In the complex ecosystem of personal finance, few variables exert as much influence over a household’s long-term wealth as mortgage rates. For the average homebuyer or real estate investor, a fraction of a percentage point can represent tens of thousands of dollars in interest over the life of a loan. Understanding “what the mortgage rates are today” requires more than a simple glance at a daily ticker; it demands an analysis of macroeconomic trends, central bank policies, and individual financial health.

As we navigate a period of significant economic transition, the cost of borrowing has become a focal point for anyone looking to enter the housing market or optimize their existing debt. This guide provides a deep dive into the mechanisms that drive mortgage rates, the current state of the market, and how you can position yourself to secure the most favorable terms possible.

Factors Influencing Today’s Mortgage Rates

Mortgage rates do not exist in a vacuum. They are the product of a delicate balance between global economic data, domestic policy, and investor sentiment. While many consumers believe the Federal Reserve sets mortgage rates directly, the reality is more nuanced.

The Role of the Federal Reserve and Monetary Policy

The Federal Reserve influences mortgage rates primarily through the Federal Funds Rate—the interest rate at which commercial banks borrow and lend to one another overnight. When the Fed raises rates to combat inflation, the cost of capital increases across the board. While this does not dictate mortgage rates on a one-to-one basis, it sets the floor for consumer lending. When the Fed signals a “hawkish” stance (maintaining or raising rates), mortgage lenders typically price in that risk, leading to higher rates for borrowers.

Inflation and the 10-Year Treasury Yield

Inflation is the greatest enemy of fixed-income investments like mortgage-backed securities (MBS). If inflation is high, the purchasing power of the future interest payments a lender receives is eroded. Consequently, investors demand higher yields to compensate for this risk. Historically, mortgage rates track the movement of the 10-year Treasury note yield very closely. Usually, there is a “spread” of about 1.5 to 2 percentage points between the 10-year Treasury yield and the average 30-year fixed mortgage rate. When market volatility is high, this spread can widen, pushing mortgage rates even higher.

Housing Market Supply and Demand

The secondary market for mortgages also plays a critical role. Most mortgages are packaged into securities and sold to investors. If there is high demand for these securities, rates can remain lower. Conversely, if investors are wary of the housing market or if there is an oversupply of mortgage debt, rates must rise to attract buyers for that debt.

Understanding Different Mortgage Products

When asking about today’s rates, it is essential to specify which product you are considering. Not all mortgages are created equal, and the rate you see advertised may not apply to every loan structure.

The 30-Year Fixed-Rate Mortgage

The 30-year fixed-rate mortgage remains the gold standard for American homebuyers. Its primary advantage is stability; your principal and interest payment remain identical for 360 months. Because the lender is taking on the risk of inflation and interest rate fluctuations for three decades, these loans typically carry higher interest rates than shorter-term or variable-rate products.

The 15-Year Fixed-Rate Mortgage

For those looking to build equity quickly and save on interest, the 15-year fixed-rate mortgage is a powerful financial tool. Because the loan term is shorter, the lender’s risk is reduced, allowing them to offer a significantly lower interest rate—often 0.5% to 1% lower than the 30-year counterpart. However, the trade-off is a much higher monthly payment, which can strain a household’s monthly cash flow.

Adjustable-Rate Mortgages (ARMs)

In a high-rate environment, Adjustable-Rate Mortgages often regain popularity. An ARM typically offers a lower “teaser” rate for an initial period (such as 5, 7, or 10 years). After that period, the rate adjusts annually based on a market index. For borrowers who plan to sell or refinance before the initial period ends, an ARM can provide substantial savings. However, they carry the inherent risk of payments increasing significantly in the future.

Strategies to Secure the Lowest Possible Rate

While you cannot control the global economy, you can control your financial profile. Lenders reserve their “best” rates—the ones you see in headlines—for borrowers who present the least amount of risk.

Optimizing Your Credit Score

Your credit score is the single most important factor in determining the rate a lender will offer you. There is often a massive pricing tier difference between a borrower with a 680 score and one with a 760 score. To secure the lowest rates, focus on reducing credit card utilization, ensuring every payment is on time, and avoiding new credit inquiries in the months leading up to a mortgage application.

The Power of a Substantial Down Payment

The Loan-to-Value (LTV) ratio is a key metric for lenders. If you put 20% down, you are seen as a much safer bet than someone putting 3.5% down. Not only does a larger down payment help you secure a lower interest rate, but it also eliminates the need for Private Mortgage Insurance (PMI), which further reduces your monthly financial burden.

Shopping Multiple Lenders and Using Points

Many borrowers make the mistake of only checking with their primary bank. However, mortgage rates can vary significantly between retail banks, credit unions, and online mortgage brokers. Furthermore, you can “buy down” your rate using discount points. One point typically costs 1% of the loan amount and reduces your interest rate by approximately 0.25%. This is an upfront investment that can pay off handsomely if you plan to stay in the home for a long time.

The Financial Mathematics of Interest Rates

To truly understand why today’s rates matter, one must look at the long-term mathematical impact on wealth. Even a 1% difference in a mortgage rate can alter a family’s financial trajectory.

The Total Cost of Interest

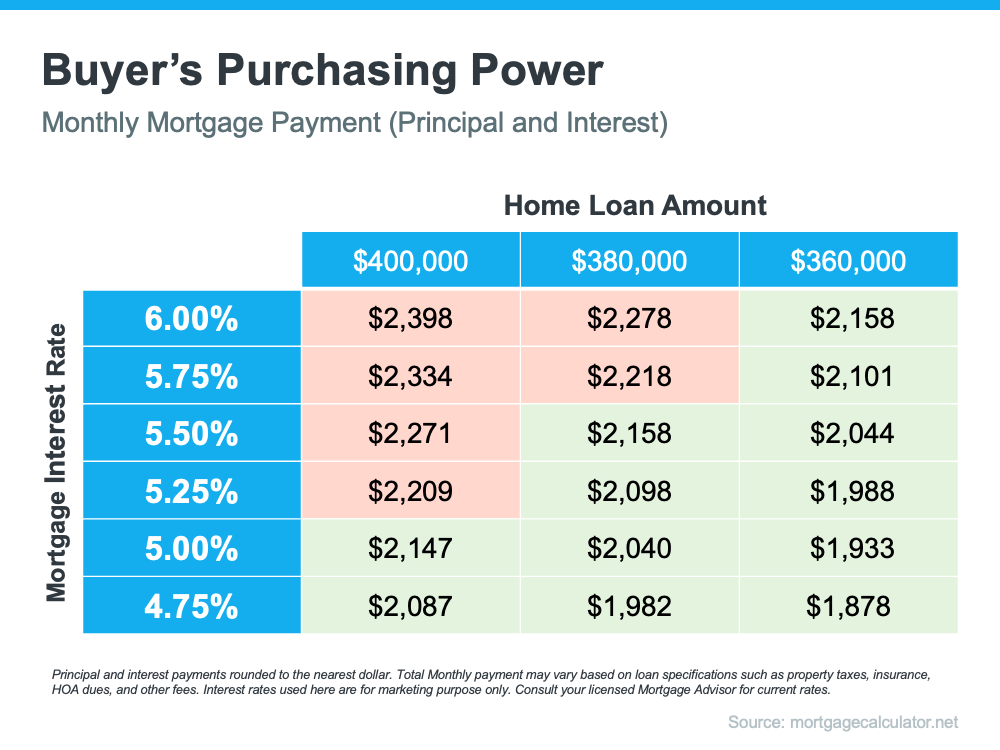

Consider a $400,000 loan. At a 4% interest rate, the total interest paid over 30 years is approximately $287,000. At a 7% interest rate, that total interest jumps to over $558,000. That is a difference of $271,000—money that could have been directed toward retirement accounts, a child’s education, or other investment vehicles. This illustrates why “timing” the market or focusing on rate reduction is a cornerstone of savvy personal finance.

The Concept of “Marry the House, Date the Rate”

A common phrase in the real estate industry is “marry the house, date the rate.” This philosophy suggests that if you find the right property, you should purchase it even if rates are high, with the intention of refinancing later when rates drop. While this can be a valid strategy, it requires a “Money” mindset: you must ensure you can afford the current payment indefinitely, as there is no guarantee that rates will fall within a specific timeframe.

Economic Outlook: Navigating Volatility in the Mortgage Market

Looking ahead, the trajectory of mortgage rates will be dictated by the “higher for longer” sentiment regarding interest rates. As the economy seeks an equilibrium between growth and controlled inflation, prospective homeowners must be prepared for continued volatility.

Why Waiting Isn’t Always the Best Strategy

Many potential buyers sit on the sidelines waiting for rates to return to the historic lows of 2020-2021. However, if rates drop, the sudden influx of buyers can lead to increased competition and skyrocketing home prices. Often, the increase in the home’s purchase price can outweigh the savings from a lower interest rate. A sound financial strategy involves looking at the “all-in” cost and determining if the monthly payment fits within a conservative 25-30% of your gross income.

Monitoring Economic Indicators

To stay ahead of the curve, keep an eye on the Consumer Price Index (CPI) reports and the monthly Jobs Report. If inflation shows signs of cooling faster than expected, mortgage rates often react positively (dropping) before the Federal Reserve even meets. Being “market-ready” means having your pre-approval in hand so you can lock in a rate the moment a favorable dip occurs.

Conclusion

What are the mortgage rates today? They are a reflection of the current pulse of the global economy and a critical benchmark for your personal financial health. By understanding the factors that move the needle, choosing the right loan product, and optimizing your personal finances, you can navigate this high-stakes environment with confidence. Remember, a mortgage is not just a debt; it is a structured financial tool that, when managed correctly, serves as the foundation for long-term stability and wealth creation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.