For many Americans, the annual ritual of filing taxes is accompanied by a nagging sense of anxiety. Even for those who strive for absolute accuracy, the specter of the Internal Revenue Service (IRS) looms large. The word “audit” often conjures images of stern agents sifting through shoeboxes of faded receipts in a windowless room. However, the reality of modern tax enforcement is far more nuanced, driven by sophisticated algorithms and specific financial triggers.

Understanding the statistical likelihood of an audit, as well as the mechanisms the IRS uses to select returns, is essential for any taxpayer—whether you are a salaried employee, a high-net-worth investor, or a small business owner. In this guide, we will break down the current odds of being audited, the red flags that attract unwanted attention, and the financial strategies you can employ to ensure your filings remain beyond reproach.

Understanding the Statistical Reality of IRS Audits

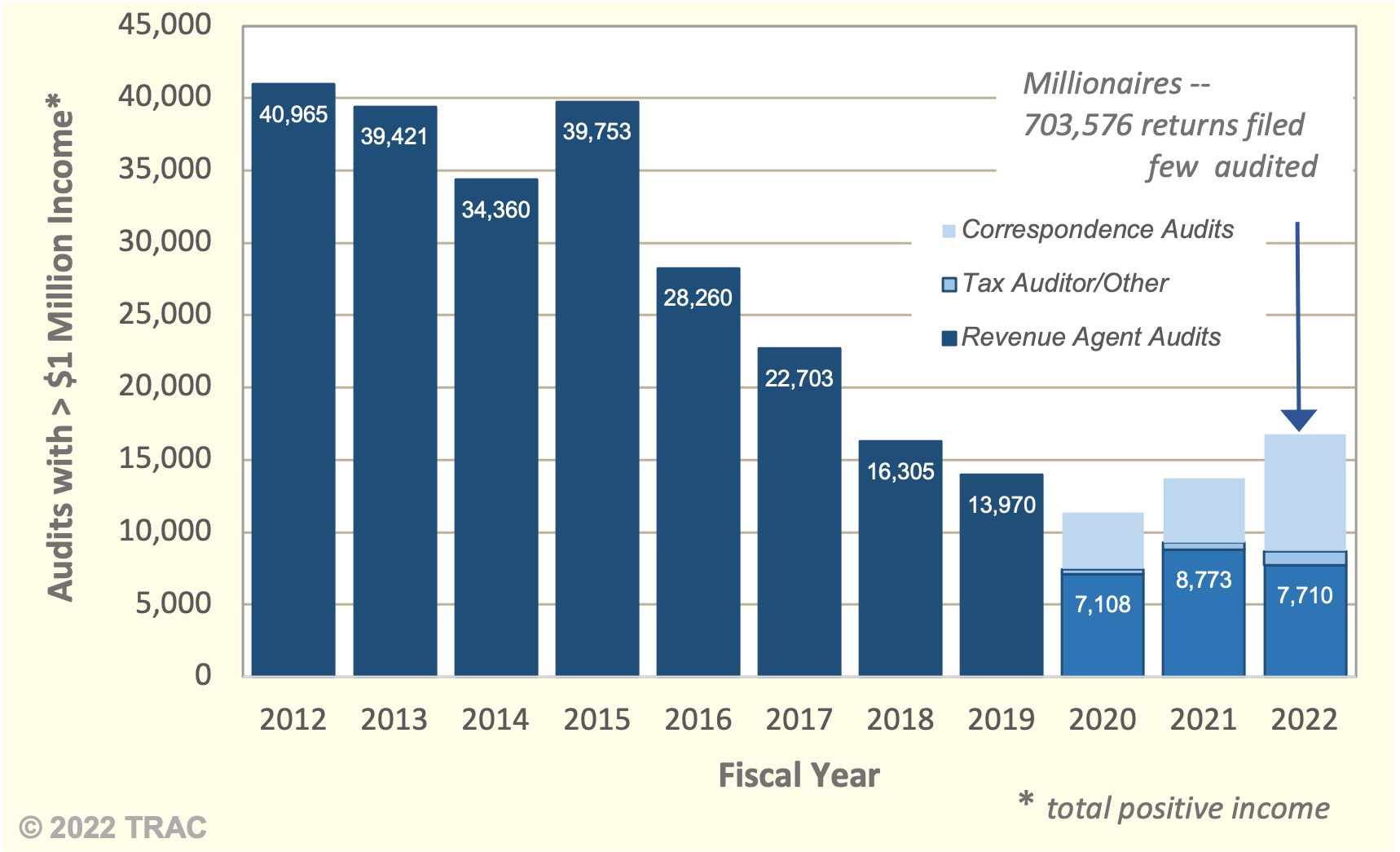

In the world of personal finance, perception rarely aligns with reality regarding the IRS. While the fear of an audit is widespread, the actual frequency of audits has been on a steady decline for over a decade. This decline is largely attributed to budget constraints and a shrinking workforce at the IRS, although recent legislative changes are beginning to shift this trajectory.

General Audit Rates Across All Taxpayers

Statistically speaking, the vast majority of individual taxpayers have a very low risk of being audited. According to the most recent IRS Data Books, the overall audit rate for individual income tax returns typically hovers around 0.4% to 0.5%. This means that roughly 1 out of every 200 to 250 taxpayers will face some form of examination.

However, this “average” is misleading because the IRS does not select returns at random in a vacuum. The agency utilizes a “risk-based” approach, concentrating its limited resources on returns that have the highest potential for significant tax changes. If you are a standard W-2 employee with modest investments and no complex business deductions, your individual odds are likely even lower than the national average.

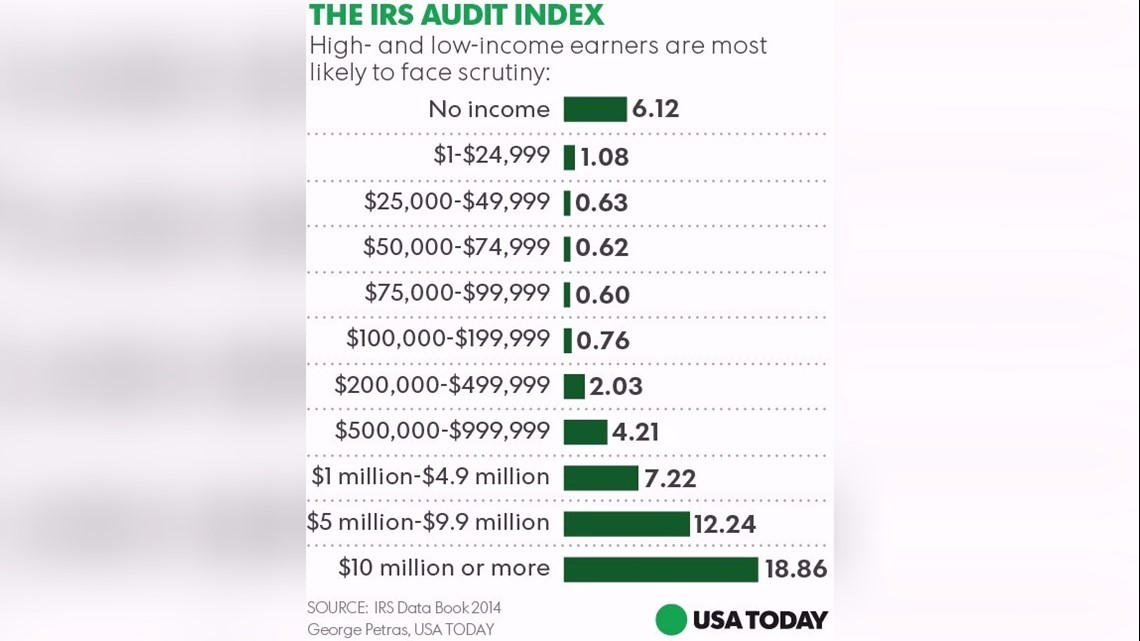

How Income Levels Influence Your Odds

The most significant factor in determining audit probability is your total positive income. The IRS data consistently shows a “U-shaped” curve regarding audit rates.

On one end of the spectrum, taxpayers claiming the Earned Income Tax Credit (EITC) face higher audit rates—often closer to 1%—because the IRS prioritizes preventing “improper payments” in social program credits. On the other end, the odds increase dramatically as income rises. For those earning between $100,000 and $500,000, the audit rate remains relatively low. However, for individuals earning over $1 million, the odds can jump to 1% or 2%. For the “ultra-wealthy” earning over $10 million annually, the audit rate has historically reached as high as 8% to 10%, as these returns often involve complex offshore accounts, tiered partnerships, and sophisticated tax shelters.

Red Flags: What Triggers an IRS Audit?

The IRS uses a computer system called the Discriminant Function System (DIF) to score every tax return. The higher the score, the higher the likelihood that an audit will result in a change to the tax liability. While the exact formulas of the DIF remain a guarded secret, financial experts have identified several recurring “red flags” that consistently drive up a taxpayer’s score.

Discrepancies in Reported Income

The most common reason for an IRS inquiry is a simple mismatch of data. The IRS receives copies of every W-2 and 1099 form issued to you. If you forget to report a $500 1099-INT from a high-yield savings account or a 1099-NEC from a side hustle, the IRS’s Automated Underreporter (AUR) system will flag the discrepancy immediately. This usually results in a “correspondence audit,” where the IRS sends a letter (Notice CP2000) proposing an adjustment. Ensuring that your tax return perfectly matches the documents reported by third parties is the single best way to avoid an inquiry.

Business vs. Personal Expenses and Schedule C Filers

Sole proprietors and freelancers who file a Schedule C are under a higher level of scrutiny than traditional employees. The IRS is particularly wary of “hobby losses”—situations where a taxpayer claims business deductions for an activity that does not have a clear profit motive.

Furthermore, excessive deductions for meals, travel, and entertainment are frequent triggers. If your business expenses seem disproportionately high compared to your gross income—for instance, claiming $40,000 in expenses on $50,000 of revenue—the IRS may want to verify that those expenses were “ordinary and necessary” for your trade. Home office deductions, while perfectly legal, also require strict adherence to the rule that the space must be used exclusively for business.

High-Value Transactions and Foreign Assets

In the modern financial landscape, the IRS has increased its focus on cryptocurrency and international holdings. If you checked the box on your Form 1040 indicating you engaged in virtual currency transactions but failed to report any capital gains or losses, you are inviting an audit. Similarly, failing to file an FBAR (Report of Foreign Bank and Financial Accounts) if you have more than $10,000 in foreign accounts is a major red flag that carries heavy penalties.

The Evolution of IRS Enforcement and “The Tax Gap”

The landscape of IRS audits is currently undergoing a significant transformation. Following the passage of the Inflation Reduction Act, the IRS received a massive infusion of funding—approximately $80 billion over ten years—specifically earmarked for modernization and enforcement.

Closing the “Tax Gap”

The “Tax Gap” is the difference between what taxpayers owe and what they actually pay on time. The IRS estimates this gap to be over $600 billion annually. To close this, the agency is investing heavily in Artificial Intelligence (AI) and data analytics. These tools allow the IRS to identify complex patterns of tax avoidance in large partnerships and hedge funds that were previously too labor-intensive to investigate. For the average taxpayer, this means that while the number of audits may not skyrocket overnight, the accuracy of the IRS’s targeting will likely improve.

Targeted Programs and Random Selection

While most audits are triggered by specific data points, a small percentage are part of the National Research Program (NRP). These are “line-by-line” audits where every single entry on a return must be substantiated. The NRP audits are conducted to help the IRS update its DIF scoring system. Essentially, these are “random” audits used for statistical research, and unfortunately, there is little a taxpayer can do to avoid them other than maintaining impeccable records.

Strategic Preparation: Reducing Your Risk and Improving Compliance

Audit protection is not about “hiding” information; it is about transparency, documentation, and professional diligence. By treating your taxes as a core component of your financial strategy, you can minimize the stress associated with potential IRS inquiries.

Documentation and Record-Keeping Best Practices

The burden of proof in an audit lies with the taxpayer. If you claim a deduction, you must be able to prove it. For business owners, this means keeping digital copies of receipts, mileage logs, and contracts for at least three to seven years. In the eyes of the IRS, if it isn’t documented, it didn’t happen. Utilizing financial software to categorize expenses in real-time can prevent the “tax season scramble” and ensure that your deductions are defensible.

The Role of Professional Tax Advice

As your financial life grows in complexity—adding rental properties, stock options, or K-1 income from partnerships—the value of a Certified Public Accountant (CPA) or Enrolled Agent (EA) increases. A tax professional does more than just fill out forms; they provide a layer of “due diligence.” They can spot anomalies that might trigger a DIF flag and advise you on how to disclose certain positions to the IRS to avoid penalties. Furthermore, having a professional represent you during an audit can significantly reduce the emotional and administrative burden.

Dealing with an Audit: Process and Outcomes

If you do receive an audit notice, it is important to remain calm and understand that most audits are resolved without any legal drama. The IRS is a bureaucracy, and following their process is the fastest way to a resolution.

Correspondence Audits vs. Field Audits

About 75% of audits are “correspondence audits,” conducted entirely through the mail. These usually focus on one or two specific items, like charitable contributions or educational credits. You simply mail in the requested documentation, and the case is closed.

“Field audits,” where an agent visits your home or place of business, are much rarer and reserved for complex corporate or high-net-worth individual returns. In these cases, it is highly recommended to have a tax attorney or CPA handle all communications with the agent to ensure your rights are protected.

Your Rights as a Taxpayer

Every taxpayer has the right to be treated professionally by IRS employees and the right to appeal an IRS decision. If you disagree with the findings of an audit, you can take your case to the IRS Appeals Office or even to U.S. Tax Court. Knowing your rights—often referred to as the “Taxpayer Bill of Rights”—is a crucial part of managing your financial health.

Conclusion: Knowledge as a Financial Tool

While the odds of an IRS audit remain statistically low for the average American, the impact of an audit can be significant if you are unprepared. The best defense against an audit is not fear, but a proactive approach to personal finance. By understanding the “red flags,” maintaining rigorous documentation, and staying informed about changing tax laws, you can file your returns with confidence. Ultimately, a well-prepared tax return is more than just a legal requirement; it is a reflection of a disciplined and strategic approach to your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.