For millions of eligible service members, veterans, and surviving spouses, the VA home loan program represents one of the most significant and deserved benefits of their service. Offering unparalleled advantages like no down payment and no private mortgage insurance (PMI), VA loans are a cornerstone of financial stability for military families seeking to achieve homeownership. However, like any mortgage product, the interest rate associated with a VA loan is a critical factor influencing affordability and long-term costs. Understanding “what are VA interest rates today” requires a nuanced look at current market dynamics, how these rates are determined, and what borrowers can do to secure the most favorable terms.

Interest rates are not static; they fluctuate daily, sometimes hourly, driven by a complex interplay of economic indicators, monetary policy, and market sentiment. For VA loans specifically, while they share many characteristics with conventional mortgages, certain features inherent to the program can sometimes lead to slightly different rate dynamics. This article aims to demystify VA loan interest rates in today’s environment, providing a comprehensive guide for those looking to leverage this invaluable benefit.

Understanding the Landscape of VA Loans and Their Unique Advantages

Before diving into the specifics of interest rates, it’s crucial to grasp the fundamental nature of VA loans. These are not loans issued directly by the Department of Veterans Affairs (VA) but rather guaranteed by the VA, allowing private lenders (banks, credit unions, mortgage companies) to offer more attractive terms to qualified borrowers. This guarantee protects lenders from losses if a borrower defaults, which is why they can offer such favorable conditions.

Eligibility Requirements for VA Loans

Eligibility is the first hurdle for any prospective VA loan borrower. It’s primarily based on service history, with specific requirements for active duty personnel, veterans, National Guard members, Reservists, and surviving spouses. A Certificate of Eligibility (COE) is the official document that confirms a veteran’s eligibility for the benefit. While the VA establishes eligibility, the lender assesses creditworthiness, income, and debt-to-income ratios, much like any other mortgage.

Key Advantages of VA Loans

The distinct benefits of VA loans are what make them so appealing:

- No Down Payment: For most eligible borrowers, a VA loan requires no money down, making homeownership accessible even without substantial savings.

- No Private Mortgage Insurance (PMI): Unlike conventional loans with less than 20% down payment, VA loans do not require PMI. This significantly reduces monthly housing costs and saves borrowers thousands of dollars over the life of the loan.

- Competitive Interest Rates: While varying daily, VA loan interest rates are often comparable to, and sometimes even lower than, conventional loan rates, thanks to the VA guarantee.

- Limited Closing Costs: The VA sets limits on certain closing costs that veterans can be charged, and some costs can be paid by the seller.

- No Prepayment Penalties: Borrowers can pay off their loan early without incurring extra fees.

- Assumability: In certain circumstances, a VA loan can be assumed by another qualified veteran, which can be an attractive feature in a rising interest rate environment.

How VA Loans Differ from Conventional Mortgages

While both serve the purpose of home financing, VA loans diverge significantly from conventional mortgages. Conventional loans are not government-backed and often require a down payment, typically 5-20% or more, to avoid PMI. Their interest rates are purely market-driven, and lender requirements for credit scores and debt ratios can be stricter. FHA loans, another government-backed option, require a down payment (as low as 3.5%) and mandate mortgage insurance premiums (MIP) for the life of the loan or a significant portion of it, regardless of equity, making VA loans often the more cost-effective choice for eligible veterans.

The Dynamics of VA Loan Interest Rates in Today’s Market

Understanding what determines “today’s” VA interest rates involves looking at a broader economic picture. Mortgage rates, including VA rates, are primarily influenced by bond market performance, specifically the yield on mortgage-backed securities (MBS). These securities rise and fall with investor demand, which in turn reacts to various economic signals.

Factors Influencing VA Interest Rates

Several key factors play a role in shaping VA interest rates on any given day:

- Federal Reserve Policy: While the Fed doesn’t directly set mortgage rates, its decisions on the federal funds rate and its overall monetary policy (like quantitative easing or tightening) heavily influence the broader interest rate environment, impacting everything from short-term loans to long-term mortgages.

- Inflation: High inflation often leads to higher interest rates as lenders demand more compensation for the erosion of money’s purchasing power over time.

- Economic Growth and Employment: Strong economic data and low unemployment can signal potential inflation, prompting a rise in rates. Conversely, economic slowdowns or recession fears can sometimes lead to lower rates as investors seek the safety of bonds.

- Housing Market Activity: Supply and demand dynamics within the housing market can also exert some influence, though less directly than broader economic indicators.

- Lender-Specific Factors: Each individual lender has its own operational costs, profit margins, and risk assessments, which can lead to variations in the rates they offer. This is why shopping around is so crucial.

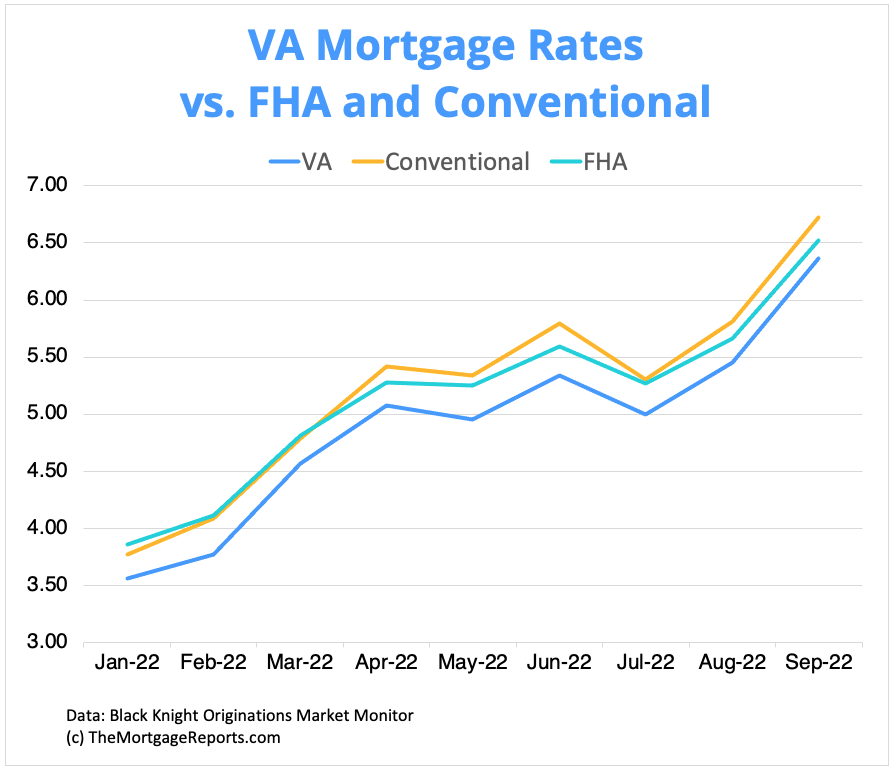

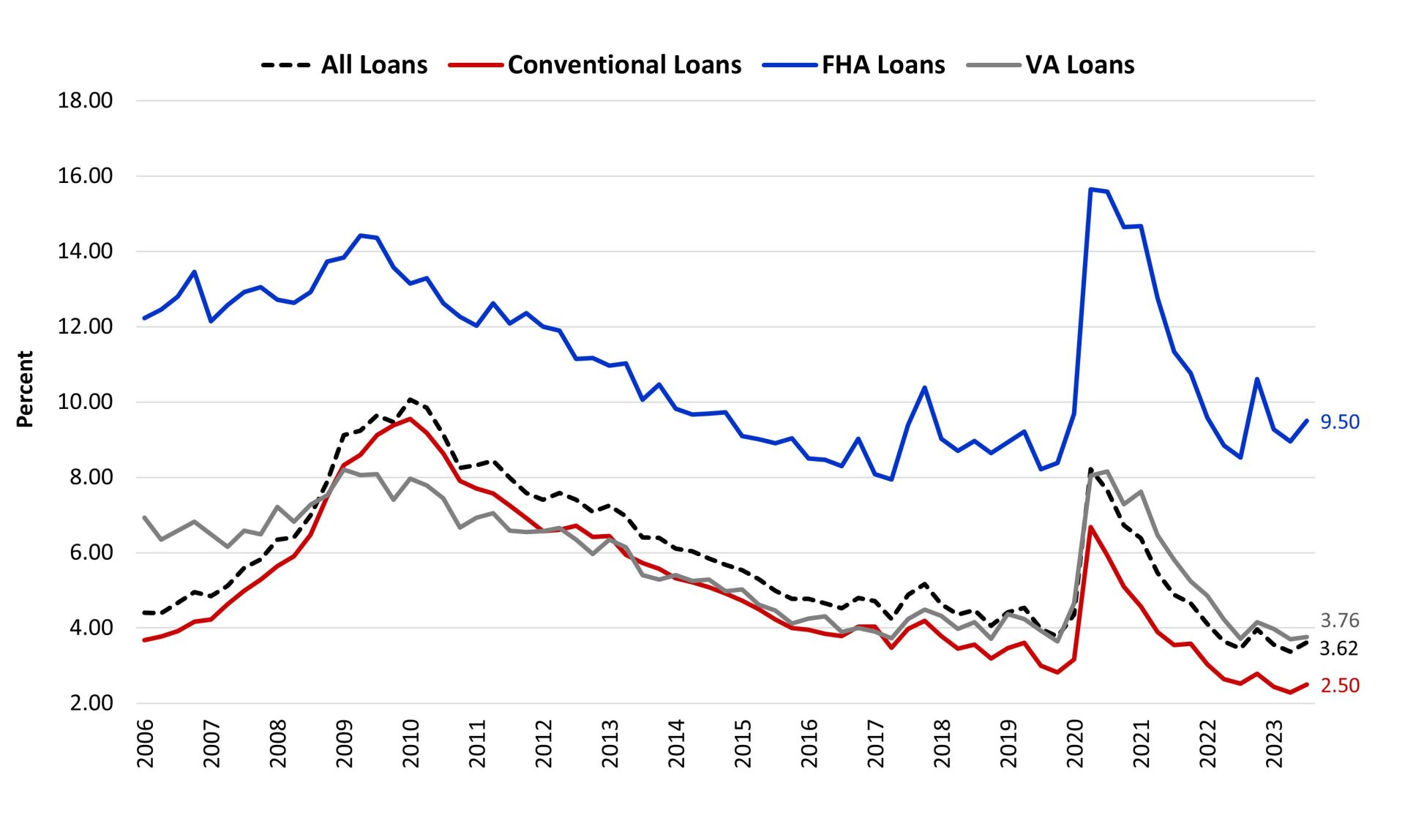

How VA Rates Compare to Other Loan Types

In today’s market, VA rates generally remain highly competitive. Often, they are similar to or even slightly lower than FHA and conventional loan rates for borrowers with excellent credit. The absence of PMI for VA loans is a significant advantage that makes the “all-in” monthly payment exceptionally attractive. However, borrowers should always compare the full package—interest rate, closing costs, and fees—across all eligible loan types to determine the best option for their specific financial situation.

The Role of Credit Score in Securing the Best VA Rates

While the VA itself doesn’t set a minimum credit score, individual lenders do. A strong credit score (generally 620 or higher, with 700+ being ideal) demonstrates a borrower’s reliability and significantly increases their chances of securing the lowest available VA interest rates. A lower credit score may still qualify for a VA loan, but it could come with a slightly higher interest rate to compensate the lender for increased risk. Lenders also look at the overall credit history, payment behavior, and debt-to-income ratio (DTI).

Navigating Today’s VA Loan Market

Given the daily fluctuations, knowing what VA interest rates are “today” means understanding how to navigate the current market effectively to lock in the best terms. This involves being informed, proactive, and strategic.

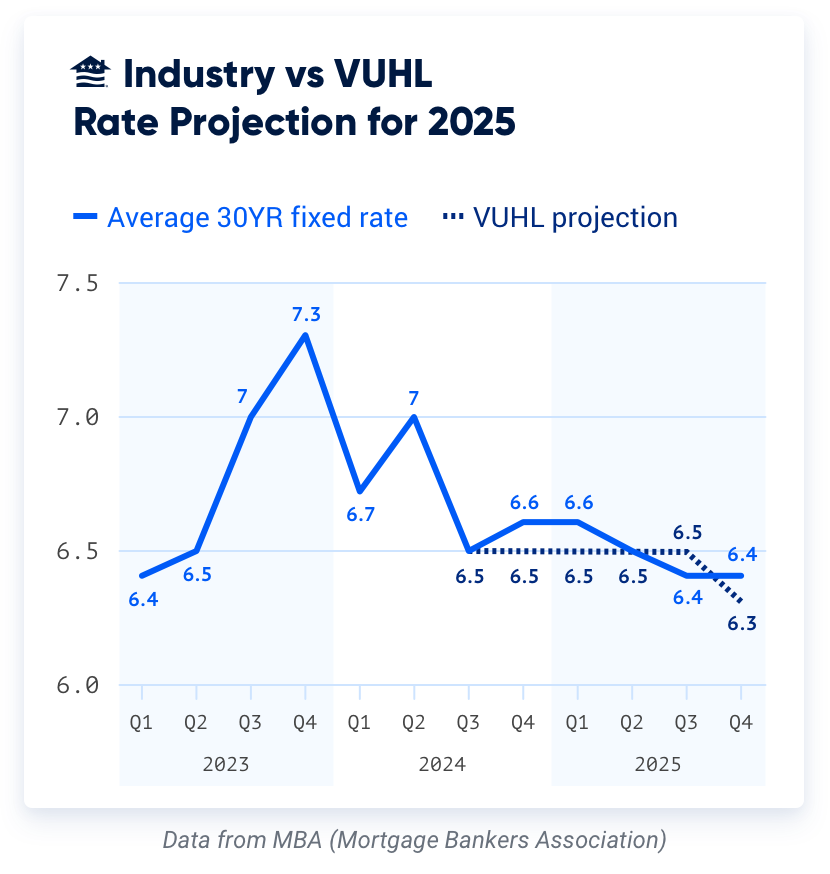

Current Market Trends and Predictions for VA Rates

The current economic climate, marked by inflation concerns, central bank responses, and geopolitical events, creates a dynamic environment for interest rates. Rates can shift based on new economic reports (like inflation data, job numbers), Federal Reserve announcements, or even global events. While no one can predict future rates with absolute certainty, staying informed about expert forecasts and economic news can help borrowers gauge potential movements. Generally, periods of economic stability and controlled inflation tend to foster more stable, and often lower, rate environments. In periods of high inflation, rates tend to climb as the Fed works to cool the economy.

Strategies for Finding Competitive VA Loan Rates

Securing the best possible VA interest rate requires a diligent approach:

- Shop Multiple Lenders: This is perhaps the most important strategy. Because lenders set their own rates and fees, comparing offers from at least 3-5 different VA-approved lenders can lead to significant savings over the life of the loan. Don’t just compare the interest rate; look at the Annual Percentage Rate (APR), which includes some fees, for a more accurate comparison.

- Improve Your Credit Score: If time permits before applying, focus on improving your credit score. Pay down debts, avoid new credit inquiries, and ensure no errors are on your credit report.

- Understand Discount Points: Borrowers can sometimes pay “discount points” (an upfront fee) to reduce their interest rate. This might be beneficial for those who plan to stay in their home for many years, as the long-term savings from a lower rate can outweigh the upfront cost.

- Be Ready to Act: When you find a favorable rate, be prepared to move quickly. Rates can change rapidly, so having your documents in order and being responsive during the application process is key.

The Importance of Lender Shopping and Rate Locks

Lender shopping is paramount. A difference of just 0.25% in an interest rate on a $300,000 loan can amount to tens of thousands of dollars over 30 years. When you receive a favorable rate quote, inquire about a rate lock. A rate lock guarantees your interest rate for a specific period (e.g., 30, 45, or 60 days) while your loan processes. This protects you if rates rise during your application period. Be aware of the lock period and any fees associated with extending it if your closing is delayed.

Beyond the Interest Rate: Other Costs and Considerations

While the interest rate is a primary driver of your monthly payment, it’s not the only financial consideration when taking out a VA loan. Understanding other associated costs is vital for a complete financial picture.

Understanding the VA Funding Fee

A unique aspect of VA loans is the VA Funding Fee. This is a one-time fee paid directly to the VA to help offset the cost of the program to taxpayers and reduce the risk to lenders. The fee amount varies depending on the loan type (purchase vs. refinance), down payment amount (if any), and whether it’s your first time using the VA loan benefit. For example, a first-time user with no down payment might pay a 2.15% funding fee, while subsequent users might pay 3.3%. Critically, some veterans are exempt from the funding fee, including those receiving VA compensation for service-connected disabilities, Purple Heart recipients, and surviving spouses. This exemption can significantly reduce the overall cost of the loan.

Closing Costs and Other Fees Associated with VA Loans

Like all mortgages, VA loans come with closing costs. These are fees associated with processing the loan and transferring property ownership. They can include appraisal fees, title insurance, recording fees, and attorney fees. While the VA limits what veterans can be charged, these costs can still add up. It’s important to get a detailed Loan Estimate from your lender, which outlines all anticipated costs. In some cases, sellers can contribute towards closing costs, and lenders may offer “no-closing-cost” options (though these often involve a slightly higher interest rate).

Refinancing Options: VA Streamline (IRRRL) and Cash-Out Refi

For veterans who already have a VA loan, two primary refinancing options exist:

- Interest Rate Reduction Refinance Loan (IRRRL), also known as a VA Streamline Refinance: This is a simplified refinancing option designed to help veterans lower their interest rate or change from an adjustable-rate to a fixed-rate mortgage. It often requires less paperwork, no appraisal, and minimal underwriting. The funding fee for an IRRRL is typically lower at 0.5%.

- VA Cash-Out Refinance: This option allows veterans to take cash out of their home equity. It can be used to consolidate debt, make home improvements, or for other financial needs. A cash-out refinance typically requires a new appraisal and more extensive underwriting, and the funding fee is generally higher (e.g., 2.15% or 3.3% for repeat users with no down payment on the new loan).

Monitoring current VA interest rates is particularly important for those considering an IRRRL, as falling rates present an opportune moment to reduce monthly payments.

Tips for a Successful VA Loan Application

Embarking on the VA loan journey can seem daunting, but with proper preparation and understanding, it can be a smooth and rewarding experience.

Preparing Your Financial Documents

Before you even speak to a lender, gather essential financial documents. This includes your Certificate of Eligibility (COE), pay stubs, W-2s or tax returns (if self-employed), bank statements, and documentation of any other income or assets. Having these ready demonstrates preparedness and can expedite the application process. Lenders will also review your credit report and pull your FICO score.

Working with VA-Approved Lenders

Not all lenders offer VA loans, and among those that do, their expertise and service quality can vary significantly. Seek out lenders who specialize in VA loans, as they will be more familiar with the nuances of the program, understand veteran-specific financial situations, and can often provide a smoother experience. Ask about their experience, turnaround times, and customer reviews.

Common Pitfalls to Avoid

- Not Shopping Around: As emphasized, failing to compare offers from multiple lenders is a common and costly mistake.

- Ignoring Credit Issues: Address any credit report errors or late payments before applying to improve your rate prospects.

- Making Major Financial Changes: Avoid opening new credit accounts, taking out new loans, or making large purchases while your loan is in process, as this can negatively impact your debt-to-income ratio or credit score and jeopardize your approval.

- Misunderstanding the Funding Fee: Be aware of whether you are exempt from the funding fee and factor it into your calculations if you are not.

- Waiting Too Long: In a rising rate environment, procrastination can cost you. If rates are favorable, act decisively.

In conclusion, “what are VA interest rates today?” is a question with a dynamic answer. While specific rates fluctuate daily, the underlying principles remain constant. VA loans offer an exceptional pathway to homeownership for eligible service members and veterans. By understanding how rates are determined, diligently shopping for lenders, and preparing thoroughly, borrowers can leverage this invaluable benefit to secure a financially advantageous and lasting investment in their future. Staying informed about current market trends and working with knowledgeable professionals will be your best allies in navigating today’s VA loan landscape.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.