In the world of personal finance and wealth management, the “feet” represent the foundation upon which your entire economic life is built. Just as a physical ailment can prevent you from walking, running, or maintaining balance, financial “foot disorders” are those foundational errors, bad habits, and systemic missteps that prevent you from moving toward financial independence.

When we ask, “What are 10 common foot disorders?” in a fiscal context, we are looking for the structural weaknesses in a budget, the inflammatory habits in an investment portfolio, and the infections of debt that can cripple a side hustle before it gains traction. To achieve long-term wealth, one must diagnose these issues early, apply the correct “treatment,” and ensure that their financial gait is steady enough to withstand market volatility.

1. Structural Disorders: Foundational Financial Missteps

The foundation of any financial plan is its structure. If the basics—budgeting, saving, and debt management—are misaligned, the entire “body” of your net worth will suffer from chronic pain. These structural disorders are often the most common and the most ignored until they cause a total collapse.

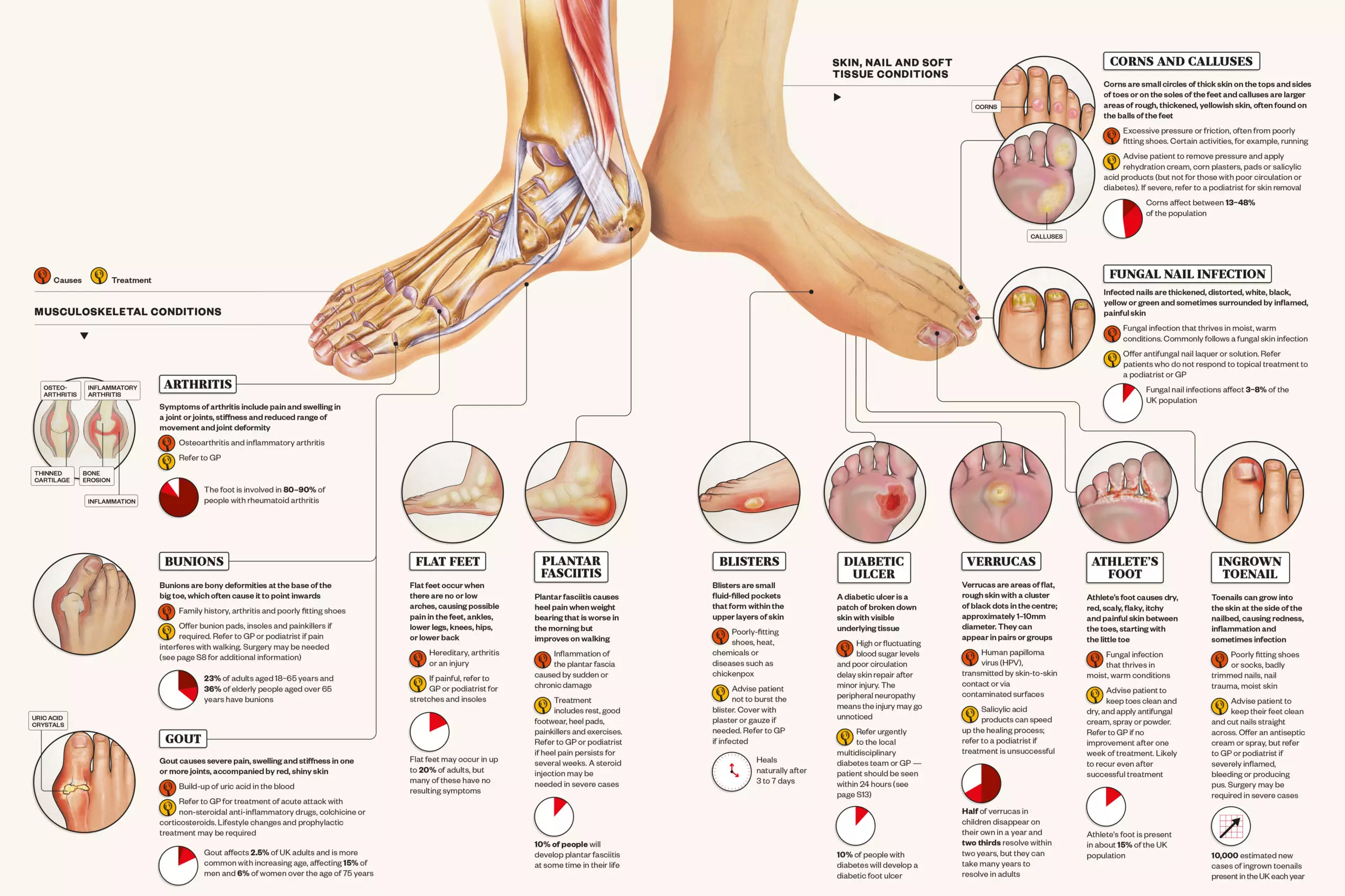

The Bunions of High-Interest Consumer Debt

In the medical world, a bunion is a bony bump that forms on the joint at the base of your big toe, caused by pressure and misalignment. In finance, high-interest consumer debt—specifically credit card debt—acts exactly like a bunion. It starts small, often due to a “misalignment” between income and lifestyle, but eventually becomes a painful protrusion that makes every step forward difficult.

High-interest debt (often exceeding 20% APR) creates a structural deformity in your cash flow. Instead of your money moving forward into investments, it is redirected to service interest. Treating this disorder requires “financial surgery”: aggressive debt repayment strategies like the debt snowball or debt avalanche methods to realign your capital.

Flat Feet: The Lack of a Liquid Emergency Fund

“Flat feet” occur when the arches of the feet collapse, leading to a lack of support for the rest of the body. Financially, this is equivalent to living without an emergency fund. Without a “cushion” of three to six months of expenses, you have no arch to absorb the shocks of life—be it a medical emergency, a car repair, or sudden job loss.

A person with flat financial feet is constantly at risk of a total breakdown. When a shock occurs, they are forced to rely on high-interest debt, which leads back to the “bunion” problem mentioned above. The remedy is a disciplined savings plan that prioritizes liquidity over returns until the arch is restored.

Plantar Fasciitis: The Chronic Pain of Overspending

Plantar fasciitis is an inflammation of the tissue that runs across the bottom of your foot. It causes stabbing pain with the first steps of the day. In the niche of personal finance, this is the chronic overspending on “lifestyle creep.” It is the pain that comes from a high-income earner who still lives paycheck to paycheck.

Overspending inflames your budget, making it impossible to pivot or take risks (like starting a side hustle or investing in a volatile but high-growth asset). Curing this requires “stretching” the budget—finding ways to expand the gap between what you earn and what you spend through rigorous tracking and intentional living.

2. Growth and Investment Disorders: Stunting Your Net Worth

Once the foundation is stabilized, the focus shifts to movement—specifically, growth through investing and income diversification. However, even with a solid structure, certain “disorders” can prevent your wealth from moving at the pace required to outrun inflation and reach retirement goals.

Hammer Toe: Rigidity in Investment Portfolios

A hammer toe is a deformity where the toe bends downward instead of pointing forward, becoming stiff and rigid. Financially, this represents a rigid, non-diversified investment portfolio. Perhaps you are “stuck” in a single stock because of emotional attachment, or perhaps you refuse to move out of low-yield bonds despite having a 30-year time horizon.

This rigidity prevents you from adapting to changing market conditions. If the economy shifts toward tech or green energy and your portfolio is stubbornly fixed in 20th-century industrials, your growth will be stunted. Professional wealth management involves “orthopedic” adjustments—rebalancing your portfolio annually to ensure your toes are pointing toward future growth, not downward toward stagnation.

Fungal Infections: The Hidden Cost of High Management Fees

Fungal infections are often invisible at first, hiding under the surface and slowly eating away at the health of the nail. In the investment world, these are the hidden management fees, high expense ratios, and “load” fees associated with certain mutual funds or predatory financial advisors.

A 1% or 2% fee might seem small, like a minor itch. However, over 30 years, a 2% fee can consume nearly half of your potential investment gains. This is a parasitic disorder that thrives on investor ignorance. The treatment is “antifungal” transparency: switching to low-cost index funds and ETFs that allow your principal to grow unimpeded.

Ingrown Nails: The Danger of Inward-Looking Financial Strategies

An ingrown nail occurs when the side of the nail grows into the flesh, causing pain and infection. In business and personal finance, this represents an “inward-looking” strategy where an individual focuses solely on saving pennies while ignoring the “flesh” of the broader economy.

While frugality is a virtue, focusing exclusively on cutting costs (the “latte factor”) while ignoring your earning potential is a disorder. It is painful and limits your mobility. To fix an ingrown financial nail, you must look outward—focusing on skill acquisition, networking, and increasing your “top-line” revenue through side hustles or career advancement.

3. Lifestyle and Side Hustle Disorders: Hindering Career Mobility

In the modern “Money” landscape, side hustles and career pivoting are the primary drivers of wealth. However, these activities are prone to specific ailments that can halt your momentum and leave you sidelined.

Blisters: The Friction of Unsustainable Side Hustles

Blisters are caused by friction—usually from shoes that don’t fit quite right. When you start a side hustle that doesn’t align with your skills or passions, you create “friction.” You might be making extra money, but the burnout (the blister) eventually makes it impossible to continue.

An unsustainable side hustle—like a high-stress delivery job on top of a 50-hour work week—will eventually burst. The goal is to find a “better fit”: a side hustle that leverages your existing expertise and offers a smoother “ride” toward your financial goals.

Calluses: Becoming Desensitized to Market Trends

Calluses are thickened areas of skin that form to protect against pressure. While protective, they also decrease sensitivity. Financially, we develop “calluses” when we become desensitized to market trends or technological shifts. We stop learning because we believe our current path is “tough enough.”

If you are a freelancer or business owner, being desensitized to the rise of AI or changes in digital marketing is a disorder. You lose the “feel” for the market. To remain agile, you must occasionally “exfoliate” your skill set—shedding old, hardened habits and learning new tools to stay sensitive to where the money is moving.

Athlete’s Foot: Contagious Financial Negativity

Athlete’s foot is a contagious fungal infection spread in communal areas. In the world of money and business, this is the “contagious” negativity of your social and professional circle. If you surround yourself with people who believe wealth is impossible, that the system is entirely rigged, or that “money is the root of all evil,” you will catch that infection.

This disorder stunts your ambition. It makes you stay in the “locker room” rather than getting out on the field. The cure is social hygiene—surrounding yourself with mentors, masterminds, and peers who have a growth mindset and healthy financial habits.

Sprains: Sudden Financial Shock and Lack of Insurance

A sprain is a sudden injury to a ligament. Financially, this is the shock of a lawsuit, a major disability, or a property loss that occurs when you are under-insured. Many people view insurance (life, disability, liability) as an unnecessary expense, but without it, a single “misstep” can result in a permanent limp.

A financial sprain can take years to heal if you have to pay out of pocket for a major liability. Proper “bracing”—in the form of comprehensive insurance coverage—ensures that even if you take a hard fall, your ligaments (your core assets) remain intact.

Conclusion: Walking Toward Financial Wellness

Just as physical foot health requires daily care, proper footwear, and occasional professional intervention, your financial “feet” require constant attention. By identifying these 10 common disorders—from the “bunions” of debt to the “fungus” of hidden fees—you can begin the process of rehabilitation.

The goal of identifying these disorders is not just to stop the pain, but to enable movement. When your financial foundation is healthy, you can walk toward a comfortable retirement, run toward a daring new business venture, and stand firm in the face of economic uncertainty. Don’t let a preventable disorder keep you from the wealth you are capable of building. Take the time to diagnose your financial gait today, apply the necessary treatments, and step confidently into a prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.