Emergency Fund: A robust emergency fund provides a critical safety net against unexpected expenses, whether they relate to car repairs, job loss, or medical emergencies. Draining your savings to make a down payment can leave you vulnerable.

- Other Financial Goals: Your car purchase shouldn’t derail other important financial objectives, such as saving for retirement, a down payment on a home, or your children’s education. Prioritizing these long-term goals is vital for overall financial health.

Understanding these intertwined aspects allows for a realistic evaluation of what car you can genuinely afford without compromising your financial stability.

How “What Car Can I Afford” Calculators Work: A Digital Financial Advisor

A “What Car Can I Afford Calculator” acts as a sophisticated financial modeling tool, taking your personal financial data and projecting realistic car affordability. It moves beyond simple payment calculations to provide a more holistic view of your potential car budget.

Key Inputs: What Information Do You Need?

To leverage these calculators effectively, you need to provide accurate information about your financial standing and preferences:

- Down Payment Amount: The cash you plan to put down upfront. A larger down payment reduces the principal loan amount, leading to lower monthly payments and less interest paid over time.

- Desired Loan Term (months): The number of months you wish to take to repay the loan (e.g., 36, 48, 60, 72 months). Shorter terms mean higher monthly payments but less total interest; longer terms offer lower monthly payments but accumulate more interest.

- Interest Rate (APR): The Annual Percentage Rate on the car loan. This is heavily influenced by your credit score. A higher credit score typically translates to a lower APR, significantly reducing the overall cost of the loan. It’s often beneficial to get pre-approved for a loan to know your potential APR before shopping.

- Monthly Income (Gross/Net): Your total income before taxes and deductions (gross) or after (net). Some calculators might ask for gross to align with DTI calculations used by lenders, while others may ask for net for a more direct view of disposable income.

- Existing Monthly Debt Payments: A sum of all your other monthly debt obligations, such as mortgage/rent, student loan payments, credit card minimums, and personal loan payments. This helps the calculator assess your DTI ratio.

- Desired Monthly Car Budget: Instead of calculating what car you can afford, some calculators work in reverse, telling you what car price you can target if you already have a specific monthly payment in mind.

The Calculation Engine: Estimating Your Limits

Once you input the data, the calculator’s engine performs several critical computations:

- Reverse Engineering from Desired Monthly Payment: If you specify a maximum monthly payment, the calculator uses the loan term and interest rate to determine the maximum loan amount you can take out. Adding your down payment to this figure gives you the approximate maximum car price you can afford.

- Calculating Total Loan Amount Based on Income and DTI: Many sophisticated calculators integrate your monthly income and existing debts to calculate your debt-to-income (DTI) ratio. Lenders typically look for a DTI below 36-43%. The calculator uses this threshold, alongside your income, to estimate the maximum monthly car payment you can realistically manage without overextending yourself. From this maximum payment, it works backward to determine the affordable car price.

- Projecting Total Interest Paid: The calculator can show you the total amount of interest you’ll pay over the life of the loan for various scenarios. This highlights the long-term cost implications of different interest rates and loan terms.

Beyond the Basic Calculation: Advanced Features

Modern “What Car Can I Afford” calculators often go beyond simple loan payment estimations, offering features that provide an even more comprehensive view:

- Incorporating Estimated Insurance Costs: Some tools allow you to input an estimated monthly insurance premium, directly integrating it into your total monthly car expense calculation.

- Fuel Cost Estimation: Based on your estimated daily mileage and the average fuel efficiency of the car type you’re considering, the calculator can project your monthly fuel costs.

- Option for Trade-in Value: If you plan to trade in your current vehicle, you can input its estimated value, which will reduce the amount you need to finance for your new car.

- Side-by-Side Comparisons: Advanced calculators may allow you to compare different car models or financial scenarios (e.g., a new car vs. a used car, different loan terms) to see how they impact your overall budget.

By utilizing these tools, prospective buyers gain clarity and control, moving from speculative dreaming to concrete, data-driven financial planning.

Strategic Approaches to Maximizing Your Car Budget

Understanding what you can afford is the first step; strategically planning your purchase is the next. Several tactics can help you get the most car for your money while staying within your financial comfort zone.

Optimizing Your Down Payment and Loan Terms

The upfront cash you put towards a car and the duration of your loan are two of the most impactful variables in your total cost of ownership.

- The Power of a Larger Down Payment: A substantial down payment is perhaps the most effective way to reduce the financial burden of a car. It directly lowers the principal amount you need to finance, resulting in smaller monthly payments and, crucially, significantly less interest paid over the life of the loan. A larger down payment also builds immediate equity, making it less likely you’ll be upside down on your loan if the car depreciates quickly. Aim for 20% or more if possible.

- Shorter Loan Terms vs. Longer Loan Terms: While longer loan terms (e.g., 72 or 84 months) offer appealingly low monthly payments, they come at a high cost in terms of total interest paid. A 60-month loan will almost always save you thousands in interest compared to a 72-month loan for the same principal, even if the monthly payment is slightly higher. Prioritize the shortest loan term you can comfortably afford.

- Understanding the Impact of Credit Score on APR: Your credit score is a direct determinant of the interest rate you’ll be offered. A higher credit score (generally 700+) qualifies you for the best rates. Before buying a car, it’s wise to check your credit report and score, and take steps to improve it if needed. Even a few percentage points difference in APR can translate to thousands of dollars over a multi-year loan.

The New vs. Used Car Dilemma

The choice between a new and used car is a pivotal decision with significant financial implications.

- Advantages of New Cars: New cars offer the latest technology, enhanced safety features, full factory warranties, and the peace of mind of being the first owner. However, they suffer the most severe depreciation, often losing 20-30% of their value in the first year alone.

- Advantages of Used Cars: Used cars generally come with a lower purchase price and have already absorbed the steepest depreciation hit. This means they tend to depreciate slower from the point of purchase. Opting for a used car allows you to potentially afford a higher-trim model or a luxury brand that would be out of reach new. The downside can be shorter or expired warranties and the potential for unexpected maintenance issues.

- Certified Pre-Owned (CPO) as a Middle Ground: CPO vehicles bridge the gap between new and used. These are late-model, low-mileage used cars that have undergone rigorous inspections and are often backed by an extended manufacturer’s warranty. While more expensive than a standard used car, they offer greater peace of mind and reliability than a typical “as-is” used purchase.

Smart Shopping and Negotiation Tactics

The price you pay for a car is often a result of your negotiation skills and preparedness.

- Research Market Prices Thoroughly: Before stepping onto a dealership lot, research the average selling price of the specific make and model you’re interested in, both new and used. Websites like Kelley Blue Book, Edmunds, and TrueCar provide valuable pricing data.

- Get Pre-Approved for a Loan: Secure a pre-approved loan from your bank or credit union before visiting dealerships. This gives you a clear understanding of your interest rate and maximum loan amount, allowing you to negotiate the car price as a cash buyer and then compare the dealer’s financing offer to your pre-approval.

- Negotiate the Out-the-Door Price: Always negotiate the “out-the-door” price, which includes all taxes, fees, and the vehicle’s selling price, rather than just focusing on the monthly payment. Dealers can manipulate loan terms to make a high purchase price seem affordable.

- Be Prepared to Walk Away: The most powerful negotiation tool you possess is your willingness to walk away if the deal isn’t right. There are always other cars and other dealerships.

Integrating Car Affordability into Your Broader Financial Plan

A car purchase is rarely an isolated event; it’s a decision that echoes throughout your entire financial landscape. Integrating car affordability into your broader financial plan ensures that your vehicle enhances, rather than detracts from, your overall financial well-being.

The Opportunity Cost of a Car Purchase

Every dollar spent on a car, particularly a more expensive one, represents a dollar that cannot be spent or invested elsewhere. This is the concept of opportunity cost. A larger car payment or longer loan term might mean:

- Less for Investments: Slower progress towards retirement savings, college funds, or other investment goals.

- Delayed Homeownership: Less money available for a down payment on a house or for renovation projects.

- Increased Debt: Less capacity to pay down existing high-interest debt, keeping you in debt longer.

Consider whether the joy and utility of a more expensive car outweigh the potential long-term financial benefits of investing or saving that money instead.

Regular Budget Review and Adjustments

Bringing a new car into your life necessitates a thorough review and potential adjustment of your overall household budget.

- Impact on Overall Budget: Accurately factor in the new monthly payment, increased insurance premiums, and estimated fuel and maintenance costs. See how these new expenditures affect your disposable income.

- Revisiting Other Spending Categories: You may need to trim spending in other discretionary categories (e.g., dining out, entertainment, subscriptions) to accommodate your new car expenses without compromising essential bills or savings.

- The Importance of an Emergency Fund: Maintaining a robust emergency fund is even more crucial with a new car. Unexpected repairs, a fender bender not fully covered by insurance, or unforeseen maintenance can quickly drain savings if you’re not prepared. Aim for 3-6 months of living expenses in an accessible savings account.

Future-Proofing Your Car Ownership

Smart financial planning extends beyond the current purchase, considering the entire lifecycle of car ownership.

- Considering Your Next Car Purchase: Even as you buy your current vehicle, have a rough idea of its expected lifespan and depreciation. This helps you anticipate when your next car purchase might be necessary and how much you might get for your current vehicle in trade.

- Building Savings for Maintenance or Future Down Payments: Start a dedicated savings fund for future car maintenance or for the down payment on your next vehicle. This proactive approach avoids financial shocks down the line.

- Understanding Trade-in Values and Depreciation Trends: Stay informed about how different makes and models hold their value. Choosing a car with slower depreciation can save you money in the long run when you eventually sell or trade it in.

Conclusion

The journey to purchasing a car, while exciting, is fraught with financial complexities that demand careful consideration and strategic planning. The “What Car Can I Afford Calculator” stands as an invaluable ally in this process, transforming a daunting task into an organized, data-driven decision. By moving beyond the surface-level monthly payment to embrace the total cost of ownership, understanding your personal financial landscape, and leveraging smart buying strategies, you can confidently navigate the automotive market. A car is an essential tool for modern life, but it should never become a burden that compromises your financial well-being. Make an informed, responsible, and confident decision, ensuring your new vehicle serves as a source of convenience and joy, rather than financial stress.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.