The concept of retirement has evolved from a simple cessation of labor into a complex financial milestone known as Full Retirement Age (FRA). For anyone navigating the landscape of personal finance, understanding the specific age at which the government and financial institutions deem you “fully retired” is critical. It is the pivot point upon which your Social Security benefits, tax strategies, and portfolio withdrawal rates turn.

Full Retirement Age is not a suggestion; it is a calculated actuarial benchmark that determines when you are entitled to 100% of your primary insurance amount. In the context of modern financial planning, reaching this age represents the transition from the accumulation phase of life to the distribution phase. This article explores the nuances of FRA, the financial implications of timing, and how to integrate this number into a robust long-term wealth strategy.

Defining Full Retirement Age (FRA) and Its Economic Foundations

At its core, Full Retirement Age is the age at which an individual becomes eligible to receive unreduced Social Security retirement benefits. While many people associate “retirement” with the age of 65, that benchmark has shifted significantly due to legislative changes designed to preserve the solvency of the Social Security trust funds.

The Legislative Evolution of FRA

The Social Security Act of 1935 originally set the retirement age at 65. However, as life expectancy increased and the ratio of workers to retirees shifted, the federal government realized that the original model was unsustainable. The Social Security Amendments of 1983 introduced a gradual increase in the FRA. This was a strategic move to adjust for the fact that Americans were living longer and drawing benefits for more extended periods. Today, the FRA is no longer a static number but a moving target based on the year you were born.

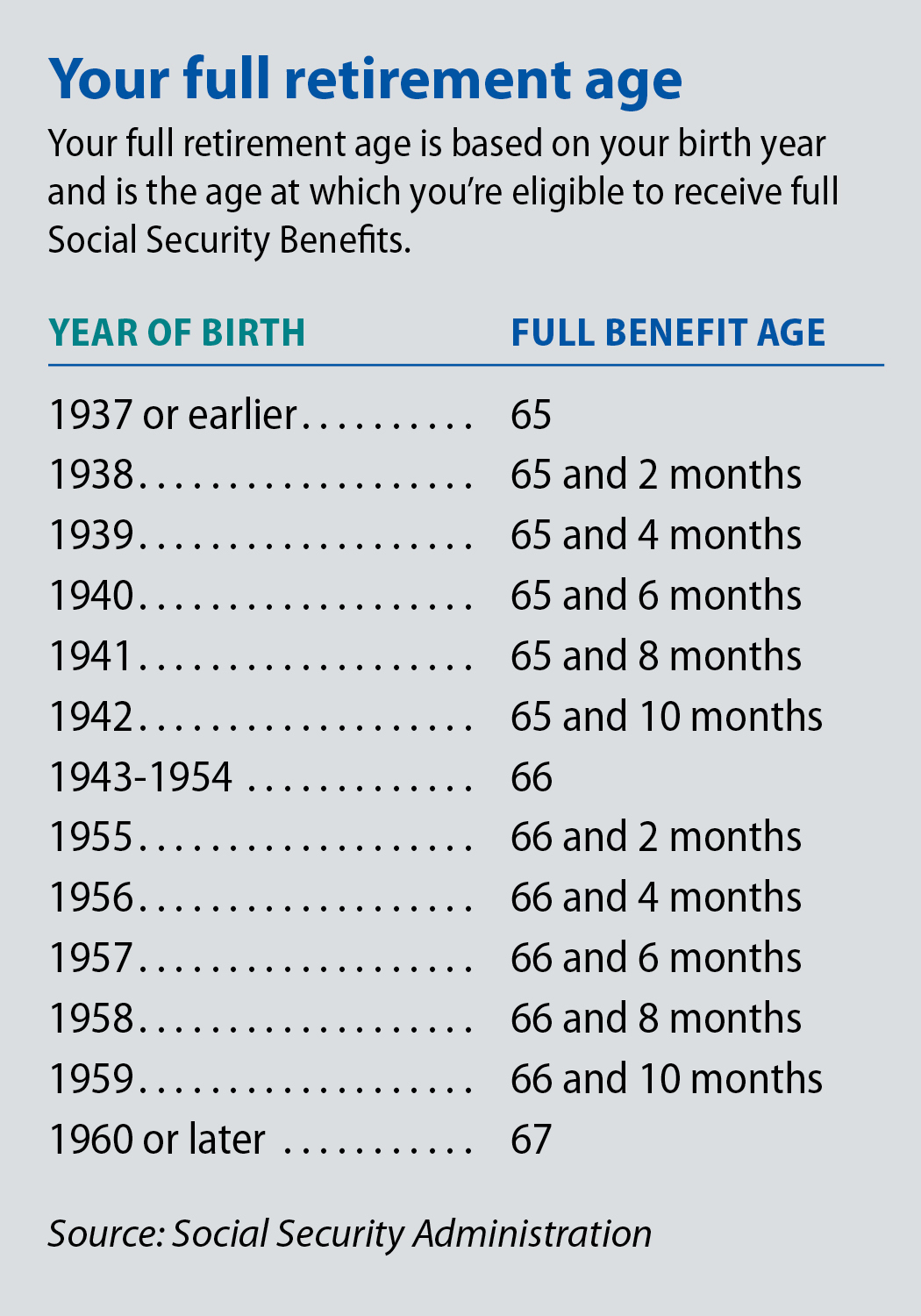

How Your Birth Year Dictates Your Financial Timeline

For those born between 1943 and 1954, the FRA was a clean 66 years. However, for those born in 1955 and later, the age increases in two-month increments. For example, if you were born in 1956, your FRA is 66 and 4 months. If you were born in 1959, it is 66 and 10 months. For everyone born in 1960 or later, the Full Retirement Age is currently set at 67. Understanding exactly where you fall on this spectrum is the first step in calculating your “burn rate” and determining when you can safely exit the workforce without leaving money on the table.

Strategic Timing: The Financial Impact of When You Claim

In personal finance, timing is often as important as the amount invested. Choosing when to claim benefits relative to your Full Retirement Age is one of the most significant financial decisions a person will make. The Social Security Administration offers a window—starting as early as age 62 and extending to age 70—but the FRA serves as the “neutral” baseline.

The Cost of Early Retirement

While you can technically retire and begin drawing benefits at age 62, doing so comes with a permanent financial penalty. If your FRA is 67 and you choose to claim at 62, your monthly benefit is reduced by approximately 30%. This reduction is actuarial; it is designed to account for the fact that you will likely receive checks for five additional years. However, from a wealth-building perspective, this reduction can significantly hamper your lifestyle in later years, especially when factoring in the compounding effect of Cost-of-Living Adjustments (COLAs), which are calculated based on your initial benefit amount.

The Bonus of Delayed Retirement

Conversely, there is a substantial financial incentive for those who can afford to wait past their FRA. For every year you delay claiming benefits beyond your Full Retirement Age, up until age 70, your benefit increases by approximately 8% per year. This is known as “Delayed Retirement Credits.” In a low-yield environment, a guaranteed 8% annual return is virtually unheard of in other asset classes. For an individual with an FRA of 67 who waits until 70, their monthly check will be 24% larger than if they had claimed at their “full” age. This strategy is often utilized by high-net-worth individuals to create a higher “floor” of guaranteed, inflation-adjusted income.

Integrating FRA into Your Broader Personal Finance Strategy

Full Retirement Age should not be viewed in a vacuum. It must be synchronized with your other financial engines, such as 401(k) plans, IRAs, and taxable brokerage accounts. A sophisticated financial plan treats the FRA as a secondary “tax and liquidity” gate.

Coordinating Social Security with Private Portfolios

A common strategy in modern finance is the “bridge strategy.” This involves using withdrawals from a 401(k) or traditional IRA to fund the years between your actual retirement date and your FRA (or age 70). By drawing down private assets first, you allow your Social Security benefit to grow via delayed credits. This approach also helps manage the sequence of returns risk—the danger that a market downturn early in retirement could deplete your portfolio. By securing a higher Social Security “paycheck” later, you reduce the long-term pressure on your invested capital.

Working While Receiving Benefits: The Earnings Test

One of the most critical reasons to know your FRA is the Social Security Earnings Test. If you claim benefits before reaching your FRA and continue to work, the government may temporarily withhold a portion of your benefits if your earnings exceed a certain threshold. In 2024, for example, if you are under FRA, the SSA deducts $1 from your benefits for every $2 you earn above the annual limit. However, once you reach the month of your Full Retirement Age, this “tax” disappears entirely. You can earn an unlimited amount of income without any reduction in your Social Security checks. This makes the FRA a liberation point for professionals who wish to transition into consulting or part-time “passion projects” without financial penalty.

Tax Implications and the “Social Security Torpedo”

Understanding the age of full retirement is also a matter of tax efficiency. The way Social Security is taxed depends heavily on your “provisional income,” which includes your Adjusted Gross Income (AGI), tax-exempt interest, and half of your Social Security benefits.

Navigating the 85% Tax Bracket

As you approach and pass your FRA, your withdrawal strategy from tax-deferred accounts can push you into a higher tax bracket for your Social Security benefits. Up to 85% of your Social Security can be subject to federal income tax if your provisional income exceeds certain levels ($34,000 for individuals, $44,000 for joint filers). Financial experts often recommend shifting some assets into Roth IRAs or municipal bonds prior to reaching FRA to lower your AGI, thereby protecting your Social Security income from excessive taxation.

Medicare and the FRA Disconnect

It is a common misconception that Medicare and Full Retirement Age are linked. They are not. Medicare eligibility remains at 65, regardless of your FRA for Social Security. Failing to understand this distinction can be a costly mistake. If you wait until your FRA of 67 to look into healthcare, you may face late-enrollment penalties for Medicare Part B and Part D that last a lifetime. A sound financial plan accounts for the “gap years” between Medicare eligibility at 65 and Full Retirement Age at 67.

The Future of Retirement: Shifts in Policy and Longevity

The definition of “full retirement” is not set in stone. As economic conditions shift and the “Silver Tsunami” of retiring Baby Boomers puts pressure on federal budgets, the financial community is bracing for potential changes to the FRA.

Will the FRA Increase to 70?

There is ongoing debate in Washington regarding raising the FRA to 68, 69, or even 70 for younger generations. From a purely mathematical standpoint, increasing the age is one of the most effective ways to ensure the longevity of the Social Security system. For Gen X, Millennials, and Gen Z, the “full retirement age” mentioned in current charts may be optimistic. Financial planning for these groups should involve “stress-testing” their retirement models by assuming a later FRA or a reduced benefit amount to ensure their private savings can cover the potential shortfall.

Longevity Risk and the New Retirement Paradigm

The ultimate goal of knowing your FRA is to mitigate “longevity risk”—the risk of outliving your money. As medical technology advances, the possibility of a 30-year retirement becomes more likely. In this context, the FRA serves as a strategic marker. While 67 is the legal definition of full retirement, many financial advisors now suggest that 70 is the “new 65” for those seeking to maximize their guaranteed income. By treating the FRA as a milestone rather than a finish line, investors can build more resilient, multi-decade financial plans that account for inflation, healthcare costs, and market volatility.

In summary, the question of “what age is considered full retirement” is answered not just by a date on a calendar, but by a comprehensive understanding of how that date influences your entire financial ecosystem. Whether you are 25 or 65, your Full Retirement Age is the anchor of your retirement planning, dictating your claiming strategy, your tax liability, and the sustainability of your wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.