Deciding when to claim Social Security benefits is one of the most critical financial decisions an individual will make in their lifetime. It is a choice that dictates the monthly cash flow for the remainder of one’s life and can significantly impact a spouse’s financial security. While the Social Security Administration provides a window of eligibility starting at age 62 and ending at age 70, the “correct” age is rarely a one-size-fits-all answer. Instead, it is a complex calculation involving life expectancy, financial needs, tax implications, and employment status.

In the landscape of personal finance, Social Security often represents the only inflation-adjusted, guaranteed-for-life income stream available to retirees. Understanding how the timing of your claim affects your “Primary Insurance Amount” (PIA) is essential for anyone looking to build a robust retirement portfolio.

Understanding the Full Retirement Age (FRA) as Your Financial Benchmark

The Full Retirement Age (FRA) is the centerpiece of the Social Security system. It is the specific age at which a worker is entitled to 100% of their earned benefits, calculated based on their highest 35 years of indexed earnings. For decades, the FRA was 65, but legislative changes in 1983 set a gradual increase to account for longer life expectancies.

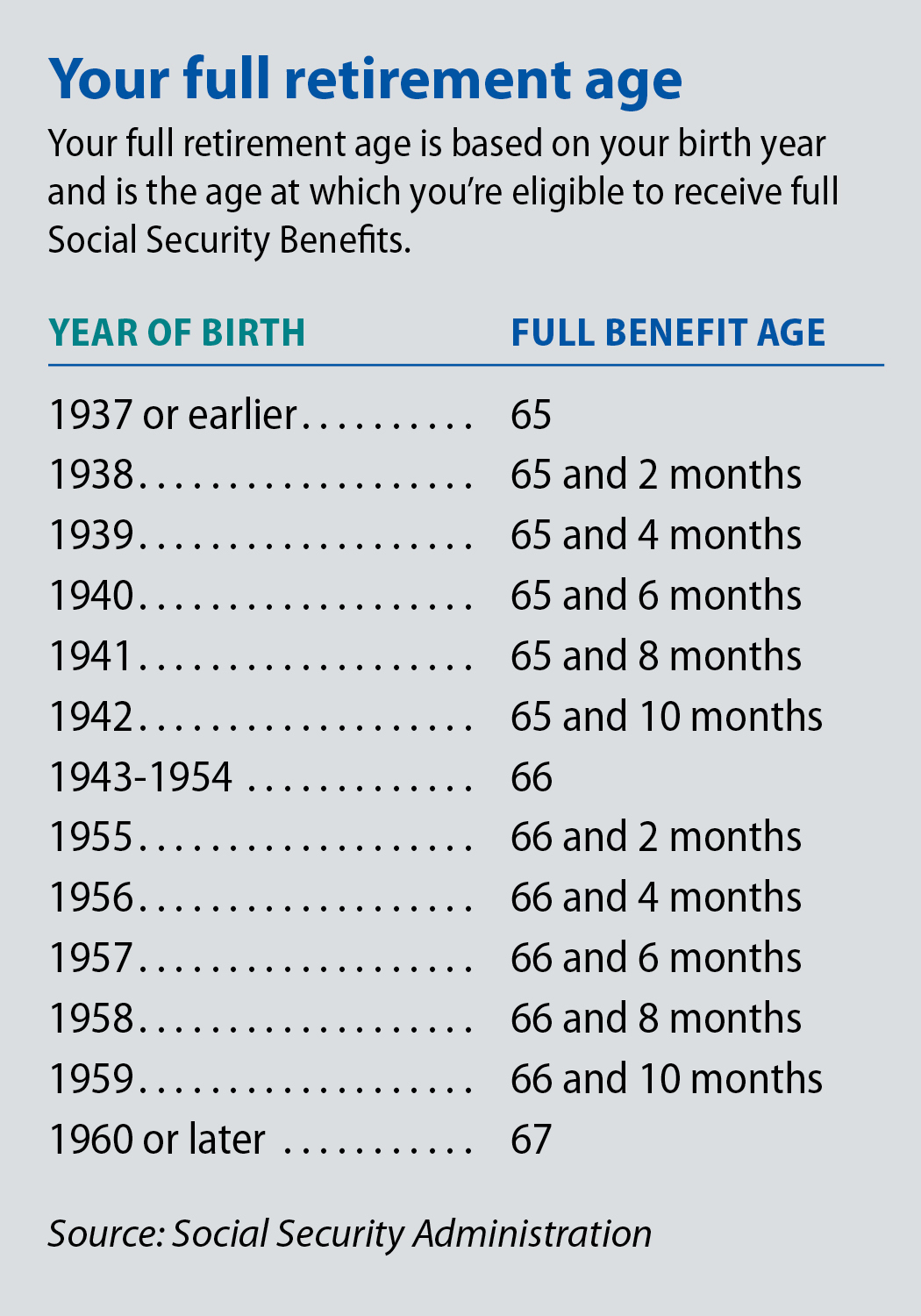

How Your Birth Year Determines Your FRA

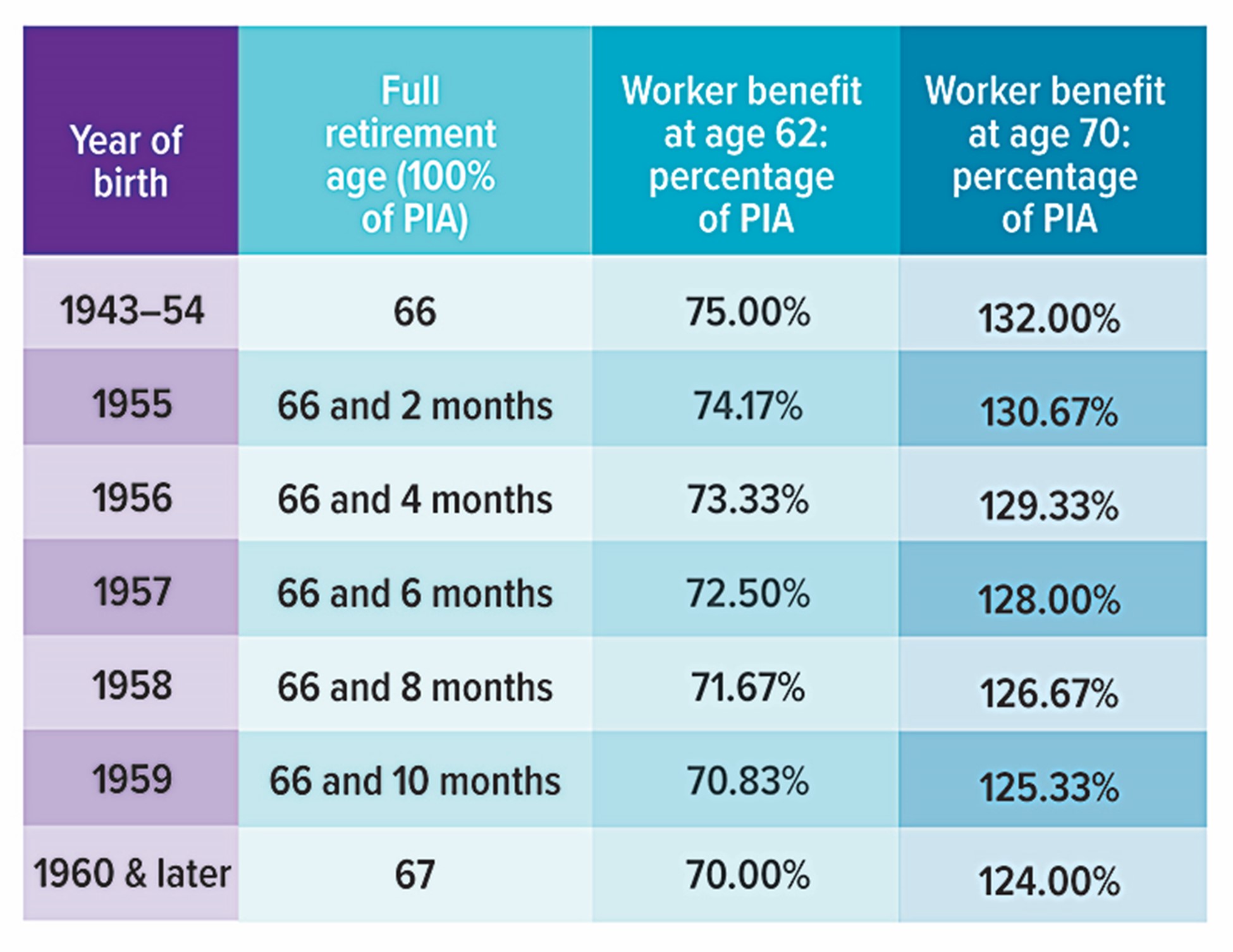

The Social Security Administration uses a sliding scale based on the year you were born. For those born between 1943 and 1954, the FRA is 66. For those born later, the age increases by two months for every year until it reaches age 67 for anyone born in 1960 or later. Understanding your specific FRA is vital because it serves as the neutral point; claiming before this age results in a permanent reduction, while claiming after results in a permanent increase.

Why the FRA is the Pivot Point for Benefit Calculations

The FRA is not just a milestone; it is the mathematical anchor for all Social Security calculations. If your FRA is 67 and you choose to claim at 62, your monthly benefit is reduced by 30%. Conversely, if you wait until 70, your benefit increases by 24%. This delta—a 54% difference in monthly income between age 62 and age 70—highlights why the FRA is the most important number in your retirement planning. It acts as the “par” against which all other ages are measured.

The Financial Implications of Claiming Early at Age 62

For many, the temptation to claim Social Security as soon as they become eligible at age 62 is strong. Whether due to health concerns, job loss, or a desire to enjoy retirement while still young and active, approximately one-quarter of Americans claim at the earliest possible opportunity. However, this immediate liquidity comes at a steep long-term cost.

The Immediate Cash Flow Advantage vs. Permanent Reduction

The primary benefit of claiming at 62 is “bird in the hand” logic. You start receiving checks immediately, which can help bridge the gap if you retire early or want to preserve your private investment accounts. However, this choice triggers a permanent reduction in your monthly benefit. This reduction is calculated monthly: for the first 36 months before FRA, the benefit is reduced by 5/9 of 1% per month. For any months beyond that, it is reduced by an additional 5/12 of 1% per month. Over a lifetime, if you live into your late 80s or 90s, the cumulative loss of income can be hundreds of thousands of dollars.

The Retirement Earnings Test for Early Claimants

A common mistake made by those claiming early is failing to account for the Social Security “Earnings Test.” If you claim benefits before your FRA and continue to work, the Social Security Administration will withhold $1 in benefits for every $2 you earn above a certain annual limit (which is $22,320 in 2024). While these withheld benefits are eventually “returned” to you through a recalculated monthly amount once you reach FRA, the immediate effect is a significant reduction in the very cash flow you sought by claiming early. This makes claiming at 62 a poor strategy for anyone intending to remain in the workforce.

Impact on Survivor and Dependent Benefits

Your decision does not just affect you; it affects your household. If you are the higher-earning spouse, claiming early permanently locks in a lower “survivor benefit” for your spouse. Should you pass away first, your spouse is entitled to the higher of their own benefit or 100% of yours. By claiming at 62, you are effectively capping the maximum amount your widow or widower can receive, potentially creating a financial hardship for them later in life when healthcare costs are highest.

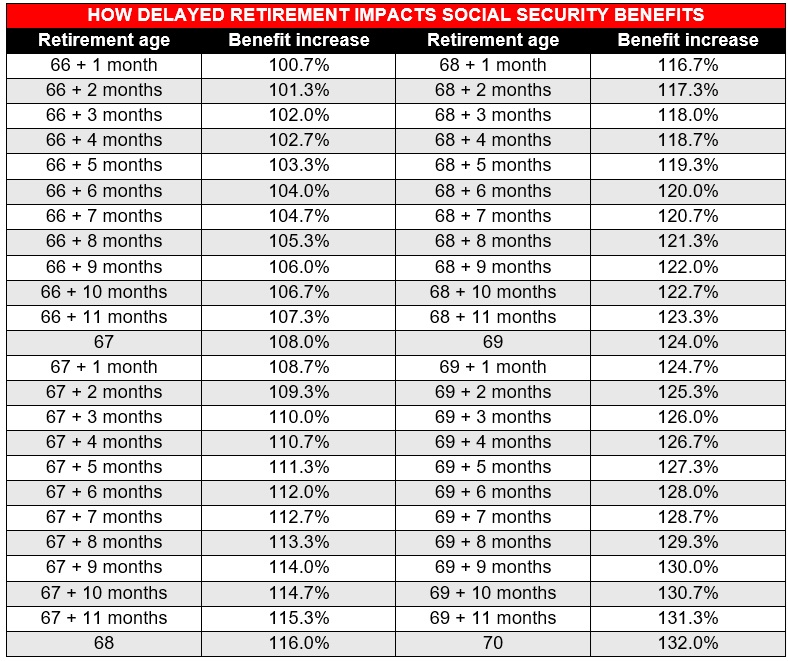

Maximizing the “Delayed Retirement Credits” Until Age 70

On the opposite end of the spectrum is the strategy of waiting until age 70. This is often viewed by financial planners as one of the best “investments” available in the market today, as the guaranteed increase in benefits far outpaces most conservative investment yields.

The Power of the 8% Annual Increase

For every year you delay claiming beyond your FRA (up until age 70), your benefit increases by 8% through “Delayed Retirement Credits.” This is a simple interest increase that is applied to your PIA. In an era where high-yield savings accounts or bonds might offer 4-5%, a guaranteed 8% return—adjusted for inflation—is an unmatched financial tool. There is no incentive to wait past age 70, as the credits stop accumulating at that point.

Longevity Risk and the “Break-Even” Analysis

The primary argument against waiting until 70 is the fear of passing away before recouping the “lost” years of payments. This leads to a “break-even” analysis—calculating the age at which the total cumulative benefits of waiting until 70 exceed the total cumulative benefits of claiming at 62 or 67. Generally, the break-even point is between age 78 and 82. Given that a 65-year-old man today has a high probability of living to 84, and a 65-year-old woman to 87, most retirees who are in average health will statistically benefit from delaying their claim.

Using Social Security as Longevity Insurance

In personal finance, we often view Social Security as an investment, but it is better categorized as insurance. Specifically, it is insurance against “longevity risk”—the risk of outliving your money. By waiting until 70 to secure the largest possible monthly check, you are creating a higher floor for your income. If you live to 95 or 100, the extra thousands of dollars per month provided by delaying until 70 become the most valuable part of your financial plan, protecting you when other assets might be depleted.

Strategic Factors for Choosing Your Optimal Claiming Age

While the math often favors waiting, life is not lived on a spreadsheet. Several qualitative and external financial factors must be weighed before signing the paperwork with the Social Security Administration.

Health Status and Life Expectancy

Your personal and family health history should heavily influence your decision. If you have chronic health issues or a family history of short lifespans, claiming at 62 or FRA may be the most rational choice. Conversely, if you are healthy and come from a family of centenarians, delaying is almost always the superior financial move.

Marital Status and Spousal Benefit Coordination

For married couples, the strategy becomes “the highest earner delays, the lower earner considers claiming earlier.” This strategy ensures that the largest possible benefit is preserved for the survivor. Additionally, if one spouse has a very low earnings history, they may be eligible for a “Spousal Benefit,” which can be up to 50% of the higher earner’s FRA benefit. Coordinating these two claims requires a holistic view of the couple’s joint life expectancy.

Tax Efficiency and Portfolio Sequencing

Social Security benefits are not always tax-free. Depending on your “combined income” (Adjusted Gross Income + Non-taxable Interest + half of your Social Security benefits), up to 85% of your benefits could be subject to federal income tax. Some retirees choose to delay Social Security and instead draw down their traditional IRAs or 401(k)s between ages 60 and 70. This strategy reduces the size of future Required Minimum Distributions (RMDs) and allows the Social Security benefit to grow untaxed until the claim is made, resulting in a more tax-efficient retirement overall.

Conclusion: Making an Informed Decision

Choosing the age to claim Social Security benefits is a balancing act between immediate needs and long-term security. While age 62 offers early freedom, it comes with a heavy “tax” in the form of reduced payments. Age 70 offers the maximum possible security but requires other assets to fund the early years of retirement.

Ultimately, the best age to claim is the one that aligns with your total financial picture: your health, your marital obligations, your tax bracket, and your other sources of income. By understanding the mechanics of the FRA, the penalties of early filing, and the rewards of delayed credits, you can transform Social Security from a confusing government program into a powerful engine for financial independence. Regardless of the choice, the goal remains the same: ensuring that your final chapters are defined by financial peace rather than fiscal uncertainty.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.