In the intricate landscape of personal finance, few tools rival the significance and versatility of Individual Retirement Accounts (IRAs). Far more than just another savings vehicle, IRAs represent a cornerstone of long-term financial planning, offering individuals powerful tax advantages designed to fuel their retirement dreams. For anyone serious about securing their financial future, understanding the nuances of IRAs is not merely beneficial; it’s essential. This comprehensive guide will demystify IRAs, exploring their core mechanisms, diverse types, strategic applications, and their crucial role within a broader financial strategy.

The Foundation of Retirement Savings: Understanding IRAs

At its heart, an IRA is a savings account designed to hold investments, offering tax benefits to individuals saving for retirement. Unlike a standard bank account, an IRA itself isn’t an investment; rather, it’s the container or wrapper that holds various investments like stocks, bonds, mutual funds, and exchange-traded funds (ETFs). The magic of an IRA lies in its tax-advantaged status, which allows your money to grow more efficiently over decades.

Defining an IRA: More Than Just a Bank Account

An Individual Retirement Account (IRA) is a retirement savings plan that allows you to save money for retirement in a tax-advantaged way. Established by the Employee Retirement Income Security Act of 1974 (ERISA), IRAs were designed to give individuals not covered by an employer-sponsored plan (like a 401(k)) a similar opportunity to save for retirement. Over time, their utility expanded, making them a vital component for almost any retirement planner, even those with workplace plans. The fundamental principle is to encourage long-term savings by offering incentives like tax deductions on contributions or tax-free withdrawals in retirement.

The Core Purpose: Tax-Advantaged Growth for Retirement

The primary objective of an IRA is to facilitate retirement savings through tax incentives. These incentives typically fall into two main categories:

- Tax-Deductible Contributions: For certain types of IRAs, the money you contribute can be deducted from your taxable income in the year it’s contributed, lowering your immediate tax bill.

- Tax-Deferred or Tax-Free Growth: Investments held within an IRA grow either tax-deferred (you don’t pay taxes until you withdraw in retirement) or tax-free (you never pay taxes on qualified withdrawals in retirement). This compounding effect, unburdened by annual taxation on gains, can dramatically accelerate wealth accumulation over decades.

The power of tax-advantaged growth cannot be overstated. By shielding investment gains from immediate taxation, your money has more opportunity to generate returns on previous returns, leading to substantially larger balances by the time you reach retirement age compared to a taxable investment account.

Key Players: Custodians and Your Investment Choices

When you open an IRA, you’ll do so through a financial institution known as a custodian or trustee. This can be a bank, brokerage firm, mutual fund company, or insurance company. The custodian is responsible for holding your assets, maintaining records, and ensuring compliance with IRS rules.

Once your IRA is established with a custodian, you gain the freedom to choose how your money is invested within that account. Unlike some employer-sponsored plans that might have a limited menu of options, most custodians offer a wide array of investment choices, including:

- Stocks: Individual company shares.

- Bonds: Debt instruments issued by governments or corporations.

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other securities.

- Exchange-Traded Funds (ETFs): Similar to mutual funds but trade like stocks on an exchange.

- Certificates of Deposit (CDs) and Money Market Accounts: Lower-risk, lower-return options often offered by banks.

- Real Estate Investment Trusts (REITs): Companies that own, operate, or finance income-generating real estate.

This flexibility allows you to tailor your IRA portfolio to your specific risk tolerance, financial goals, and timeline.

Deciphering the Main Types of IRAs

While the core concept of an IRA remains consistent, several distinct types cater to different financial situations, income levels, and tax preferences. The most common types are Traditional, Roth, SEP, and SIMPLE IRAs.

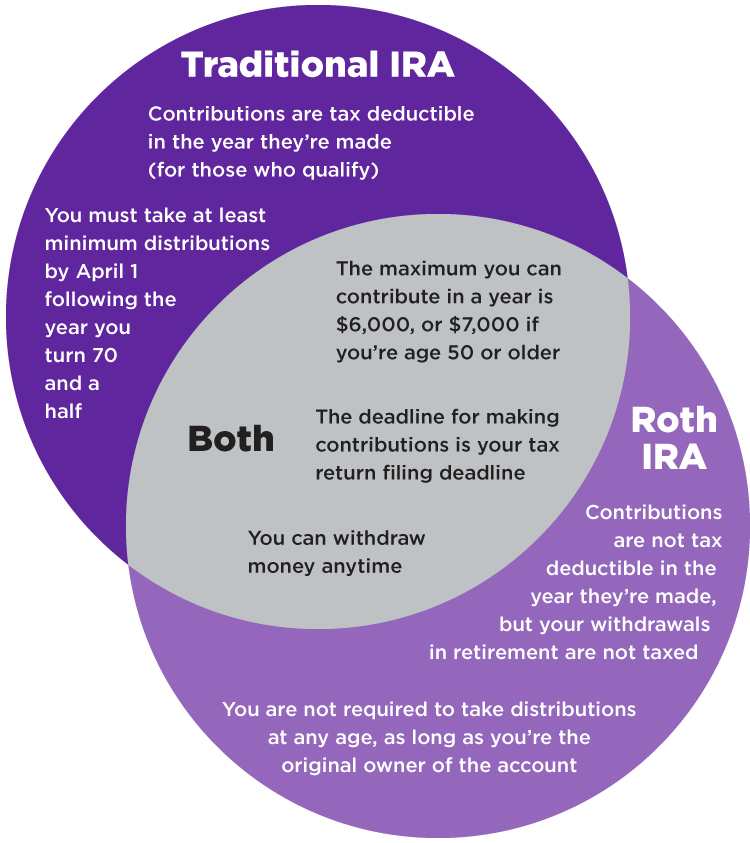

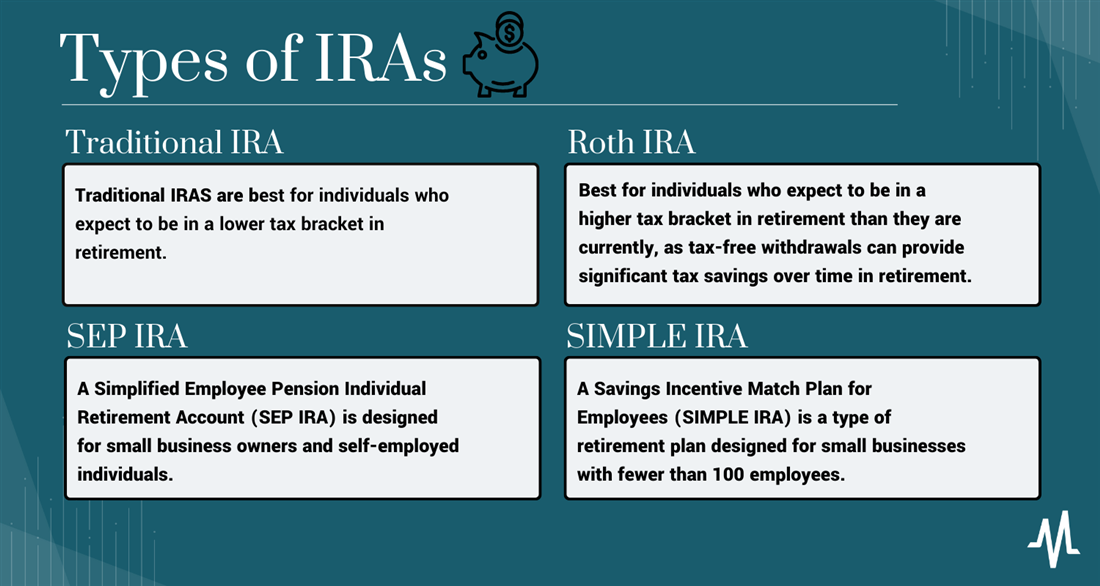

Traditional IRA: Pre-Tax Contributions and Deferred Taxes

The Traditional IRA is perhaps the most classic form, dating back to the inception of IRAs. Its defining characteristic is the potential for tax-deductible contributions in the present, leading to tax-deferred growth.

Who Benefits Most from a Traditional IRA?

Individuals who expect to be in a lower tax bracket in retirement than they are during their working years often find the Traditional IRA appealing. This is because they get a tax break now (when their tax bracket is higher) and pay taxes later (when their tax bracket is anticipated to be lower). It’s also a good choice for those who are nearing retirement and want to reduce their current taxable income.

Contribution Limits and Deductibility

For 2024, the contribution limit for Traditional IRAs is $7,000, with an additional “catch-up” contribution of $1,000 for individuals aged 50 and older, bringing the total to $8,000.

The deductibility of your Traditional IRA contributions depends on two factors:

- Whether you (or your spouse) are covered by a retirement plan at work.

- Your Modified Adjusted Gross Income (MAGI).

If neither you nor your spouse is covered by a workplace retirement plan, your contributions are generally 100% tax-deductible, regardless of your income. If you are covered by a workplace plan, the deductibility phases out at higher income levels. For single filers in 2024, the deduction begins to phase out with MAGI between $77,000 and $87,000, and for those married filing jointly, between $123,000 and $143,000.

Withdrawals from a Traditional IRA in retirement are taxed as ordinary income. Withdrawals before age 59½ generally incur a 10% early withdrawal penalty, in addition to being taxed, unless an exception applies.

Roth IRA: Post-Tax Contributions and Tax-Free Withdrawals

Introduced in 1997, the Roth IRA offers an alternative tax strategy: pay taxes on your contributions now, and enjoy tax-free withdrawals in retirement.

Who Benefits Most from a Roth IRA?

The Roth IRA is often ideal for younger individuals who anticipate being in a higher tax bracket during retirement than they are currently. By paying taxes on contributions now (when their tax bracket might be lower), they lock in tax-free growth and withdrawals later, potentially saving a significant amount in taxes over their lifetime. It’s also beneficial for those who want tax diversification in retirement, having both taxable and tax-free income sources.

Income Limitations and Contribution Rules

The contribution limits for Roth IRAs are the same as Traditional IRAs ($7,000 for 2024, or $8,000 if aged 50 or older). However, eligibility to contribute directly to a Roth IRA is subject to income limitations. For 2024, the ability to contribute directly begins to phase out for single filers with MAGI between $146,000 and $161,000, and for those married filing jointly, between $230,000 and $240,000. If your income exceeds these limits, you cannot make a direct contribution, though a “backdoor Roth” strategy may be an option.

Qualified withdrawals from a Roth IRA are completely tax-free and penalty-free, provided the account has been open for at least five years and you are age 59½ or older, disabled, or using the funds for a first-time home purchase (up to $10,000).

SEP IRA: Simplified Employee Pension for the Self-Employed

A Simplified Employee Pension (SEP) IRA is designed specifically for self-employed individuals and small business owners. It allows employers (including those who are self-employed) to contribute to their own retirement and their employees’ retirement accounts.

Eligibility and Contribution Advantages

SEP IRAs are much easier to set up and administer than a 401(k) plan. Eligibility is broad, making them attractive for freelancers, independent contractors, and small business owners with few or no employees.

The primary advantage of a SEP IRA is the high contribution limits. For 2024, you can contribute the lesser of 25% of your net self-employment earnings (for self-employed individuals) or $69,000. Contributions are tax-deductible for the employer (the business owner), and the funds grow tax-deferred. Employees, if applicable, cannot contribute to a SEP IRA; only the employer makes contributions. Withdrawals are taxed as ordinary income in retirement, similar to a Traditional IRA.

SIMPLE IRA: Savings Incentive Match Plan for Employees (Small Businesses)

A Savings Incentive Match Plan for Employees (SIMPLE) IRA is an employer-sponsored retirement plan designed for small businesses (typically those with 100 or fewer employees) that want to offer a retirement benefit without the complexity or cost of a 401(k).

Employer-Sponsored, Employee-Driven Benefits

Both employees and employers can contribute to a SIMPLE IRA. Employees can contribute up to $16,000 for 2024 ($19,500 if age 50 or older), and these contributions are tax-deductible. Employers are required to make contributions in one of two ways:

- Matching Contribution: Match employee contributions dollar-for-dollar up to 3% of their compensation.

- Non-Elective Contribution: Contribute 2% of each eligible employee’s compensation, regardless of whether the employee contributes.

Like Traditional and SEP IRAs, contributions grow tax-deferred, and withdrawals in retirement are taxed as ordinary income. Early withdrawals (before age 59½) are generally subject to a 10% penalty, which increases to 25% if withdrawn within the first two years of participation in the plan.

Strategic Considerations for IRA Contributions

Maximizing the benefits of an IRA involves more than just opening an account; it requires strategic planning around contribution limits, special situations like catch-up contributions, and understanding advanced maneuvers like rollovers and backdoor Roth IRAs.

Contribution Limits: Staying Within IRS Guidelines

The IRS sets annual limits on how much you can contribute to an IRA. For 2024, the standard limit for Traditional and Roth IRAs is $7,000. These limits apply across all your Traditional and Roth IRAs combined. For instance, if you have both a Traditional and a Roth IRA, your total contributions to both cannot exceed $7,000 (or $8,000 if 50 or older). Exceeding these limits can result in penalties. It’s crucial to be aware of these limits and plan your contributions accordingly, ideally maximizing them each year.

Catch-Up Contributions: A Boost for Older Savers

Recognizing that some individuals may start saving later in life or need to accelerate their retirement savings in their later working years, the IRS allows for “catch-up” contributions. If you are age 50 or older by the end of the tax year, you can contribute an additional $1,000 to your Traditional or Roth IRA, bringing the total annual limit to $8,000 for 2024. This provision provides a valuable opportunity to boost your retirement nest egg as you approach your golden years.

Rollovers: Consolidating Retirement Funds

A rollover involves moving funds from one retirement account to another. This is a common strategy when changing jobs, consolidating multiple old 401(k)s, or moving funds from an employer-sponsored plan into an IRA for greater investment flexibility or lower fees.

Direct vs. Indirect Rollovers

There are two main types of rollovers:

- Direct Rollover: The money is transferred directly from one trustee or custodian to another. This is the safest and most recommended method, as the funds never touch your hands, avoiding potential tax withholdings or penalties.

- Indirect Rollover: You receive a check for your retirement funds, and you have 60 days to deposit that money into another qualified retirement account. If you fail to do so within the 60-day window, the funds will be considered a taxable distribution and, if you’re under 59½, potentially subject to a 10% early withdrawal penalty. Furthermore, the IRS may withhold 20% of the distribution for taxes, which you’d have to make up from other funds to fully roll over the original amount.

Rollovers are generally tax-free events when executed correctly. They can simplify your financial life, provide more control over your investments, and potentially reduce fees.

Backdoor Roth IRA: Navigating Income Limits

For high-income earners whose Modified Adjusted Gross Income (MAGI) exceeds the limits for direct Roth IRA contributions, the “backdoor Roth IRA” strategy offers a legitimate way to contribute. This involves two steps:

- Contribute non-deductible funds to a Traditional IRA. Since your income is too high for deductible contributions, these contributions are after-tax.

- Immediately convert the Traditional IRA funds to a Roth IRA. Since the original contributions were non-deductible (after-tax), this conversion is typically tax-free. Any earnings that accrued between contribution and conversion would be taxable.

The backdoor Roth IRA is a powerful tool for those who want to benefit from tax-free growth and withdrawals but are otherwise locked out due to income restrictions. However, it can be complex, especially if you have existing pre-tax Traditional IRA balances (which trigger the “pro-rata rule”), so seeking advice from a financial advisor or tax professional is highly recommended.

Managing Your IRA: Investments, Distributions, and Penalties

Once your IRA is established and funded, ongoing management becomes crucial. This includes making informed investment choices, understanding rules around withdrawing funds in retirement, and knowing the consequences of early withdrawals.

Investment Choices Within an IRA

As mentioned, an IRA is a vessel for investments. The specific assets you hold within your IRA are entirely up to you (within the custodian’s offerings) and should align with your financial goals, risk tolerance, and time horizon.

Stocks, Bonds, Mutual Funds, ETFs, and More

Most IRA custodians offer a broad spectrum of investment options:

- Equities (Stocks): Offer potential for higher returns but come with higher volatility.

- Fixed Income (Bonds): Provide stability and income, often with lower risk than stocks.

- Diversified Funds (Mutual Funds, ETFs): Offer instant diversification across various asset classes, industries, or geographies, managed professionally or passively.

- Cash Equivalents: For short-term needs or as a temporary holding place.

The selection of investments should be part of a well-thought-out asset allocation strategy. For instance, younger investors with a longer time horizon might lean more heavily towards stocks, while those nearing retirement might shift towards a more conservative portfolio with a higher allocation to bonds. Regularly reviewing and rebalancing your IRA portfolio is vital to ensure it remains aligned with your objectives.

Understanding Required Minimum Distributions (RMDs)

To ensure the IRS eventually collects taxes on tax-deferred funds, the government mandates that you begin withdrawing money from certain retirement accounts once you reach a specific age. These are called Required Minimum Distributions (RMDs).

When They Start and How They’re Calculated

For Traditional, SEP, and SIMPLE IRAs, RMDs generally begin at age 73 (as of 2023, under the SECURE 2.0 Act). The amount of your RMD is calculated annually based on your account balance at the end of the previous year and your life expectancy factor from IRS tables. Failure to take an RMD can result in a significant penalty (historically 50%, now reduced to 25%, and potentially 10% if corrected promptly).

Roth IRAs, notably, do not have RMDs for the original owner. This means the money can continue to grow tax-free for the owner’s entire life and then be passed on to beneficiaries, offering significant estate planning advantages.

Early Withdrawal Penalties: When It Costs to Access Funds

IRAs are designed for retirement savings, and the tax advantages are contingent on leaving the money untouched until retirement age. Withdrawing funds from a Traditional, SEP, or SIMPLE IRA before age 59½ generally incurs a 10% early withdrawal penalty, in addition to the withdrawal being taxed as ordinary income.

Exceptions to the 10% Penalty

There are several exceptions to the early withdrawal penalty, though the withdrawals might still be taxable. These include:

- Qualified higher education expenses.

- Up to $10,000 for a first-time home purchase.

- Unreimbursed medical expenses exceeding 7.5% of your Adjusted Gross Income (AGI).

- Payments due to disability.

- Substantially equal periodic payments (SEPPs).

- For individuals called to active duty military service.

- Payments to beneficiaries after the account owner’s death.

Understanding these rules is critical, as dipping into your IRA early can significantly diminish your retirement savings and trigger unexpected tax burdens.

IRAs in Your Broader Financial Plan

IRAs are powerful tools, but they are just one component of a holistic financial strategy. Integrating them effectively with other savings vehicles and considering their role in estate planning can amplify their benefits.

Complementing Employer-Sponsored Plans (401(k)s)

For many individuals, an employer-sponsored retirement plan like a 401(k), 403(b), or TSP will be their primary retirement savings vehicle, especially if it offers an employer match (which should always be maximized). However, IRAs serve as excellent complements. If you’ve maxed out your 401(k) contributions and still want to save more, an IRA provides an additional avenue. The choice between a Traditional IRA and a Roth IRA can also help you diversify your tax strategy, ensuring you have both taxable and tax-free income streams in retirement.

Estate Planning and Beneficiary Designations

IRAs are valuable assets that can be passed on to beneficiaries. Properly designating beneficiaries for your IRA is a critical aspect of estate planning. Unlike assets passed through a will (which typically go through probate), IRA assets transfer directly to the named beneficiaries, simplifying the process and often avoiding probate court.

Beneficiaries have specific rules regarding how they can inherit and withdraw from an IRA, often allowing them to “stretch” the distributions over their lifetime, preserving the tax-advantaged growth. However, the SECURE Act and SECURE 2.0 Act introduced significant changes to beneficiary rules, particularly for non-spouse beneficiaries, often requiring them to distribute the entire account within 10 years of the original owner’s death. Consulting with an estate planning attorney is advisable to ensure your IRA beneficiary designations align with your overall estate plan and current tax laws.

Seeking Professional Guidance: Financial Advisors and Tax Professionals

The world of IRAs, with its various types, contribution limits, income phase-outs, rollover rules, RMDs, and tax implications, can be complex. While this guide provides a comprehensive overview, individual circumstances can vary greatly.

Engaging with a qualified financial advisor can help you determine which type of IRA is best suited for your goals, optimize your investment strategy within the IRA, and integrate it seamlessly into your overall financial plan. Similarly, a tax professional can provide invaluable assistance with understanding deductibility, navigating income limits, executing complex strategies like backdoor Roth IRAs, and ensuring compliance with all IRS regulations. Their expertise can help you maximize the benefits of your IRA while avoiding costly mistakes.

In conclusion, Individual Retirement Accounts are indispensable tools for building a secure financial future. By understanding their mechanics, leveraging their tax advantages, and integrating them strategically into your broader financial landscape, you can harness their power to achieve a comfortable and worry-free retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.