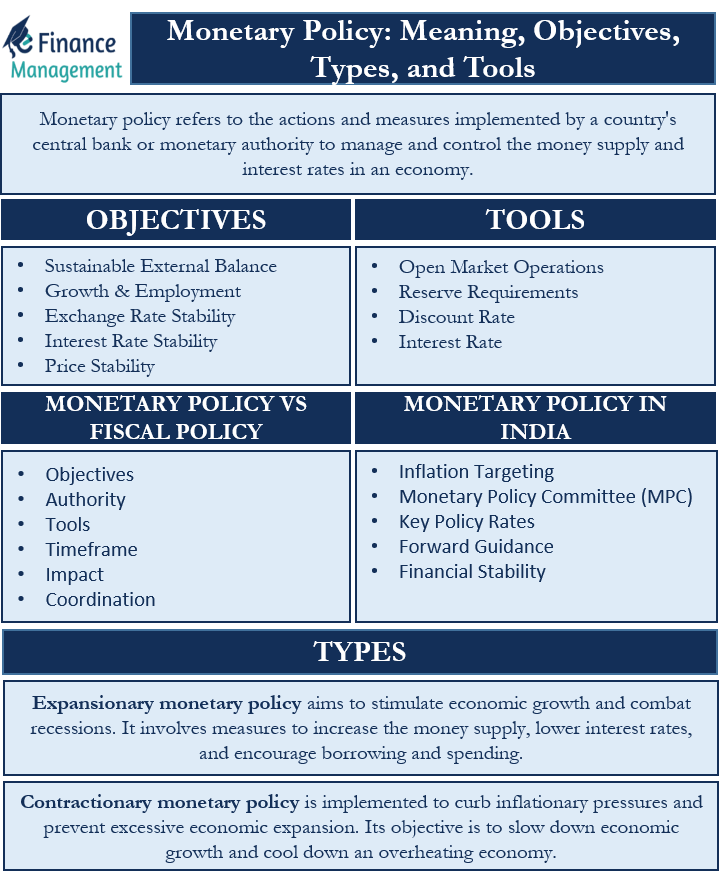

Monetary policy serves as the backbone of modern economic management. While the term often conjures images of complex spreadsheets and high-level meetings behind closed doors at the Federal Reserve or the European Central Bank, its application affects every facet of financial life. From the interest rate on your mortgage to the price of a gallon of milk, the “tools” used by central banks are the levers that steer the global economy.

In the pursuit of price stability and maximum sustainable employment, central banks do not simply hope for the best. Instead, they utilize a sophisticated toolkit designed to influence the supply and cost of money in an economy. Understanding these tools is essential for any investor, business owner, or student of finance seeking to navigate the ebits and flows of the market.

The Conventional Toolkit: Traditional Levers of Influence

For decades, monetary policy was defined by three primary instruments. These are often referred to as “conventional” tools, as they represent the standard methodology for adjusting the money supply in a stable economic environment.

Open Market Operations (OMO)

Open Market Operations are perhaps the most frequently used tool in a central bank’s arsenal. This process involves the buying and selling of government securities (such as Treasury bonds) in the open market. When a central bank wants to increase the money supply and lower interest rates, it buys bonds from commercial banks. This injects fresh liquidity into the banking system, giving banks more capital to lend to consumers and businesses. Conversely, to combat inflation and “mop up” excess liquidity, the central bank sells securities, effectively pulling money out of the system.

The Discount Rate

The discount rate is the interest rate charged to commercial banks and other depository institutions on loans they receive from their regional Federal Reserve Bank’s lending facility—the “discount window.” By raising the discount rate, the central bank makes it more expensive for banks to borrow money. This ripple effect eventually reaches the consumer, as banks raise their own lending rates to maintain profit margins. Lowering the discount rate has the opposite effect, encouraging borrowing and spending.

Reserve Requirements

Historically, central banks mandated that commercial banks hold a certain percentage of their deposits in reserve, either in their vaults or at the central bank. By lowering reserve requirements, the central bank allows banks to lend out a greater portion of their deposits, thereby increasing the money supply. Raising the requirement restricts lending. While this was once a primary tool, many modern central banks, including the Federal Reserve, have shifted toward a “zero-reserve” environment, relying instead on other mechanisms to control liquidity.

Interest on Reserve Balances (IORB)

In the modern era, particularly in the United States, the Interest on Reserve Balances (IORB) has become a primary tool. Instead of forcing banks to hold reserves via a mandate, the central bank pays interest on the funds banks choose to keep on deposit. By adjusting this rate, the central bank sets a “floor” for interest rates, as banks have no incentive to lend to the private market at a rate lower than what they can safely earn from the central bank.

Unconventional Monetary Policy: Navigating Extraordinary Times

When traditional tools reach their limits—such as when interest rates hit the “zero lower bound”—central banks must turn to unconventional methods. These strategies gained prominence following the 2008 financial crisis and were utilized extensively during the global pandemic.

Quantitative Easing (QE)

Quantitative Easing is a massive expansion of Open Market Operations. Instead of just buying short-term government bonds, the central bank purchases long-term securities, including mortgage-backed securities and corporate bonds. The goal of QE is to lower long-term interest rates and encourage investment in riskier assets like stocks and corporate debt. By flooding the system with liquidity, the central bank aims to jumpstart economic activity when lowering short-term rates is no longer an option.

Forward Guidance

Monetary policy is as much about psychology as it is about mathematics. Forward guidance is a communication tool where the central bank provides transparent information about its future policy intentions. By signaling that interest rates will remain low for an extended period, the central bank influences the long-term expectations of households and businesses. If a company knows rates will be low for three years, they are more likely to take out a loan for a new factory today.

Negative Interest Rates

In some economies, such as the Eurozone and Japan, central banks have experimented with negative interest rates. This essentially charges commercial banks for holding excess reserves. The intent is to “punish” banks for sitting on cash, thereby forcing them to lend it out to the public to stimulate the economy. While controversial, it remains a tool in the unconventional kit for fighting deflationary pressures.

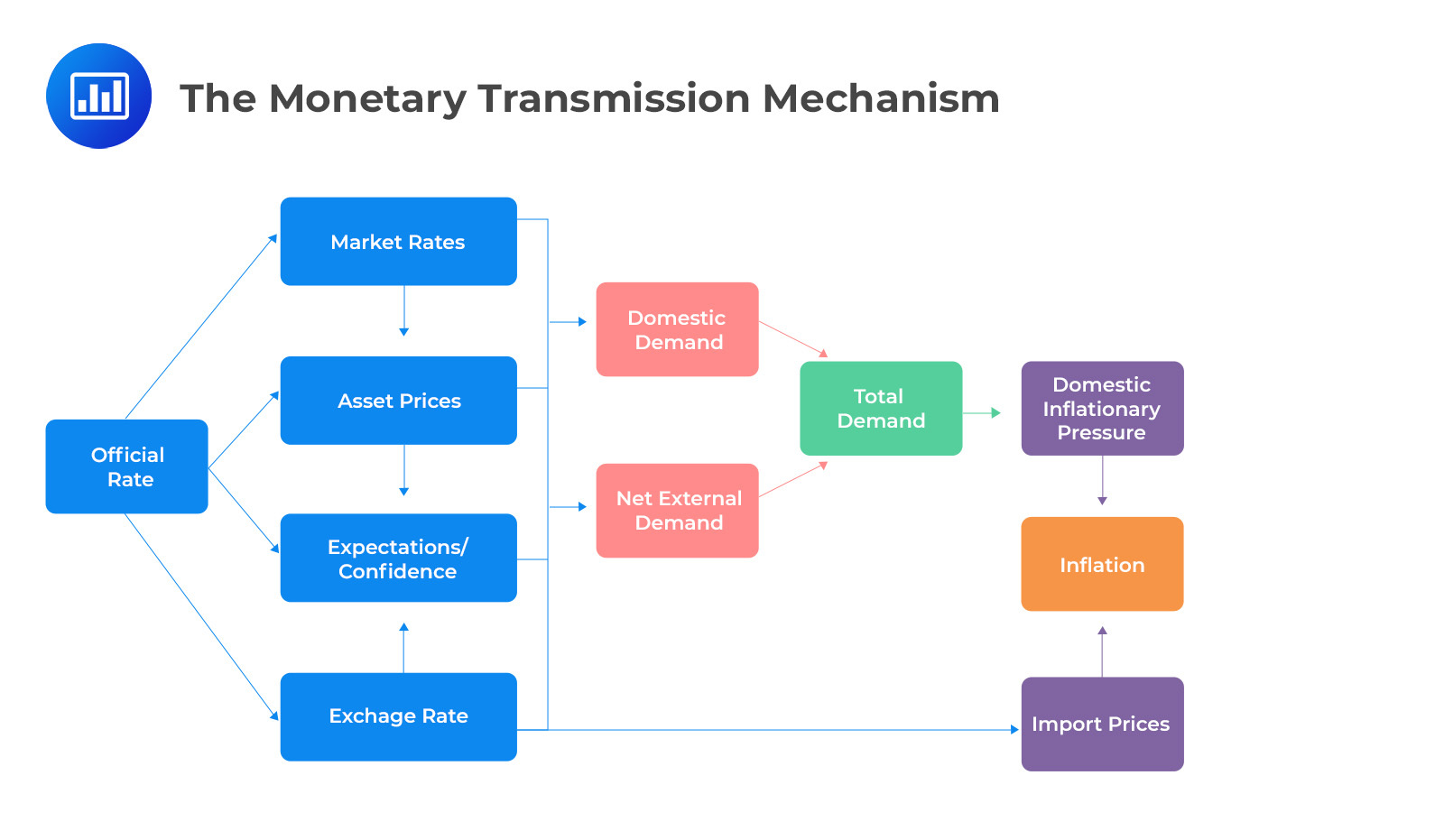

The Transmission Mechanism: How Policy Becomes Reality

Identifying the tools is only half the battle; understanding how these tools translate into real-world economic changes is vital. This process is known as the transmission mechanism of monetary policy.

Impact on Consumer Borrowing and Spending

The most immediate effect of monetary tool adjustment is seen in the credit markets. When the central bank lowers the target interest rate, the cost of car loans, credit cards, and mortgages typically falls. This increases the disposable income of households and encourages “big-ticket” purchases, which in turn drives demand for manufacturing and services.

Business Investment and Capital Allocation

For corporations, the cost of capital is a deciding factor in expansion. When monetary policy is “accommodative” (low rates), the hurdle rate for new projects decreases. Companies are more likely to issue bonds to fund research and development or to hire more staff. In a “tight” monetary environment (high rates), businesses often pivot toward cost-cutting and capital preservation, slowing the overall pace of economic growth to prevent overheating.

The Wealth Effect and Asset Prices

Monetary policy tools have a profound impact on asset valuations. Low interest rates make fixed-income investments like savings accounts less attractive, pushing investors toward the stock market and real estate. This rise in asset prices creates a “wealth effect,” where consumers feel more financially secure because their portfolios or home values have increased, leading to higher levels of discretionary spending.

The Challenges and Limitations of Monetary Tools

Despite the precision with which central banks attempt to operate, monetary policy is not a panacea. There are inherent challenges that can blunt the effectiveness of even the most well-deployed tools.

The Problem of Policy Lags

Monetary policy is often described as “steering a large ship.” When the captain turns the wheel, the ship doesn’t move instantly. There is a significant time lag—often 12 to 18 months—between a change in interest rates and its full effect on inflation and employment. This delay creates the risk of “overshooting,” where a central bank keeps rates too high for too long, accidentally triggering a recession.

Supply-Side Shocks

Monetary tools are designed to manage “demand.” By making money cheaper or more expensive, central banks influence how much people want to buy. However, monetary policy is largely ineffective against supply-side shocks, such as a global oil shortage or a broken supply chain. If the price of goods is rising because there simply aren’t enough of them, raising interest rates may stop people from buying, but it won’t produce more goods.

The Liquidity Trap

A liquidity trap occurs when consumers and investors lose confidence to such a degree that they hoard cash regardless of how low interest rates go. In this scenario, the central bank’s tools become “pushing on a string.” No matter how much liquidity is injected into the system, it fails to circulate, rendering traditional monetary policy temporarily powerless.

Conclusion: The Evolving Science of Money

The tools of monetary policy represent a bridge between theoretical economics and the practical reality of financial markets. From the foundational mechanics of Open Market Operations to the modern complexities of Quantitative Easing and Forward Guidance, these instruments allow central banks to act as the “lender of last resort” and the “stabilizer of first resort.”

For the individual participant in the economy, recognizing these tools provides a roadmap for financial planning. When the central bank signals a shift toward tightening, it is a cue to brace for higher borrowing costs and potentially volatile asset prices. When they lean toward accommodation, it often signals an environment ripe for investment and expansion. While the tools may evolve with technology and shifting global dynamics, their core purpose remains the same: maintaining the delicate balance of the machine we call the economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.