In the world of business finance, understanding the nomenclature of the balance sheet is fundamental to grasping a company’s health. One of the most frequently asked questions by new entrepreneurs and finance students is: “What account is accounts receivable?” While it might seem like a simple ledger entry, Accounts Receivable (AR) represents the lifeblood of a company’s cash flow and serves as a primary indicator of its operational efficiency.

At its core, Accounts Receivable is a Current Asset account. It represents money owed to a business by its customers for goods or services delivered but not yet paid for. Because these balances are typically expected to be converted into cash within a single fiscal year (or operating cycle), they are categorized as short-term assets. This article explores the strategic importance of AR in business finance, its role in accrual accounting, and how managing this account effectively can determine the solvency of an organization.

1. Defining the Asset: The Role of Accounts Receivable in Business Finance

To understand what account Accounts Receivable belongs to, one must first understand the fundamental accounting equation: Assets = Liabilities + Equity. Accounts Receivable sits firmly on the “Assets” side of the ledger.

The Anatomy of a Current Asset

A current asset is any resource that a company expects to convert into cash, sell, or consume within one year. Accounts Receivable is often the most significant current asset a business possesses, right after cash itself. It represents a legal obligation from a debtor to pay the creditor. In the hierarchy of liquidity, AR is considered highly liquid, though it ranks below cash and short-term investments because it requires an extra step (collection) before the value can be utilized.

Accrual vs. Cash Basis Accounting

The existence of an Accounts Receivable account is a hallmark of the accrual basis of accounting. In cash-basis accounting, revenue is only recorded when money hits the bank. However, in accrual accounting—which is the standard for most mid-to-large-scale businesses—revenue is recognized when it is earned, regardless of when the cash is received. When a service is performed on credit, the “Accounts Receivable” account is debited, and “Revenue” is credited. This allows businesses to match their income with the expenses incurred to generate that income during a specific period.

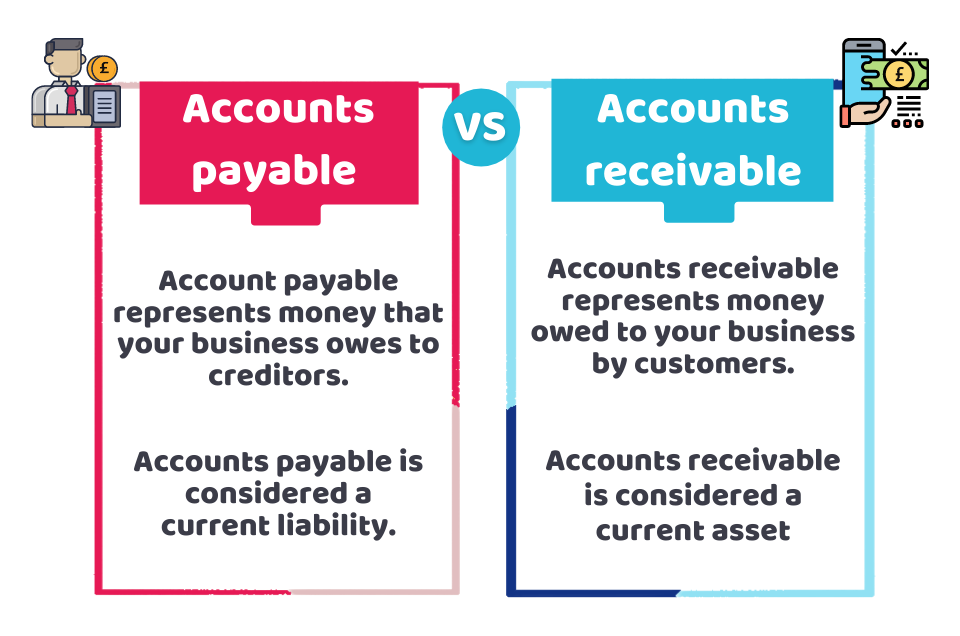

Accounts Receivable vs. Accounts Payable

It is common for beginners to confuse Accounts Receivable with its counterpart, Accounts Payable (AP). While AR is an asset representing money coming in, Accounts Payable is a liability representing money going out to suppliers or vendors. Managing the “spread” or the timing between these two accounts is the essence of working capital management. A healthy business seeks to collect its AR faster than it is required to pay its AP.

2. The Lifecycle of an Accounts Receivable Entry

The journey of an AR entry begins long before a bill is sent and ends only when the bank reconciliation is complete. Understanding this lifecycle is crucial for maintaining financial integrity.

Extending Credit and the Sales Invoice

The process begins when a business decides to offer “net terms” to a customer (e.g., Net 30, meaning payment is due in 30 days). Once the product is shipped or the service is rendered, an invoice is generated. This invoice acts as the source document for the accounting entry. From a financial perspective, the company has “sold” its inventory or time in exchange for a “promise to pay.”

The Journal Entry Process

When the sale occurs, the accountant records a debit to the Accounts Receivable account. This increases the total value of the company’s assets. Simultaneously, a credit is made to the Sales Revenue account, which eventually flows into the Income Statement. When the customer finally pays the bill, the company records a debit to Cash (increasing assets) and a credit to Accounts Receivable (decreasing the asset). The net effect is that one asset (a promise) has been exchanged for another asset (cold hard cash).

Subsidiary Ledgers and the General Ledger

In a complex business, the “Accounts Receivable” line item on the balance sheet is actually a summary. Behind it lies a “Subsidiary Ledger” that tracks exactly how much each individual customer owes. Maintaining this level of detail is vital for personal branding and relationship management; charging a customer twice or failing to credit a payment can damage a company’s professional reputation and financial credibility.

3. Measuring Financial Health Through AR Metrics

Simply knowing that Accounts Receivable is an asset isn’t enough; financial managers must also know how “hard” that asset is working. Because AR is not yet cash, its value is theoretical until collected.

The Importance of the AR Aging Report

The Aging Report is a financial tool that categorizes AR balances based on how long an invoice has been outstanding (e.g., 0–30 days, 31–60 days, 61–90 days, and 90+ days). This report is a diagnostic tool for business finance. If a significant portion of the AR falls into the 90+ category, it signals a breakdown in the collection process or potential issues with customer creditworthiness.

Days Sales Outstanding (DSO)

DSO is a key performance indicator (KPI) that measures the average number of days it takes a company to collect payment after a sale has been made. A low DSO indicates that the company is efficient in its collections and has high-quality customers. A rising DSO often suggests that the business is over-extending credit or that its customers are struggling financially, which can lead to a “cash crunch” even if the business is technically profitable on paper.

The Cash Conversion Cycle (CCC)

The Cash Conversion Cycle measures how long it takes for a company to convert its investments in inventory and other resources into cash flows from sales. Accounts Receivable is a critical component of this formula. By shortening the time an invoice sits in the AR account, a business improves its liquidity and reduces the need for external financing or high-interest lines of credit.

4. Risks and Realities: Bad Debt and Valuations

While Accounts Receivable is an asset, it is also a risk. Not every customer who receives an invoice will pay it. Accounting for this reality is a sophisticated part of business finance.

The Allowance for Doubtful Accounts

To adhere to the principle of conservatism in accounting, businesses must not overstate the value of their assets. Therefore, they create a contra-asset account known as the “Allowance for Doubtful Accounts.” This account reduces the total Accounts Receivable to its “Net Realizable Value”—the amount the company realistically expects to collect.

Writing Off Bad Debt

When a specific invoice is deemed uncollectible (perhaps due to a customer’s bankruptcy), the business must “write it off.” This involves removing the balance from the Accounts Receivable account and recognizing a Bad Debt Expense on the income statement. For a business owner, high bad debt expenses are a red flag that the credit policy is too lenient or that the market environment is deteriorating.

AR as Collateral and Factoring

In the world of online income and side hustles, or even major corporate finance, Accounts Receivable can be used as leverage. “Factoring” is a financial transaction where a business sells its accounts receivable to a third party (a factor) at a discount. This provides immediate cash flow, although at the cost of a percentage of the revenue. Additionally, many banks will lend money to businesses using their AR as collateral, provided the aging report shows high-quality, current balances.

5. Strategic Management: Turning Receivables into Cash Flow

Effective management of the Accounts Receivable account is what separates a thriving business from one that is “profit rich but cash poor.”

Streamlining the Billing Process

The faster an invoice is sent, the faster it can be paid. Strategic financial management involves automating the billing process to ensure invoices are accurate and delivered immediately upon the completion of work. Errors in invoicing are one of the primary reasons for payment delays, leading to inflated AR balances that don’t reflect actual collectible value.

Implementing Proactive Credit Policies

Before allowing a customer to add to the Accounts Receivable account, businesses should conduct credit checks. Establishing clear credit limits and terms ensures that the “Asset” on the balance sheet is composed of reliable promises from stable entities. In the realm of personal branding and professional services, setting clear expectations regarding payment terms is essential for maintaining a professional image and ensuring a steady stream of income.

Incentivizing Early Payments

Many businesses offer discounts to improve their AR turnover (e.g., “2/10, Net 30,” which offers a 2% discount if paid within 10 days). While this slightly reduces the total revenue, the increase in liquidity and the reduction in collection risk often make it a wise financial move. In business finance, “cash today” is almost always more valuable than “cash tomorrow” due to the time value of money and the ability to reinvest that capital into growth opportunities.

In conclusion, “Accounts Receivable” is far more than just a line item on a balance sheet; it is a dynamic indicator of a company’s operational health and financial strategy. As a Current Asset, it represents the future cash flows that will sustain the business. By understanding how to categorize, track, and optimize this account, business owners and financial professionals can ensure that their organization remains liquid, solvent, and ready for long-term growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.