In the vast landscape of financial knowledge, certain fundamental mathematical concepts serve as the bedrock upon which complex strategies and sound decisions are built. Among these, geometric sequences stand out as a particularly powerful, yet often underappreciated, framework. Far from being an abstract academic exercise, understanding geometric sequences is absolutely crucial for anyone looking to master personal finance, optimize investments, or navigate the intricate world of business finance.

At its heart, a geometric sequence is a series of numbers where each term after the first is found by multiplying the previous one by a fixed, non-zero number called the common ratio. While this definition might sound purely mathematical, its real-world implications, especially in the realm of money, are profound. From the exponential growth of compound interest to the calculating depreciation of assets, geometric sequences are silently at work, shaping our financial realities. This article will demystify this critical concept, illustrating how it underpins some of the most vital financial principles and empowering you to harness its power for your own financial success.

The Core Concept: Understanding Geometric Sequences

To truly appreciate the financial implications of geometric sequences, we must first grasp their foundational mathematical structure. This isn’t about rote memorization of formulas, but rather an intuitive understanding of the pattern that defines them and sets them apart.

Defining the Pattern: Common Ratio

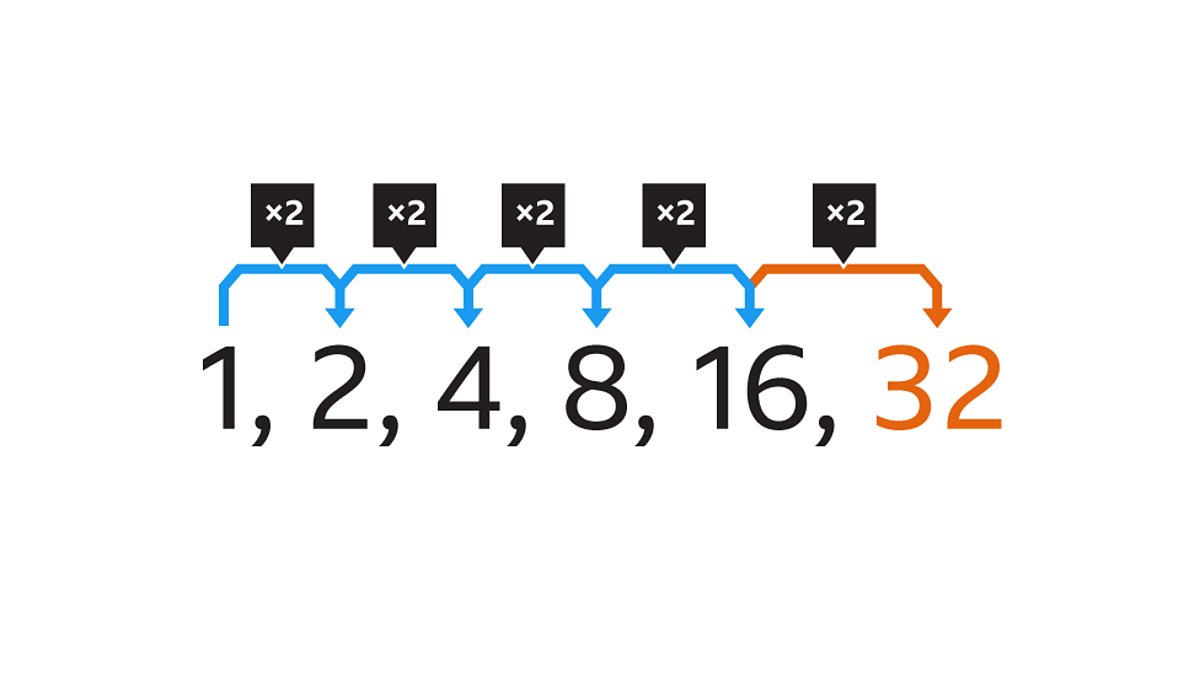

A geometric sequence is a progression of numbers where the ratio of any term to its preceding term is constant. This constant factor is known as the “common ratio” (often denoted as ‘r’). Consider a sequence like 2, 4, 8, 16, 32… Here, each number is twice the previous one. The common ratio is 2. Another example could be 100, 50, 25, 12.5… In this case, each term is half of the previous one, so the common ratio is 0.5 (or 1/2).

The key takeaway is this multiplicative relationship. Unlike arithmetic sequences, where a constant amount is added or subtracted, geometric sequences involve a constant proportion by which terms increase or decrease. This seemingly small distinction is precisely what gives geometric sequences their exponential power, making them incredibly relevant to financial growth and decay.

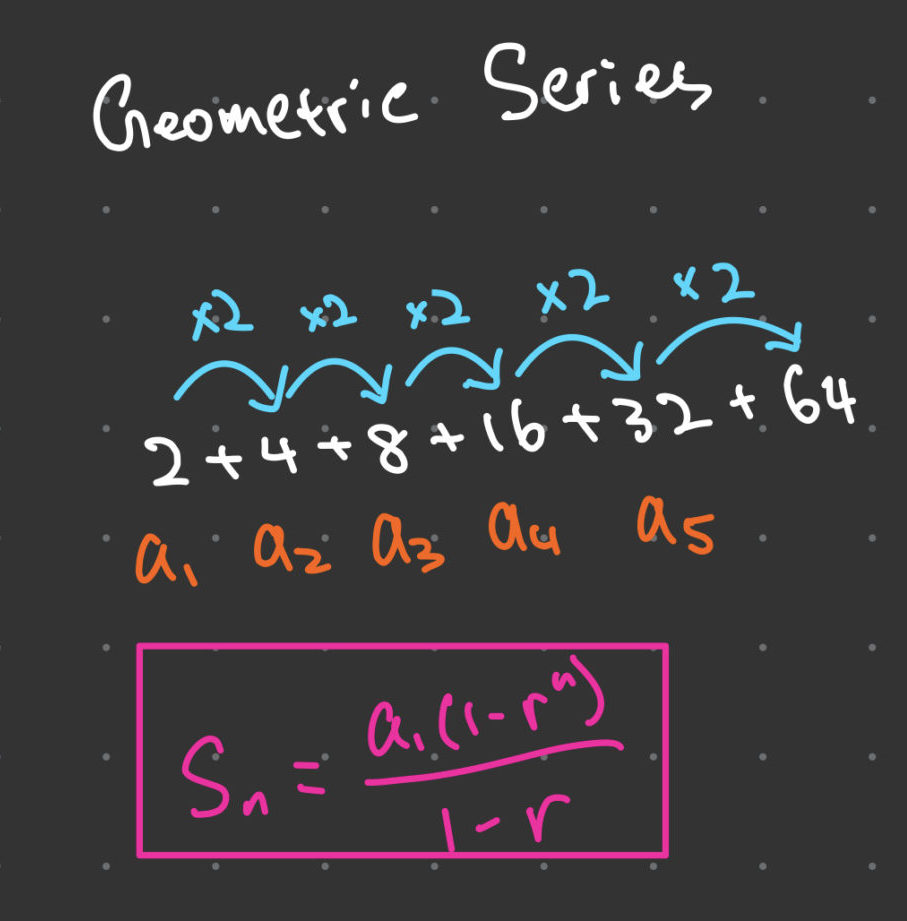

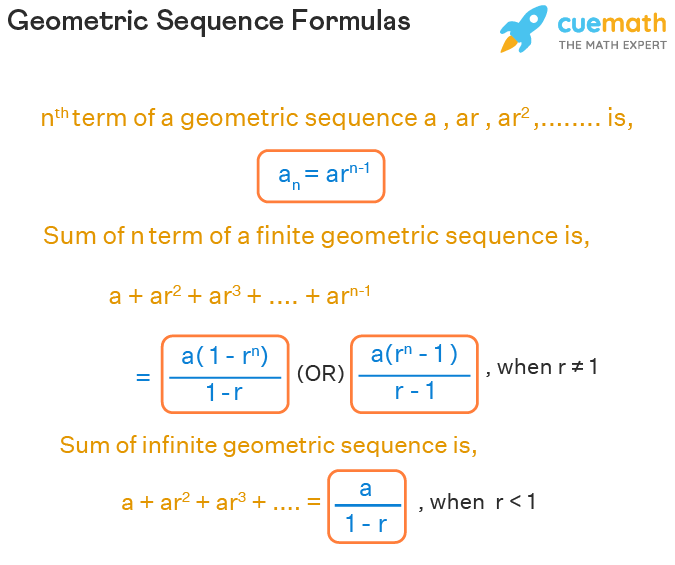

The Formula Behind Financial Growth

Mathematically, a geometric sequence can be represented by the formula:

$an = a1 cdot r^{(n-1)}$

Where:

- $a_n$ is the nth term (e.g., the value of your investment after ‘n’ periods).

- $a_1$ is the first term (e.g., your initial principal investment).

- $r$ is the common ratio (e.g., 1 + interest rate, or 1 – depreciation rate).

- $n$ is the number of terms or periods.

This formula directly translates into financial calculations. For instance, if you invest $1,000 ($a1$) at a 5% annual interest rate ($r = 1.05$), after 1 year ($n=2$, since $a1$ is year 0), your investment will be $1000 cdot (1.05)^{(2-1)} = $1050$. After 5 years ($n=6$), it would be $1000 cdot (1.05)^{(6-1)} = $1000 cdot (1.05)^5 approx $1276.28$. This illustrates the compounding effect, where not just the principal, but also the accumulated interest, begins to earn interest.

Contrasting with Arithmetic Sequences: The Power of Multiplication

To truly appreciate the significance of geometric sequences in finance, it’s helpful to briefly contrast them with their linear counterparts: arithmetic sequences. An arithmetic sequence involves adding or subtracting a constant difference to each term. For example, 100, 110, 120, 130… (adding 10 each time).

In financial terms:

- Arithmetic Growth: Simple interest, where interest is only earned on the initial principal. If you earn $100 in simple interest each year, your balance grows linearly.

- Geometric Growth: Compound interest, where interest is earned on the principal and on the accumulated interest. If your balance grows by 10% each year, the amount of interest earned increases over time, leading to exponential growth.

The difference in outcomes between these two types of growth, especially over long periods, is staggering. Understanding this distinction is fundamental to grasping why geometric sequences are the backbone of wealth creation.

The Power of Compounding: Geometric Sequences in Personal Finance

The most celebrated application of geometric sequences in personal finance is undoubtedly compound interest. However, their influence extends to various other critical areas, shaping both our opportunities for wealth accumulation and the challenges of debt.

Compound Interest: The Investor’s Best Friend

Compound interest is often hailed as the “eighth wonder of the world,” and for good reason. It’s a direct manifestation of a geometric sequence. When you earn interest on your initial investment (principal) and then earn interest on that accumulated interest, your money grows exponentially.

Let’s say you invest $5,000 at an annual interest rate of 7%.

- Year 1: $5,000 * (1 + 0.07) = $5,350

- Year 2: $5,350 * (1 + 0.07) = $5,724.50

- Year 3: $5,724.50 * (1 + 0.07) = $6,125.21

Each year, the base upon which interest is calculated increases, creating a geometric progression. Over decades, this seemingly small annual percentage can transform modest savings into substantial wealth. This is the cornerstone of long-term investing, retirement planning, and building intergenerational wealth. The earlier you start investing, the more periods your money has to compound, and the more pronounced the geometric growth becomes.

Debt: The Other Side of the Geometric Coin

While compounding can be an investor’s best friend, it can be a borrower’s worst enemy. Credit card debt, high-interest loans, and even mortgages often involve interest calculations that follow a geometric sequence. If you only make minimum payments on a credit card with a high annual percentage rate (APR), the unpaid interest gets added to your principal, and then that new, larger principal accrues more interest. This creates a vicious cycle of geometric growth, making it incredibly difficult to pay off debt.

For example, a $1,000 credit card balance at 20% APR will quickly balloon if not paid down aggressively. The longer the balance remains, the more the interest compounds, and the harder it is to escape. Understanding the geometric nature of debt is crucial for prioritizing repayment strategies and avoiding financial pitfalls. It underscores the importance of minimizing high-interest debt and paying off balances promptly.

Saving for Retirement: A Geometric Progression

Retirement planning is perhaps the most compelling real-world application of geometric sequences for individuals. Contributions made early in one’s career have decades to compound, leading to significantly higher returns than later contributions. A person who invests $200 per month from age 25 to 35 ($24,000 total) might end up with more money at retirement than someone who invests $200 per month from age 35 to 65 ($72,000 total), simply because the early investments benefited from more periods of geometric growth.

This principle emphasizes the power of “time in the market” over “timing the market.” By consistently investing, even modest amounts, and allowing your capital to grow geometrically over extended periods, you can achieve substantial financial security for your golden years. It’s a testament to the fact that patient, disciplined saving and investing is a geometric sequence waiting to unfold.

Strategic Applications in Investing and Business Finance

Beyond personal savings and debt management, geometric sequences play an integral role in more sophisticated financial analyses within investing and business contexts. They are essential tools for valuation, asset management, and strategic planning.

Valuing Investments: Discounted Cash Flows and Geometric Series

When professional investors evaluate companies or projects, they often use models like Discounted Cash Flow (DCF). DCF involves projecting future cash flows and then “discounting” them back to their present value. This discounting process essentially reverses a geometric sequence. Future cash flows are worth less today because of the opportunity cost of money (i.e., you could have invested that money elsewhere and earned a return).

A geometric series, which is the sum of terms in a geometric sequence, is used to calculate the present value of a stream of future cash flows, particularly when those cash flows are expected to grow at a constant rate (e.g., dividends that grow geometrically). Understanding this allows investors to determine a fair price for an asset today based on its future earning potential, adjusted for the time value of money. This is a critical component of fundamental analysis and investment decision-making.

Depreciation and Asset Management

Businesses often own assets (like machinery, vehicles, or buildings) that lose value over time. This loss of value is called depreciation. While some depreciation methods are linear (arithmetic), others, like the declining balance method, follow a geometric sequence.

In the declining balance method, a fixed percentage of the asset’s current book value is depreciated each year. For example, if a machine worth $10,000 depreciates by 20% annually:

- Year 1: Depreciation = $10,000 * 0.20 = $2,000. Book value = $8,000.

- Year 2: Depreciation = $8,000 * 0.20 = $1,600. Book value = $6,400.

- Year 3: Depreciation = $6,400 * 0.20 = $1,280. Book value = $5,120.

The book value of the asset forms a geometric sequence where the common ratio is (1 – depreciation rate). This method is important for accurate financial reporting, tax planning, and making informed decisions about when to replace or upgrade assets.

Business Growth Models and Projections

Businesses frequently use geometric sequences to model and project various aspects of their operations. Sales forecasts, market share growth, and even viral marketing campaigns can exhibit geometric growth patterns. If a business aims to grow its revenue by 15% each year, this is a geometric progression. Understanding this allows management to set realistic targets, allocate resources effectively, and assess the sustainability of growth trajectories.

For example, startups often experience geometric user acquisition or revenue growth in their early stages. Projecting this growth requires an understanding of common ratios and how they influence future scale. However, it’s also crucial to recognize that pure geometric growth often isn’t sustainable indefinitely, and models need to adjust for market saturation or competitive forces.

Leveraging Geometric Sequences for Financial Success

Armed with an understanding of geometric sequences, you are better equipped to make smarter financial decisions, plan more effectively, and navigate the complexities of the monetary world.

Financial Planning and Goal Setting

Whether you’re saving for a down payment, a child’s education, or retirement, geometric sequences provide the framework for setting realistic and achievable financial goals. By knowing your target amount ($an$), your initial contribution ($a1$), and your expected rate of return (embedded in $r$), you can calculate how long it will take to reach your goal ($n$) or what annual contribution you need to make. This empowers you to create actionable financial plans rather than relying on guesswork. Financial planning software and calculators heavily rely on these underlying geometric principles.

Making Informed Investment Decisions

Understanding geometric growth makes you a more discerning investor. You’ll appreciate why long-term investing in assets that compound consistently (like dividend stocks or growth funds) can lead to substantial wealth. You’ll also be wary of investment schemes that promise “arithmetic” returns on a fixed base, as true, sustainable wealth is built on compounding. Furthermore, knowing how geometric series are used in valuation models helps you interpret investment research and make more informed choices about buying or selling assets.

Mitigating Financial Risks

On the flip side, recognizing the geometric nature of high-interest debt is a powerful motivator for paying it down aggressively. It highlights the true cost of carrying credit card balances and empowers you to prioritize debt repayment as a critical step toward financial freedom. By understanding how quickly debt can compound, you can put strategies in place to avoid falling into debt traps and maintain a healthier financial standing.

In conclusion, geometric sequences are far more than a mathematical curiosity; they are a cornerstone of financial literacy. They explain the extraordinary power of compound interest, the insidious nature of compounding debt, and the fundamental principles behind investment valuation and business growth. By internalizing this concept, you gain a powerful lens through which to view your finances, enabling you to make more intelligent decisions, build lasting wealth, and navigate the economic landscape with greater confidence and insight. Embrace the power of the common ratio, and you’ll unlock a deeper understanding of your financial journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.