In the complex and ever-evolving landscape of healthcare, the efficient and cost-effective management of essential supplies is paramount. Among the most fundamental and widely used resources are intravenous (IV) fluids. While their clinical necessity is undisputed, for healthcare administrators, financial officers, and procurement specialists, understanding the different types of IV fluids extends beyond their therapeutic applications to encompass crucial financial considerations. The selection, procurement, storage, and administration of these fluids represent a significant portion of a healthcare facility’s operating budget. Therefore, a thorough comprehension of the three primary categories of IV fluids – crystalloids, colloids, and blood products – is not only a clinical imperative but also a strategic financial decision-making tool. This article will delve into these three main types of IV fluids from a business finance perspective, examining their characteristics, cost implications, and the strategic decisions that influence their use within a healthcare organization.

The Financial Significance of IV Fluid Categories

The vast array of IV fluids available can be broadly categorized into three main types, each with distinct compositions, mechanisms of action, and, consequently, varying cost profiles. Recognizing these differences is the first step in optimizing procurement, inventory management, and ultimately, patient care costs. For healthcare businesses, this understanding translates into informed purchasing strategies, risk mitigation related to stockouts or overstocking, and the potential for significant savings.

Crystalloids: The Workhorses of Fluid Management

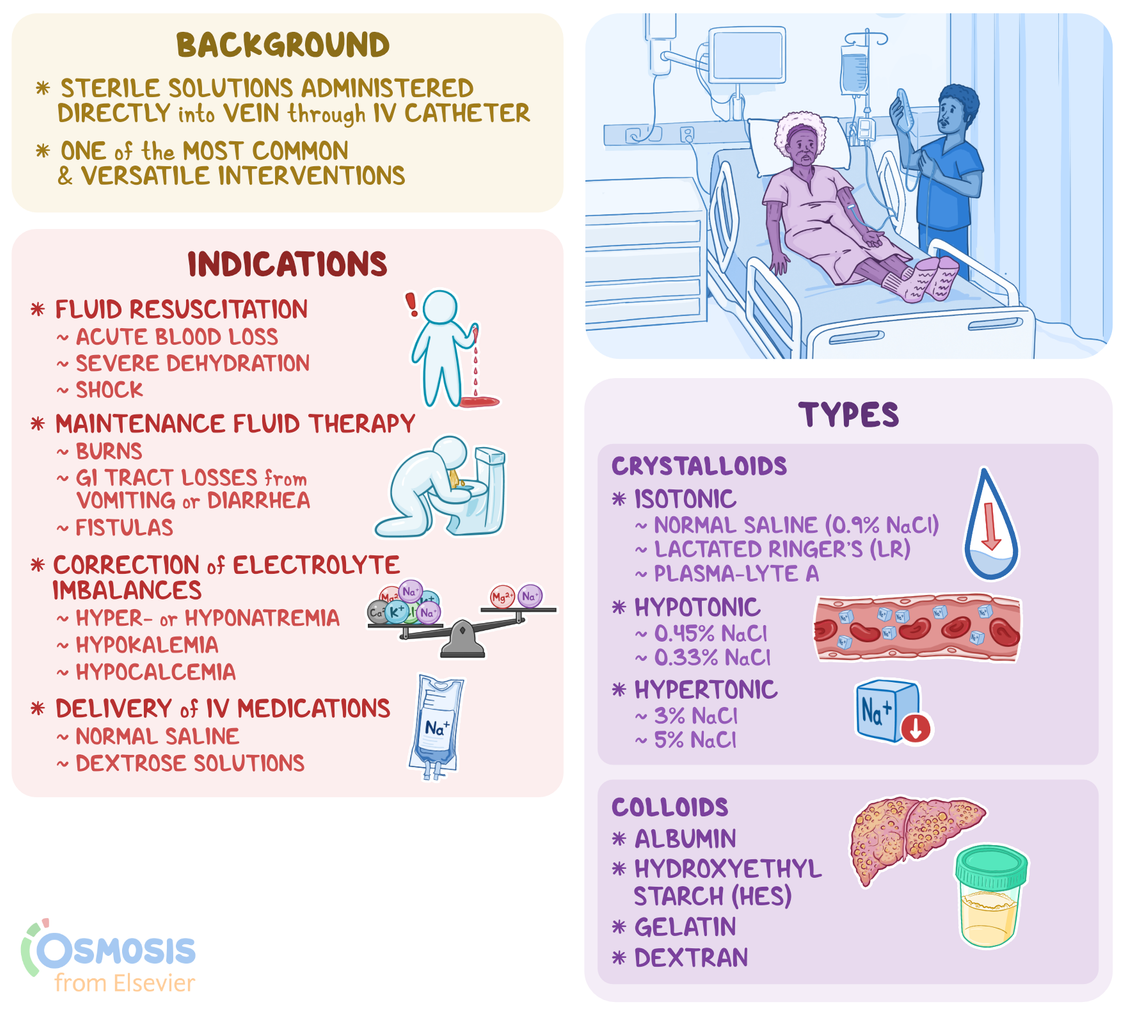

Crystalloids represent the most common and cost-effective category of IV fluids. These solutions are composed of small molecules that can freely pass through semipermeable membranes, including capillary walls. Their primary function is to expand the extracellular fluid volume, which includes both the interstitial and intravascular spaces. From a financial standpoint, crystalloids are the baseline against which other fluid types are often compared due to their affordability and widespread availability.

Composition and Cost-Effectiveness of Crystalloids

Crystalloids are typically aqueous solutions containing electrolytes such as sodium, potassium, chloride, and sometimes bicarbonate or lactate, as well as non-electrolyte solutes like dextrose. The most prevalent examples include:

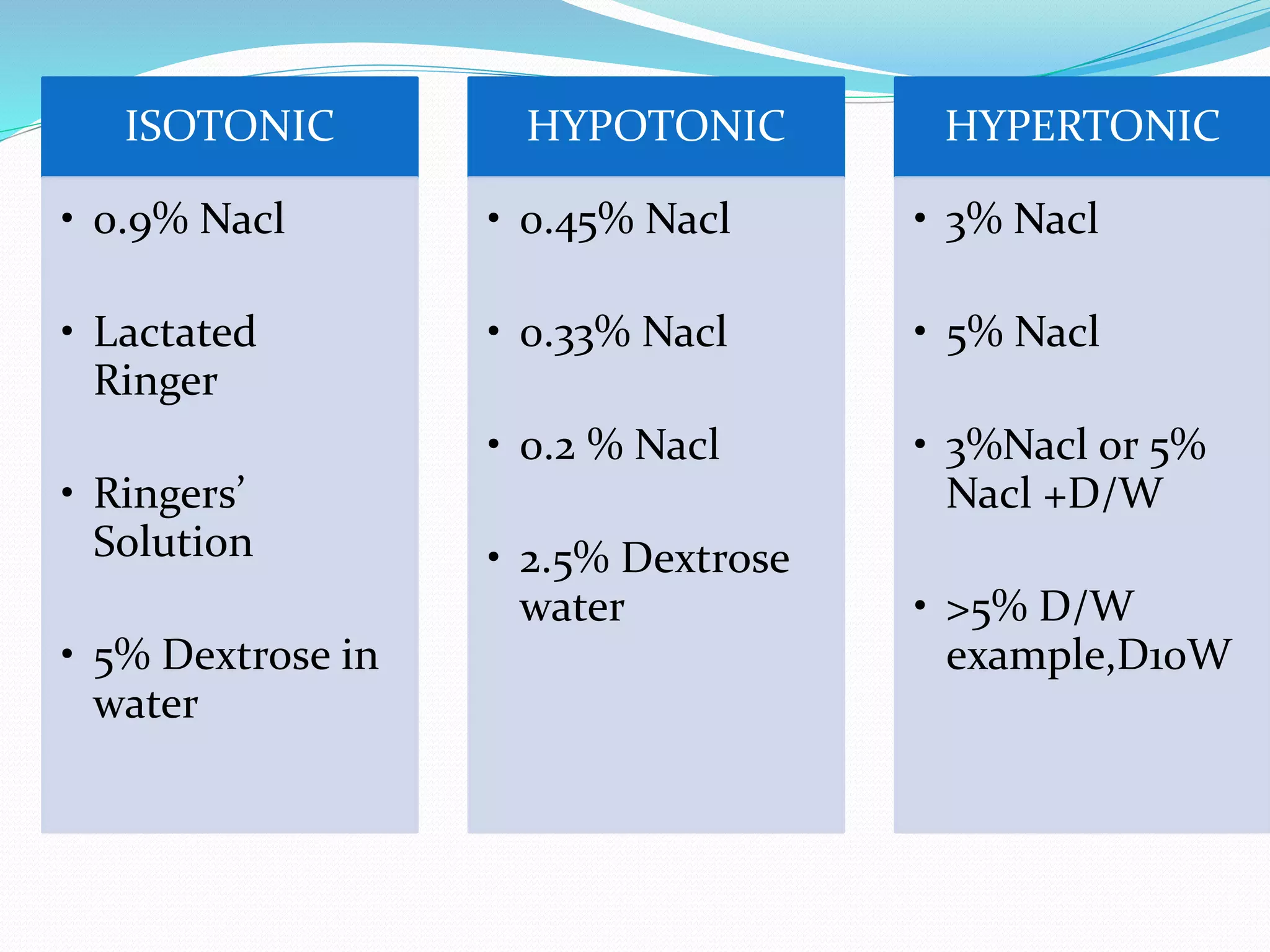

- Isotonic Solutions: These have an electrolyte concentration similar to that of plasma.

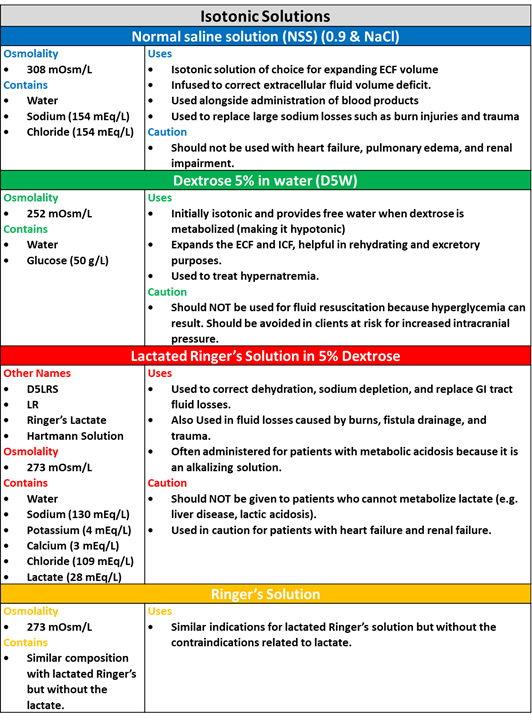

- 0.9% Sodium Chloride (Normal Saline): This is arguably the most ubiquitous IV fluid. Its low cost of manufacturing, extensive shelf-life, and versatility make it a cornerstone of fluid resuscitation and maintenance. From a procurement perspective, bulk purchasing of normal saline offers significant economies of scale. The financial advantage lies in its minimal processing requirements and the readily available raw materials.

- Lactated Ringer’s Solution: Slightly more complex than normal saline due to the addition of lactate, potassium, and calcium, Lactated Ringer’s is often favored for its ability to buffer metabolic acidosis. While its cost may be marginally higher than normal saline due to the additional components and slightly more complex manufacturing process, it remains a highly cost-effective option for a broader range of clinical scenarios. The financial benefit here lies in potentially reducing the need for separate bicarbonate administration in certain patients.

- Hypotonic Solutions: These solutions have a lower solute concentration than plasma, causing water to move from the intravascular space into the interstitial and intracellular spaces. Examples include 0.45% sodium chloride and 5% dextrose in water (D5W). While less commonly used for rapid volume expansion, they are crucial for managing certain electrolyte imbalances and providing free water. Their financial impact is generally lower than isotonic crystalloids due to lower electrolyte content, but careful monitoring is required to prevent fluid shifts, which could lead to secondary complications and increased healthcare costs.

- Hypertonic Solutions: These solutions have a higher solute concentration than plasma, drawing water from the interstitial and intracellular spaces into the intravascular space. Examples include 3% sodium chloride and 10% dextrose. Their use is typically limited and their cost is generally higher than isotonic solutions due to the concentration of solutes. From a financial planning perspective, their use needs to be carefully justified due to their higher unit cost and the need for more intensive patient monitoring to avoid complications, which can incur additional financial burdens.

The financial appeal of crystalloids stems from their relatively simple manufacturing processes, large production volumes, and long shelf lives. This translates into lower per-unit acquisition costs, making them the primary choice for routine fluid maintenance, moderate volume resuscitation, and as vehicles for drug administration. For healthcare institutions, optimizing the formulary for crystalloids, negotiating favorable contracts with manufacturers, and implementing efficient inventory management systems (e.g., just-in-time delivery for high-volume items) are critical financial strategies.

Colloids: The Volume Expanders with Higher Financial Implications

Colloids are IV solutions that contain larger molecules, such as starches, proteins, or synthetic polymers, which are too large to pass freely through capillary membranes. This property allows them to remain in the intravascular space for longer periods, effectively increasing plasma volume. While clinically beneficial in specific situations, their higher cost compared to crystalloids necessitates careful financial consideration.

The Economic Considerations of Colloid Solutions

Colloids are primarily used for more aggressive fluid resuscitation in conditions of significant intravascular volume depletion, such as severe hemorrhage or sepsis, where rapid and sustained plasma volume expansion is critical. The main categories of colloids and their financial implications include:

- Albumin: Derived from human plasma, albumin is a natural colloid that plays a vital role in maintaining oncotic pressure. Its clinical efficacy is well-established for conditions like hypovolemic shock, severe burns, and hepatic cirrhosis. However, the cost of albumin is substantially higher than that of crystalloids. This is due to the complex and resource-intensive process of plasma collection, screening, purification, and sterile processing. From a financial management perspective, the use of albumin needs to be carefully justified based on patient acuity and response to less expensive alternatives. Bulk purchasing agreements and careful inventory control are crucial to manage its significant cost. Furthermore, potential risks associated with blood products, though minimized by stringent screening, can also indirectly impact financial exposure through increased monitoring or legal considerations.

- Synthetic Colloids: These include solutions like hydroxyethyl starches (HES) and dextrans. While historically used more widely, the use of certain synthetic colloids has been re-evaluated due to concerns about potential adverse effects, such as kidney injury and coagulopathy. This has led to market withdrawal of some products and stricter regulatory oversight. Financially, the cost of synthetic colloids can vary but is generally higher than crystalloids. The decision to use them often involves a risk-benefit analysis that includes not only the immediate cost of the fluid but also the potential for increased patient monitoring, treatment of side effects, and longer hospital stays, all of which contribute to the overall financial burden. For procurement departments, staying abreast of evolving clinical guidelines and regulatory changes impacting synthetic colloids is essential for making sound financial decisions.

The financial decision-making process for colloids involves a nuanced assessment. While they offer superior volume expansion in certain critical care scenarios, their elevated cost necessitates a clear clinical indication and a rigorous cost-benefit analysis. Healthcare systems must implement protocols that ensure colloids are used judiciously, avoiding unnecessary expenditure while ensuring that critically ill patients receive appropriate, albeit more expensive, treatment when indicated. Strategies such as formulary restrictions, physician education on appropriate indications, and careful negotiation with suppliers are key to managing the financial impact of these fluids.

Blood Products: The Most Costly and Clinically Specific IV Therapy

Blood products, while technically not “fluids” in the same sense as crystalloids and colloids, are administered intravenously and represent the most expensive and clinically specific category of IV therapy. Their use is reserved for specific conditions requiring the replacement of blood components or the administration of therapeutic proteins. From a financial perspective, blood products present a unique set of challenges and opportunities for cost management within healthcare organizations.

The Financial and Logistical Complexities of Blood Products

The administration of blood products is not merely an expense; it involves a complex supply chain, rigorous quality control, and specialized handling. The main types of blood products administered intravenously include:

- Packed Red Blood Cells (PRBCs): Used to treat anemia and improve oxygen-carrying capacity. The cost of PRBCs is high, reflecting the extensive process of blood donation, donor screening, blood typing, cross-matching, processing, and storage. Furthermore, the limited shelf-life of PRBCs requires sophisticated inventory management to minimize wastage. Financial strategies involve maximizing utilization, minimizing wastage through careful ordering and timely administration, and negotiating contracts with blood banks. The cost of potential transfusion reactions also needs to be factored into the overall financial risk assessment.

- Platelets: Administered to patients with low platelet counts or bleeding disorders. Like PRBCs, platelets are expensive due to the complexities of collection and processing, and they have a very short shelf-life, necessitating rapid turnover and efficient inventory management. Strategies to mitigate costs include precise ordering based on laboratory values and clinical need, and minimizing the need for platelet transfusions through appropriate medical management of underlying conditions.

- Fresh Frozen Plasma (FFP): Used to replace clotting factors in patients with bleeding due to coagulation deficiencies. FFP also carries a significant cost associated with its collection, processing, and storage. Its use is typically guided by specific coagulation test results and clinical bleeding. Financial management focuses on ensuring that FFP is administered only when indicated by laboratory parameters and clinical presentation to avoid unnecessary expenditure.

- Cryoprecipitate: A blood product derived from plasma rich in certain clotting factors. Its cost is also substantial, and its use is limited to specific bleeding disorders. Similar to FFP, financial prudence dictates careful selection of patients for cryoprecipitate transfusion.

Beyond the direct acquisition costs, the financial implications of blood products extend to the personnel required for administration, the specialized equipment for monitoring, and the potential for managing adverse reactions, which can significantly increase patient care costs. Healthcare organizations must implement robust transfusion policies and guidelines, invest in staff training, and utilize electronic health record systems to track blood product usage, ensuring that these valuable and expensive resources are used appropriately and efficiently, thereby optimizing the financial stewardship of the facility. The financial health of a healthcare organization can be significantly impacted by its blood product management strategies.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.