Navigating the landscape of car insurance can often feel like a complex puzzle. With countless providers vying for your business, each promising competitive rates, the quest to find the “cheapest” car insurance is a common priority for budget-conscious consumers. However, the term “cheapest” is profoundly subjective in the insurance world; what’s affordable for one driver might be prohibitively expensive for another. This comprehensive guide aims to demystify the process, helping you understand the factors that drive insurance costs, explore top strategies for reducing your premiums, and identify major players often associated with competitive rates, empowering you to make an informed financial decision.

Car insurance is not just a legal requirement in most places; it’s a vital financial safety net designed to protect you from the potentially devastating costs associated with accidents, theft, or other unforeseen incidents involving your vehicle. While prioritizing affordability is smart financial planning, it’s crucial not to compromise on adequate coverage. The true value lies in finding the optimal balance between cost and comprehensive protection, ensuring you’re prepared for whatever the road may bring without overspending.

Understanding the Dynamics of Car Insurance Pricing

Before diving into specific companies or strategies, it’s essential to grasp the fundamental mechanics behind how car insurance premiums are calculated. Insurance companies are masters of risk assessment, using a sophisticated array of data points to predict the likelihood of you filing a claim and how much that claim might cost them.

Factors Influencing Your Premium

Your individual circumstances and choices significantly impact the rate you’re offered. Here are the primary factors insurers consider:

- Driver’s Age and Experience: Younger, less experienced drivers (especially teenagers) are statistically more prone to accidents, leading to higher premiums. Rates generally decrease as drivers mature and gain more experience.

- Driving Record: This is paramount. A clean record free of accidents, speeding tickets, or other moving violations will always result in lower rates. Conversely, a history of infractions or claims will drive up your premium significantly.

- Vehicle Type: The make, model, year, safety features, and even the color of your car matter. Expensive, high-performance, or frequently stolen vehicles cost more to insure due to higher repair costs, greater liability risk, or increased theft risk.

- Location (Garaging Address): Where you live and park your car plays a crucial role. Urban areas with higher traffic density, crime rates, or a greater incidence of natural disasters typically have higher premiums than rural areas.

- Credit Score (in most states): Insurers often use a credit-based insurance score as a predictor of how likely you are to file a claim. A good credit score can lead to lower premiums, while a poor one can lead to higher costs.

- Coverage Limits and Deductibles: The amount of coverage you choose (liability, collision, comprehensive) and your deductible amount directly impact your premium. Higher deductibles (the amount you pay out-of-pocket before insurance kicks in) generally lead to lower premiums, and vice-versa.

- Annual Mileage: Drivers who log fewer miles annually are often seen as lower risk, potentially qualifying for discounts.

- Marital Status: Married individuals are statistically less likely to file claims than single drivers, often resulting in slightly lower rates.

The Myth of a Single “Cheapest” Company

It’s a common misconception that there is one universal “cheapest car insurance company” for everyone. Because premiums are so highly individualized, a company that offers the lowest rate to your neighbor might be significantly more expensive for you, and vice versa. Each insurance provider uses its own proprietary algorithms and risk assessment models, which weigh these factors differently.

Therefore, the quest for the “cheapest” isn’t about finding a single company but rather finding the company that offers you the most competitive rate based on your specific profile. This necessitates a proactive and personalized approach rather than a one-size-fits-all expectation.

Top Strategies for Finding Affordable Car Insurance

Finding genuinely affordable car insurance requires diligence and a strategic approach. It’s not enough to simply pick the first company you see; rather, it involves careful comparison and optimization of your policy.

Shop Around and Compare Quotes Extensively

This is arguably the most impactful strategy. Do not settle for the first quote you receive. Insurance rates can vary by hundreds, even thousands, of dollars between providers for the exact same coverage.

- Utilize Online Comparison Tools: Websites like The Zebra, QuoteWizard, or Bankrate can provide multiple quotes simultaneously by inputting your information once. While these are a great starting point, they may not include every single insurer.

- Directly Contact Insurers: Reach out to major national carriers (e.g., Geico, Progressive, State Farm, Allstate) as well as smaller regional ones. Many companies offer online quote tools directly on their websites.

- Work with Independent Agents: An independent insurance agent works with multiple insurance companies and can shop around on your behalf, often finding deals you might miss. They can also offer personalized advice. Aim to get at least 3-5 quotes to ensure you’re getting a comprehensive view of the market.

Leverage Available Discounts

Insurance companies offer a wide array of discounts that can significantly reduce your premium. It’s crucial to inquire about every possible discount you might qualify for.

- Bundling Discounts: Combine your car insurance with other policies (homeowners, renters, life insurance) from the same provider. This is often one of the most substantial discounts.

- Good Driver/Accident-Free Discounts: Reward for maintaining a clean driving record over a certain period (e.g., 3-5 years).

- Good Student Discounts: For young drivers who maintain a B average or higher.

- Low Mileage Discounts: For those who drive less than a specified number of miles annually, often verified by telematics devices.

- Multi-Car Discounts: Insuring multiple vehicles under the same policy.

- Anti-Theft Device Discounts: For vehicles equipped with approved alarm systems or tracking devices.

- Defensive Driver Course Discounts: Completing an approved defensive driving course can sometimes lower your rates, especially for older drivers or those with minor infractions.

- Payment Discounts: Paying your premium in full, opting for automatic payments, or choosing paperless billing can all lead to small but cumulative savings.

- Professional/Affiliation Discounts: Some companies offer discounts to members of certain professional organizations, alumni associations, or employee groups.

Optimize Your Coverage Wisely

While cutting coverage to save money can be tempting, it’s vital to ensure you maintain adequate protection. However, there are smart ways to adjust your policy.

- Increase Your Deductible: If you have a solid emergency fund, increasing your collision and comprehensive deductibles (e.g., from $500 to $1,000) can substantially lower your monthly premium. Just ensure you can comfortably afford the deductible should you need to file a claim.

- Re-evaluate Comprehensive and Collision for Older Cars: For older vehicles with low market value, the cost of comprehensive and collision coverage might outweigh the potential payout after an accident. Consider dropping these coverages if your car is worth less than a few thousand dollars.

- Understand Required vs. Optional Coverage: Know your state’s minimum liability requirements. While meeting the minimum is the cheapest option, it often provides insufficient protection in a serious accident. However, review optional coverages like roadside assistance or rental car reimbursement; if you already have these through another service (e.g., credit card, auto club), you might not need them on your policy.

Improve Your Driver Profile Over Time

Some of the most significant savings come from being a responsible driver and managing your financial health.

- Maintain a Clean Driving Record: This cannot be stressed enough. Avoid accidents and traffic violations at all costs. Over time, a spotless record will unlock the best rates.

- Improve Your Credit Score: If your state allows the use of credit-based insurance scores, working on improving your overall credit health can lead to lower premiums. Pay bills on time, reduce debt, and monitor your credit report for errors.

- Enroll in Telematics Programs: Many insurers offer programs (like Progressive’s Snapshot or Geico’s DriveEasy) that monitor your driving habits (speed, braking, mileage). Safe drivers can earn significant discounts.

Exploring Major Insurance Providers Known for Competitive Rates

While the “cheapest” company is subjective, certain providers are consistently recognized for offering competitive rates to a broad spectrum of drivers. It’s always worth getting a quote from these companies.

National Giants and Their Offerings

These large insurers dominate the market and often have the resources to offer a variety of discounts and competitive pricing, though their rates can vary wildly depending on the individual.

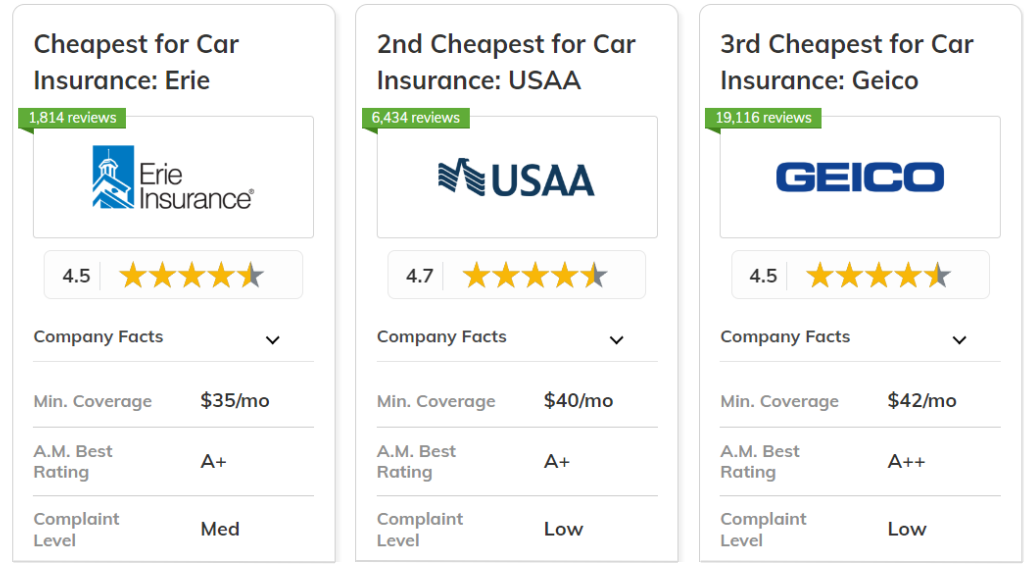

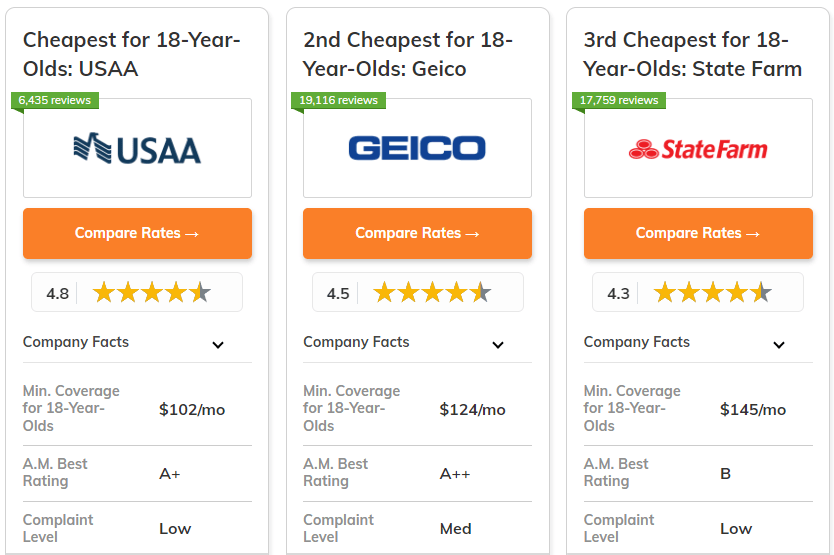

- Geico: Frequently cited for its competitive pricing, especially for drivers with good records. Geico operates primarily online and over the phone, which helps keep overhead costs lower. They are known for a wide array of discounts.

- Progressive: Another online-focused giant, Progressive is well-known for its Name Your Price® tool and Snapshot® program, which allows safe drivers to earn discounts based on their actual driving habits. They cater to a broad range of drivers.

- State Farm: While often perceived as having local agents, State Farm remains a significant competitor. They are known for strong customer service and often offer good rates when bundled with other policies.

- Allstate: With a vast network of agents, Allstate provides personalized service and various discounts. Their rates can be competitive, particularly for those who bundle policies.

- USAA: Exclusively available to military members, veterans, and their families, USAA consistently receives top ratings for customer satisfaction and often offers some of the lowest rates in the industry. If you’re eligible, they are a must-check.

- Farmers: Offers a wide range of coverage options and discounts, with a strong focus on personalized service through agents.

- Liberty Mutual: Known for customized coverage options and various discounts, including for online quotes and early shopping.

Regional and Niche Insurers

Don’t overlook smaller or specialized insurance companies. Sometimes, a regional insurer might have a better understanding of local risks and offer more favorable rates than a national giant. Similarly, some companies specialize in certain demographics (e.g., high-risk drivers, classic car owners) and can offer competitive pricing within their niche. Examples include Erie Insurance (Mid-Atlantic/Midwest), The General (for high-risk drivers), or Esurance (an online-focused option, part of Allstate).

Online-First Insurers

Companies that primarily operate online often have lower overhead costs, which they can pass on to consumers in the form of lower premiums. Beyond Geico and Progressive, look into newer online-only players that might disrupt the market with aggressive pricing.

Navigating the Quote Process and Making Your Decision

Getting quotes is just the first step. Understanding what information you’ll need and what other factors to consider beyond just the price tag are critical for making a smart, long-term decision.

Essential Information You’ll Need

To get accurate quotes, have the following information ready:

- Personal Information: Your full name, date of birth, address, marital status, driver’s license number, and social security number (optional, but helps with credit checks).

- Vehicle Information: Year, make, model, VIN (Vehicle Identification Number), current mileage, and primary use (commute, pleasure, business).

- Driving History: Details on any past accidents, traffic violations, or claims for all drivers on the policy.

- Desired Coverage: Understand the types and limits of coverage you want (liability, collision, comprehensive, etc.) and your preferred deductibles.

Beyond the Price Tag: What Else to Consider?

While price is a major factor, it shouldn’t be the only one. A cheap policy from an unreliable insurer can be more costly in the long run.

- Customer Service and Support: How easy is it to get in touch with a representative? Are they responsive and helpful? Check customer reviews and ratings from organizations like J.D. Power and Associates or the Better Business Bureau.

- Claims Process Efficiency: This is where an insurer truly proves its worth. How quickly and fairly do they process claims? A smooth and timely claims experience is invaluable after an accident.

- Financial Stability: Ensure the company is financially sound and able to pay out claims. Ratings from agencies like A.M. Best or Standard & Poor’s can provide this insight.

- Online Tools and Mobile Apps: For tech-savvy individuals, a robust online portal and user-friendly mobile app for managing policies, paying bills, and filing claims can be a significant convenience factor.

Reviewing Your Policy Annually

Insurance rates are not static. They can change based on market conditions, your driving record, or even your insurer’s risk assessment models. It’s a best practice to:

- Review your policy details annually to ensure your coverage still meets your needs.

- Shop around for new quotes at least once a year, especially if you’ve had significant life changes (moved, got married, bought a new car, had a birthday). Loyalty doesn’t always pay off in the insurance world; new customer discounts can often be more attractive.

Conclusion

Finding the cheapest car insurance company is a highly personalized endeavor that demands research, comparison, and a strategic approach. There is no single answer that fits everyone, as rates are profoundly influenced by individual factors such as your age, driving history, vehicle type, location, and desired coverage.

By understanding how premiums are calculated, diligently shopping around for multiple quotes, leveraging every available discount, and optimizing your coverage without sacrificing essential protection, you can significantly reduce your car insurance costs. Remember to look beyond just the price; consider the insurer’s customer service reputation, claims process efficiency, and financial stability. By actively managing your car insurance, you ensure you’re both adequately protected and financially savvy, paving the way for substantial savings in your personal finance journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.