Discovering that you owe the Internal Revenue Service (IRS) more than you can afford to pay is a stressful experience that millions of taxpayers face every year. Whether it stems from an unexpected windfall, a mistake in withholding, or the complexities of self-employment income, tax debt can feel like an insurmountable weight. However, the IRS is not merely a collection agency; it is a massive bureaucratic entity that prefers consistent, predictable payments over the high costs of aggressive collection actions like levies or liens.

For those in the “Money” niche—investors, small business owners, and proactive individuals—understanding the mechanics of IRS installment agreements is a vital component of financial literacy. Setting up a payment plan is not an admission of defeat; it is a strategic financial move to protect your credit, your assets, and your peace of mind. This guide provides a deep dive into the types of plans available, the application process, and the long-term financial implications of managing tax debt.

Understanding Your Options: The Different Types of IRS Installment Agreements

Before clicking “apply” on the IRS website, you must understand that not all payment plans are created equal. The IRS offers several “Installment Agreements” (IAs) tailored to different financial situations and debt totals. Choosing the right one can save you thousands in setup fees and administrative headaches.

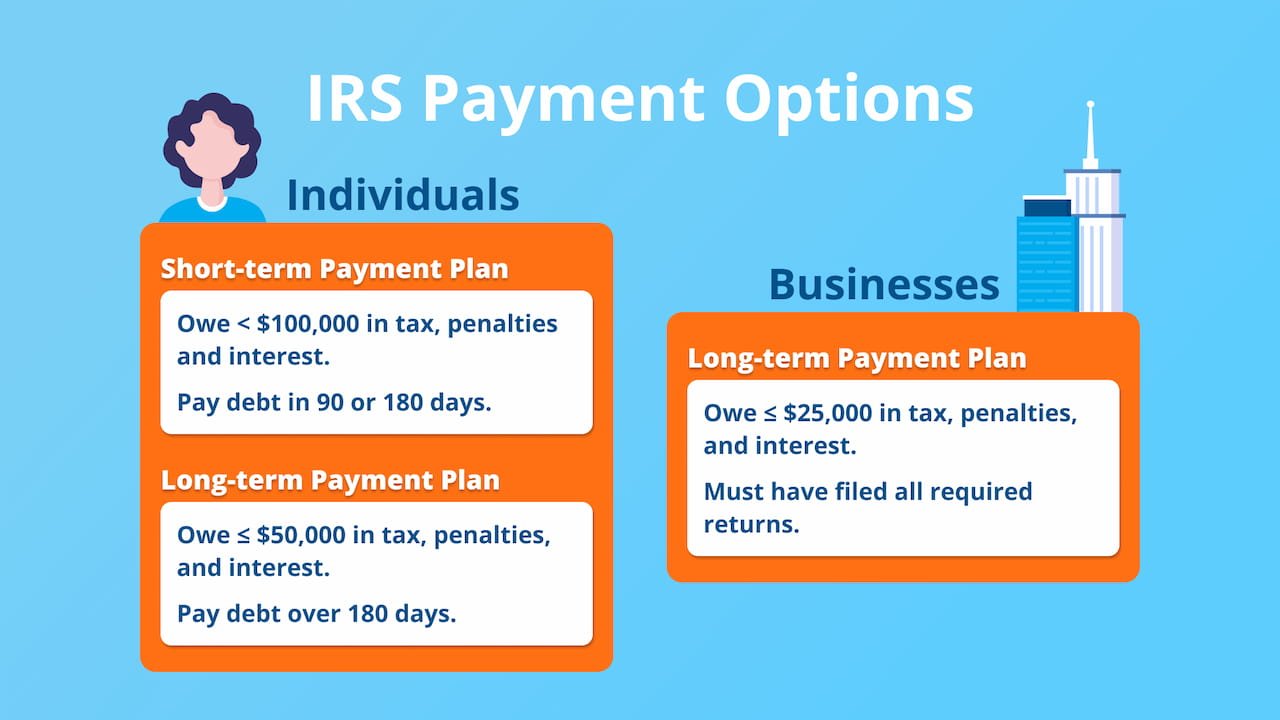

Short-Term Payment Plans (180 Days or Less)

If you find yourself in a temporary liquidity crunch—perhaps you are waiting for a real estate closing or an investment to mature—the short-term payment plan is often the most cost-effective route. This plan gives you up to 180 days to pay your liability in full, including accrued interest and penalties.

The primary advantage of the short-term plan is the cost: there is no setup fee. From a personal finance perspective, this is almost always preferable to taking out a high-interest personal loan or charging the debt to a credit card. However, you must be certain you can clear the balance within the six-month window, as failure to do so may lead to more stringent requirements later.

Long-Term Payment Plans (Installment Agreements)

For those who need more than six months to settle their debt, the IRS offers long-term installment agreements. These plans allow for monthly payments over a period of up to 72 months (six years). While these plans provide significant breathing room, they come with setup fees that vary based on how you apply and how you choose to pay.

There are two main sub-categories here:

- Direct Debit Installment Agreements (DDIA): This is the IRS’s preferred method. Payments are automatically deducted from your bank account. It carries the lowest setup fee and is often required if your debt exceeds certain thresholds.

- Standard Installment Agreements: You pay monthly via check, money order, or the Online Payment System. These carry higher setup fees because they require more administrative oversight from the IRS.

Streamlined Installment Agreements

For individual taxpayers who owe $50,000 or less (including tax, penalties, and interest), the IRS offers “Streamlined” processing. The benefit of a streamlined agreement is that you generally do not have to provide the IRS with a detailed financial statement (Form 433-F). This prevents the IRS from digging into your equity, expenses, and asset base, making the approval process much faster and less intrusive.

The Step-by-Step Process to Applying for an IRS Payment Plan

Once you have identified the plan that fits your budget, the application process requires precision. Errors in the application can lead to delays, which in turn allow interest to compound further.

Gathering Necessary Financial Documentation

Before beginning the application, you must ensure all your tax returns are filed. The IRS will not approve a payment plan if you have unfiled returns from previous years. Compliance is the prerequisite for cooperation. You will need your total debt amount (found on your most recent notice), your Social Security Number or ITIN, and your bank routing and account numbers if you are opting for direct debit.

If you owe more than $50,000, be prepared to fill out Form 433-F, the Collection Information Statement. This document requires a comprehensive breakdown of your monthly income, living expenses, and the value of your assets. In the world of business finance, this is akin to a full audit of your personal balance sheet.

Using the Online Payment Agreement (OPA) Tool

The most efficient way to set up a plan is through the IRS Online Payment Agreement tool. Available on the IRS.gov website, this tool provides immediate notification of whether your plan has been accepted.

The digital interface is designed to guide you through the selection process. You will enter your proposed monthly payment amount and your preferred payment date. A professional tip: always propose a payment amount that you are 100% certain you can meet. It is easier to pay more than your minimum requirement voluntarily than it is to lower a mandated payment amount once the agreement is signed.

Applying via Form 9465 (Paper Application)

While the online tool is faster, some situations require the filing of Form 9465, “Installment Agreement Request.” This is typically used if you cannot use the online system or if you are submitting the request along with a physical tax return. When filing Form 9465, it is wise to include the first month’s payment with the application to demonstrate “good faith.” This proactive approach can sometimes expedite approval and show the revenue officer that you are serious about debt resolution.

Associated Costs, Interest, and Penalties: What to Expect

A common misconception in personal finance is that a payment plan “stops the bleeding.” While it stops aggressive collection actions, it does not stop the accrual of costs. Understanding the “cost of capital” when borrowing from the IRS is essential.

Setup Fees and User Fees

The IRS charges a fee to establish an installment agreement. As of the current fiscal period, these fees can range from $31 for an online direct debit setup to over $200 for a paper-based non-direct debit setup. For savvy financial planners, the takeaway is clear: always apply online and always choose direct debit to minimize these sunk costs.

Accruing Interest and Failure-to-Pay Penalties

Even with an approved plan, the IRS continues to charge interest and penalties on the unpaid balance. The interest rate is set quarterly and is typically the federal short-term rate plus 3%. Additionally, the failure-to-pay penalty is usually 0.5% per month.

However, there is a silver lining: once an installment agreement is approved for an individual who filed their return on time, the failure-to-pay penalty is often reduced to 0.25% per month. Over a several-year period, this reduction can save a taxpayer a significant amount of money, making the formal agreement far superior to simply “sending what you can” without a plan.

Low-Income Taxpayer Waivers

For those facing genuine financial hardship, the IRS offers fee waivers or reimbursements for the setup costs. If your income falls below 250% of the federal poverty guidelines, you may qualify for a “low-income taxpayer” status. This status can waive the setup fee entirely or cap it at a significantly lower rate, ensuring that the path to financial recovery isn’t blocked by the very fees intended to manage it.

Maintaining Your Agreement and Avoiding Default

The hardest part of an IRS payment plan isn’t the setup—it’s the maintenance. A single missed payment or a failure to file a future tax return can trigger a “Default Notice,” which can lead to the termination of the agreement and the immediate initiation of levies on bank accounts or wages.

Keeping Up with Future Filing Requirements

The most critical condition of any IRS payment plan is “future compliance.” This means you must file all future tax returns on time and pay all future taxes in full. If you owe money again the following year, you are technically in default of your current agreement. For freelancers and business owners, this necessitates a rigorous approach to quarterly estimated payments to ensure that next year’s tax bill doesn’t jeopardize this year’s payment plan.

Payment Methods: Direct Debit vs. Manual Payments

While we have touched on the cost benefits of Direct Debit, the “behavioral finance” benefit is even greater. Automating your tax debt payment treats it like a fixed mortgage or utility bill. It removes the psychological friction of manually sending money to the government every month. If you must pay manually, using the IRS Direct Pay system is preferable to mailing checks, as it provides an immediate digital receipt and reduces the risk of payments getting lost in the mail.

What Happens if You Miss a Payment?

Life happens. If you realize you cannot make a monthly payment, the worst thing you can do is ignore it. You should contact the IRS immediately. In some cases, they can grant a one-time skip or a temporary restructuring of the plan. If the plan defaults, you usually have 30 days to appeal or rectify the situation before the IRS resumes collection activities. Reinstating a defaulted agreement usually incurs another fee, making consistency the most profitable strategy.

Conclusion: Financial Empowerment Through Structure

Managing tax debt is an exercise in disciplined financial management. By setting up a formal payment plan with the IRS, you are taking control of a volatile situation and turning it into a manageable line item in your monthly budget.

While the goal of any sound financial strategy is to avoid tax debt through proper withholding and estimated payments, the IRS installment agreement serves as a vital safety net. It protects your credit score by preventing federal tax liens and provides a clear, structured path back to “tax-neutral” status. In the grand scheme of personal finance, the ability to navigate the complexities of the IRS is a sign of financial maturity. By understanding the types of plans, the application nuances, and the costs involved, you can move from a state of financial anxiety to a state of structured resolution.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.