For decades, the age of 70½ was etched into the minds of American retirees as the definitive milestone for Required Minimum Distributions (RMDs). It was the point at which the Internal Revenue Service (IRS) finally demanded its share of the tax-deferred “seed money” individuals had been cultivating in their 401(k)s and Traditional IRAs. However, recent legislative overhauls—most notably the SECURE Act of 2019 and the SECURE 2.0 Act of 2022—have fundamentally shifted this financial goalpost.

Understanding the current RMD age is no longer a simple matter of remembering a single number; it requires an understanding of your birth year and the evolving federal statutes designed to address increasing life expectancies and the changing economic realities of modern retirement. In the current personal finance landscape, failing to track these changes can result in some of the steepest penalties in the tax code.

Understanding the SECURE 2.0 Act and the Shifting RMD Age

The primary driver behind the confusion regarding RMD ages is the SECURE 2.0 Act. This bipartisan legislation was designed to encourage more robust retirement savings while acknowledging that many Americans are working longer and living deeper into their senior years. By delaying the age at which distributions must begin, the government allows retirement assets more time to grow tax-deferred.

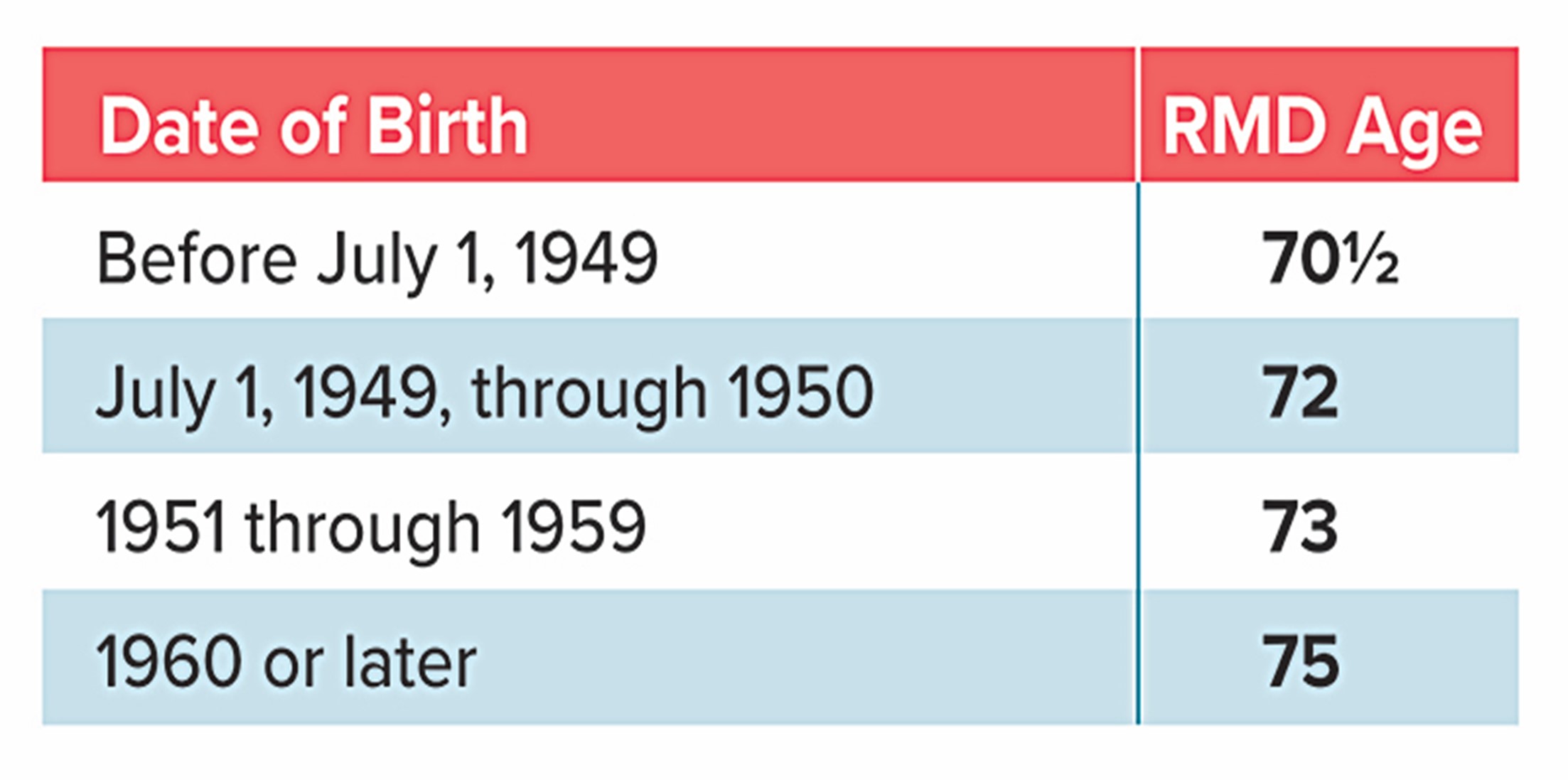

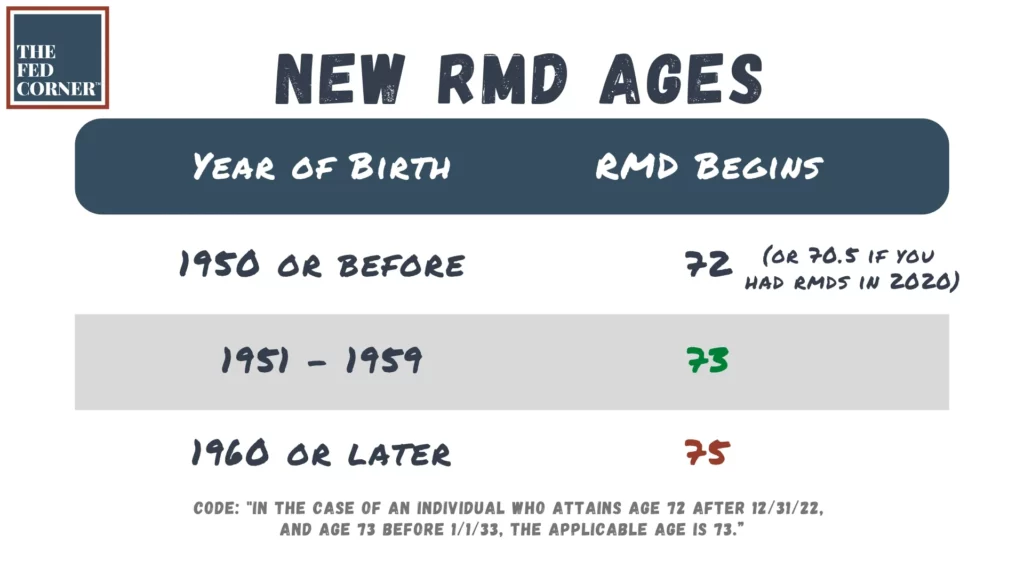

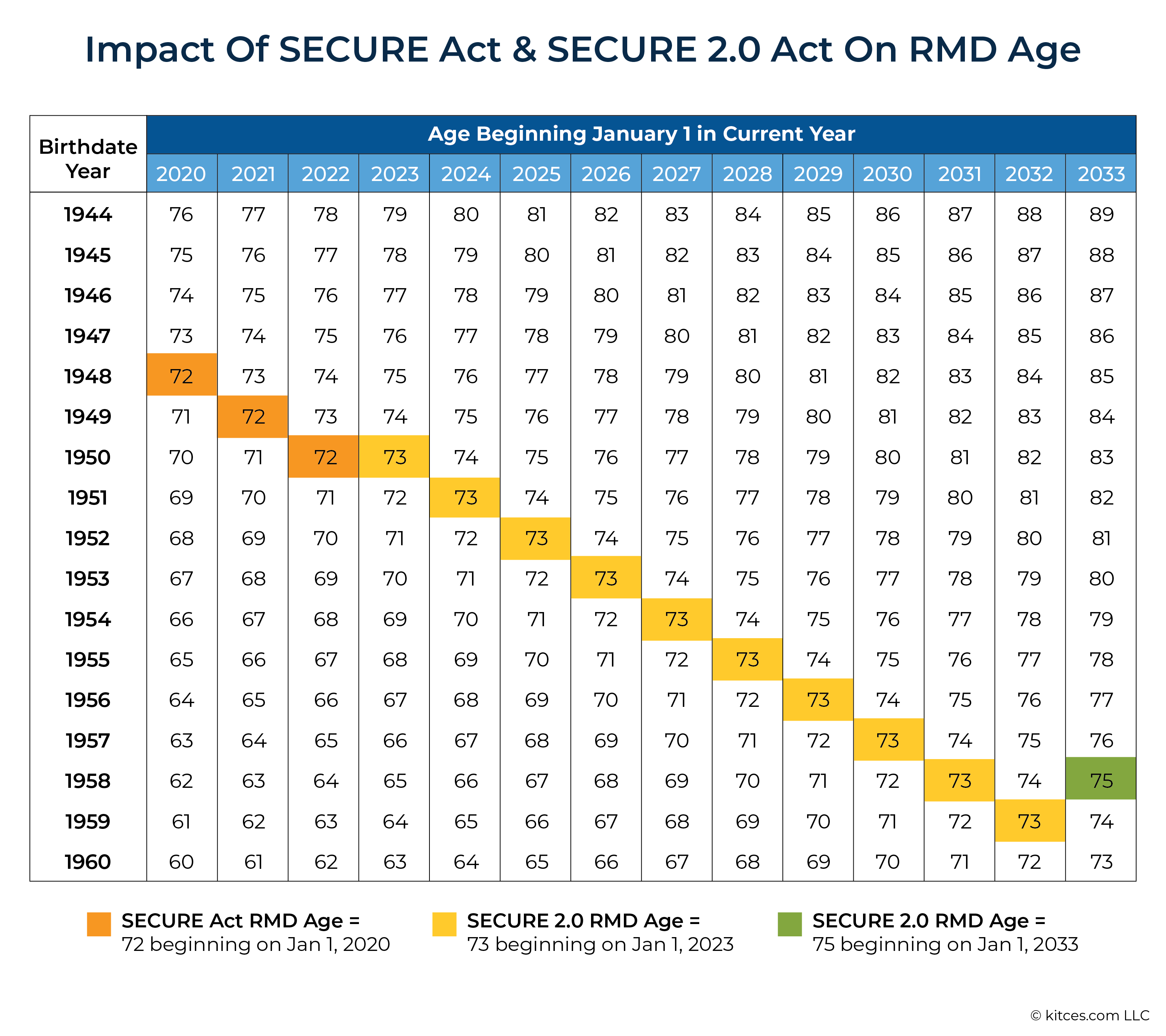

The Transition from 72 to 73

As of January 1, 2023, the age to begin taking RMDs increased to 73. This change specifically applies to individuals who turned 72 after December 31, 2022. If you reached age 72 in 2022 or earlier, you were already required to begin your distributions under the previous rules and must continue to do so. This one-year bump provides a brief but valuable window for retirees to perform additional tax planning, such as Roth conversions, before the mandatory distributions begin to impact their taxable income.

Looking Ahead: The Jump to Age 75 in 2033

The SECURE 2.0 Act did not stop at age 73. It established a secondary tier for younger workers. For those born in 1960 or later, the RMD age is scheduled to increase to 75 starting in the year 2033. This staggered implementation means that financial planning is now highly personalized. A couple where one spouse was born in 1959 and the other in 1960 will find themselves navigating two different sets of federal mandates, requiring a sophisticated approach to their joint withdrawal strategy.

Why the IRS Mandates Required Minimum Distributions

To manage your finances effectively, it is helpful to understand the “why” behind the RMD. Retirement accounts like Traditional IRAs and 401(k)s offer tax breaks on the “front end”—contributions are often tax-deductible, and growth is tax-deferred. The IRS views this as a temporary loan of tax revenue. RMDs are the mechanism by which the government ensures that these funds are eventually withdrawn and taxed as ordinary income, rather than being passed down indefinitely as a tax-free legacy vehicle.

Calculating Your Required Minimum Distribution (RMD)

Knowing the age at which you must start is only half the battle; the second half is determining exactly how much you are required to take. The IRS does not set a flat percentage for everyone. Instead, the amount is calculated based on your account balance and your projected life expectancy.

The Role of Life Expectancy Tables

The IRS provides specific “Life Expectancy Tables” to help taxpayers calculate their RMDs. The most commonly used is the Uniform Lifetime Table, which is designed for unmarried owners, married owners whose spouses are not more than 10 years younger, and married owners whose spouses are not the sole beneficiaries of their IRAs. Each year, you find the “distribution period” (a divisor) that corresponds to your age. As you get older, the divisor decreases, which means the percentage of the account you must withdraw increases.

Determining Account Balances for Calculation

The RMD for a given year is based on the fair market value of your retirement accounts as of December 31 of the previous year. For example, if you are calculating your RMD for 2024, you must look at the total value of your eligible accounts on December 31, 2023. This creates a potential pitfall: if the stock market experiences a significant downturn early in the year, your RMD (based on the previous year’s high balance) might represent a larger-than-expected percentage of your current portfolio.

The April 1st Deadline for the First Distribution

While RMDs are generally due by December 31 each year, the IRS offers a one-time grace period for your very first distribution. You have the option to delay your first RMD until April 1 of the year following the year you reach the required age. However, caution is advised. If you delay your first RMD to April 1, you will still be required to take your second RMD by December 31 of that same year. Doubling up on distributions in a single tax year can push you into a higher tax bracket and potentially increase your Medicare premiums.

Tax Implications and Penalties for Non-Compliance

From a personal finance perspective, RMDs are significant because they are treated as ordinary income. They are not taxed at the more favorable long-term capital gains rates. This mandatory influx of cash can create a “tax torpedo” for the unwary.

How RMDs Impact Your Tax Bracket

For many retirees, their RMDs may exceed their actual lifestyle needs. This “forced income” can unintentionally push a taxpayer from the 12% or 22% bracket into a higher tier. Furthermore, because RMDs increase your Adjusted Gross Income (AGI), they can trigger the taxation of Social Security benefits. Many retirees find that once RMDs begin, their effective tax rate is higher in retirement than it was during their working years.

The Cost of Procrastination: The Excise Tax Penalty

Historically, the penalty for failing to take an RMD was one of the most draconian in the tax code: 50% of the amount that should have been withdrawn. Fortunately, the SECURE 2.0 Act reduced this penalty to 25%. Furthermore, if the error is corrected in a “timely manner” (generally within two years), the penalty may be further reduced to 10%. While less severe than before, a 10% to 25% loss of principal is still a significant blow to a retirement nest egg and should be avoided through meticulous record-keeping.

Impact on Medicare Premiums (IRMAA)

An overlooked aspect of RMDs is their impact on Medicare Part B and Part D premiums. If your RMD pushes your income over certain thresholds, you may be subject to the Income-Related Monthly Adjustment Amount (IRMAA). This is essentially a surcharge on your healthcare costs. Because IRMAA is based on tax returns from two years prior, a large RMD at age 73 can lead to significantly higher healthcare costs at age 75.

Strategic Financial Planning for RMD Management

Because RMDs are mandatory, savvy investors look for ways to fulfill the requirement while minimizing the tax damage. There are several advanced strategies that can help manage the impact of these distributions.

Utilizing Qualified Charitable Distributions (QCDs)

If you are charitably inclined and at least 70½ years old, you can utilize a Qualified Charitable Distribution (QCD). This allows you to transfer up to $105,000 (indexed for inflation) per year directly from your IRA to a qualified 501(c)(3) charity. The beauty of the QCD is that the amount transferred counts toward your RMD but is not included in your adjusted gross income. This is often more tax-efficient than taking the RMD as income and then claiming a charitable deduction.

The Benefits of Roth Conversions Before RMD Age

Because Roth IRAs do not have RMD requirements for the original owner, many financial advisors recommend “filling up” lower tax brackets with Roth conversions in the years between retirement and the start of RMDs. By paying taxes now at a known rate, you reduce the balance of your Traditional IRA, thereby reducing the size of your future mandatory distributions and creating a tax-free bucket for your heirs.

Aggregating RMDs Across Multiple Accounts

If you have multiple Traditional IRAs, the IRS allows you to calculate the RMD for each account separately but withdraw the total amount from just one (or any combination) of the IRAs. This provides flexibility; you can choose to liquidate assets from an underperforming account while leaving a high-growth account untouched. Note, however, that this “aggregation rule” does not apply to 401(k)s or 403(b)s; RMDs for those employer-sponsored plans must be taken from each specific account.

Exceptions and Special Considerations

While the rules for RMDs are rigid, there are a few notable exceptions that can provide relief for specific types of accounts and employment situations.

The “Still Working” Exception for 401(k) Plans

If you are still employed at age 73 and do not own more than 5% of the company you work for, you may be able to delay RMDs from your current employer’s 401(k) or 403(b) until you actually retire. This exception does not apply to IRAs or retirement plans from previous employers. This rule allows high-earners who continue to work into their 70s to keep their current workplace savings growing tax-deferred for as long as they remain on the payroll.

Inherited IRAs and the 10-Year Rule

The rules for RMDs on inherited accounts are entirely different and were significantly altered by the original SECURE Act. Most non-spouse beneficiaries are now required to fully distribute the contents of an inherited IRA within 10 years of the original owner’s death. While they may not have a specific “minimum” amount to take each year during that decade, the entire balance must be zeroed out by the end of the tenth year, which often necessitates strategic annual withdrawals to avoid a massive tax bill in year ten.

Roth IRAs: The Exception to the RMD Rule

It is important to reiterate that Roth IRAs are the most powerful tool for avoiding RMDs. Under current law, the original owner of a Roth IRA is never required to take distributions. This makes the Roth IRA an ideal vehicle for both long-term tax-free growth and for passing wealth to the next generation. For those worried about the “tax trap” of RMD age, prioritizing Roth contributions or conversions remains the most effective hedge against future mandatory withdrawals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.