In the landscape of modern personal finance, few sequences of digits are as ubiquitous yet as misunderstood as the routing number. Whether you are setting up your first paycheck via direct deposit, paying your monthly mortgage through an automated portal, or wiring funds for a significant investment, the routing number serves as the invisible bridge connecting your capital to its destination.

While it may seem like a mere string of random digits found at the bottom of a check, the routing number—often referred to officially as an American Bankers Association (ABA) Routing Transit Number (RTN)—is a sophisticated tool of the financial industry. Understanding how to locate, use, and protect this number is a fundamental pillar of financial literacy. This guide explores the depths of the routing number, providing the insights necessary to manage your money with precision and security.

Understanding the Anatomy and Purpose of Routing Numbers

Before one can master the “how” of routing numbers, one must understand the “what.” In the United States, the routing number is a nine-digit code used to identify a specific financial institution in a transaction. This system was developed by the American Bankers Association in 1910 to simplify the sorting and shipment of paper checks, but it has since evolved into the backbone of digital banking.

What is a Routing Number?

At its core, a routing number is an address for a bank. Just as a zip code helps the postal service deliver a letter to the right town, the routing number tells the Federal Reserve and other financial institutions exactly where to send a electronic payment or a physical check. Every bank or credit union that is federally or state-chartered and maintains an account with a Federal Reserve Bank is assigned at least one routing number. Larger institutions often have multiple routing numbers assigned to different regions or specific types of transactions, such as wire transfers versus ACH (Automated Clearing House) transfers.

The American Bankers Association (ABA) System

The nine-digit sequence is not arbitrary; it follows a strict mathematical formula.

- The first two digits represent the Federal Reserve district where the bank is located.

- The third digit identifies the Federal Reserve check processing center assigned to the bank.

- The fourth digit indicates the state in which the bank is located.

- The fifth through eighth digits are unique identifiers for the specific bank.

- The ninth digit is a “check digit,” a complex mathematical calculation of the previous eight digits used to verify that the number is valid and has not been mistyped.

Transit vs. Account Numbers: Knowing the Difference

It is a common error to confuse the routing number with the account number. While the routing number identifies the bank, the account number identifies you. Think of the routing number as the apartment building’s street address and the account number as your specific unit number. To complete a transaction, both are required. Providing only one is like sending a letter to “Apartment 4B” without a street address—it simply will not arrive.

How to Find Your Routing Number: A Step-by-Step Guide

In an era of paperless banking, many consumers no longer carry a checkbook. Consequently, locating a routing number can feel like a scavenger hunt. However, financial institutions provide several touchpoints where this information is readily accessible.

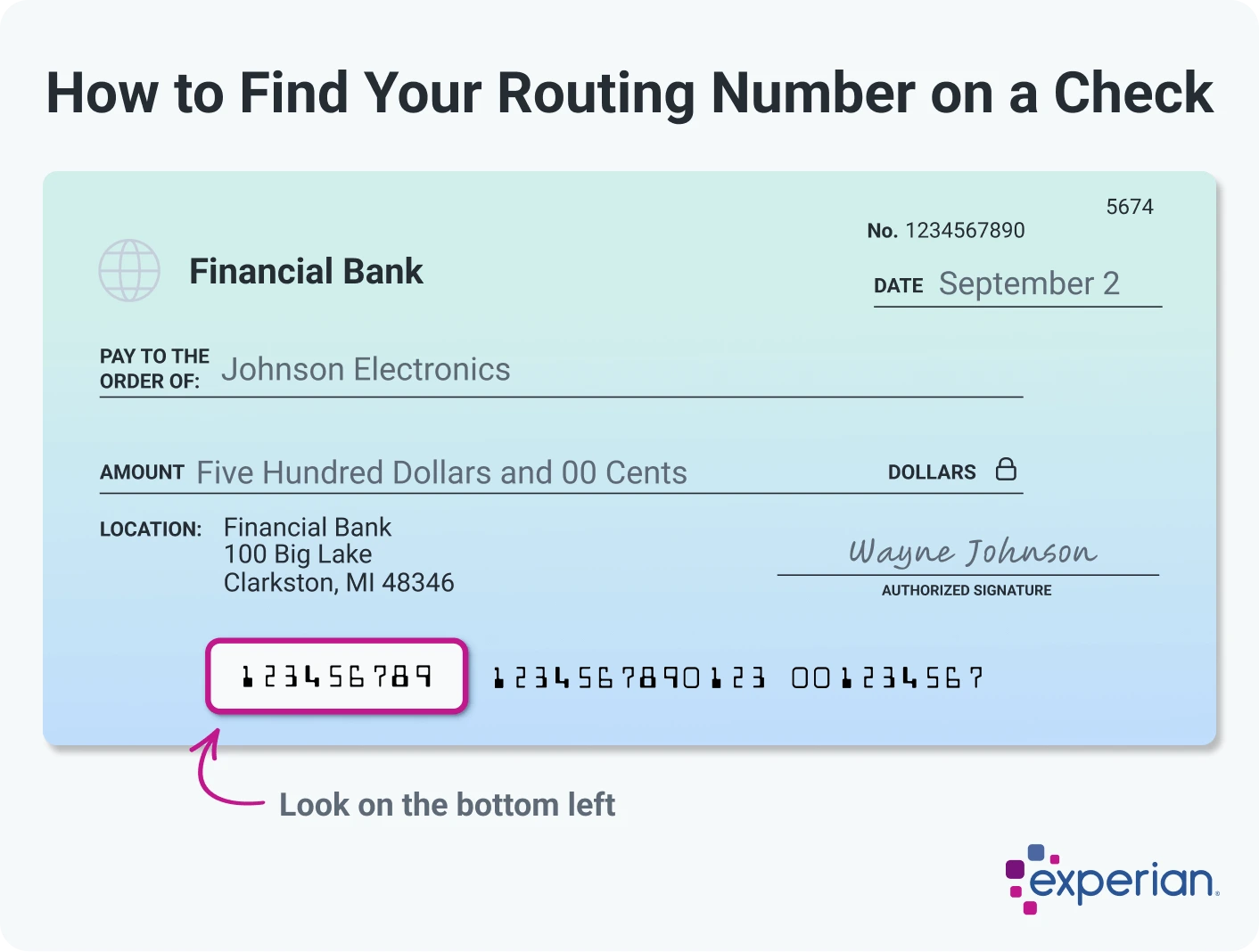

Reading Your Physical Checks

If you still use paper checks, the routing number is easiest to find there. Look at the bottom left-hand corner of the check. You will see three distinct sets of numbers printed in a unique font (known as MICR, or Magnetic Ink Character Recognition).

- The first sequence on the left, flanked by special symbols, is your nine-digit routing number.

- The middle sequence is typically your account number.

- The final, shortest sequence is the check number.

It is important to ensure you are reading a check and not a deposit slip. On many deposit slips, the routing number may be different or located in a different position, which can lead to rejected transactions if used for direct deposits.

Online Banking and Mobile Apps

For the digital-first user, your routing number is usually housed within your bank’s secure portal. Once logged into your dashboard:

- Navigate to the “Account Details” or “Account Summary” tab.

- Look for a link labeled “Show Routing Number” or “Electronic Transfers.”

- Be aware that some banks provide two different routing numbers: one for “ACH” (used for direct deposits and bill pay) and one for “Domestic Wire Transfers.” Using the wire routing number for a standard paycheck deposit can cause the transaction to fail.

Direct Deposit Forms and Bank Statements

If you do not have access to your online login, your monthly bank statement (either physical or PDF) almost always lists the routing number alongside your account balance. Additionally, most banks offer a pre-filled “Direct Deposit Authorization Form” on their website which contains the routing number, account number, and bank address in a format specifically designed for HR departments.

The Critical Role of Routing Numbers in Financial Transactions

The routing number is the “engine” behind almost every movement of money in the U.S. economy. Understanding the specific contexts in which it is used can help you optimize your personal cash flow and avoid costly delays.

Setting Up Direct Deposits and Automatic Payments

The most common use for a routing number is the establishment of a “push/pull” relationship between your bank and an external entity. When you provide your routing number to your employer, you are enabling a “push” transaction (Direct Deposit). When you provide it to a utility company or a credit card issuer, you are often enabling a “pull” transaction (Auto-Pay). Because these transactions are processed through the ACH network, they are highly secure but require 100% accuracy in the routing digits to prevent funds from being “lost” in the banking system for several business days while the error is rectified.

Wire Transfers vs. ACH Transfers

While they may seem similar, Wire Transfers and ACH transfers are different financial products.

- ACH Transfers are typically free or low-cost and are processed in batches (taking 1–3 days). They use the standard routing number.

- Wire Transfers are immediate and usually come with a fee (ranging from $15 to $50). Many banks require a separate routing number for wires. If you are closing on a house or sending a large sum of money, always confirm with your bank if they have a dedicated “Wire Routing Number” to ensure the funds arrive on time.

Navigating Domestic vs. International Transfers (SWIFT/BIC)

The nine-digit routing number is a uniquely American standard. If you need to receive money from an individual or business outside of the United States, a routing number alone will not suffice. You will need a SWIFT code (also known as a BIC or Business Identifier Code). The SWIFT code is an 8 to 11-character alphanumeric code that identifies your bank globally. While your domestic routing number is used once the money reaches the U.S. border, the SWIFT code is what gets it across the ocean.

Security and Strategy: Protecting Your Financial Identity

Because the routing number is a public identifier of a bank, many people wonder if it is “secret” information. The answer is nuanced. While your routing number isn’t a secret—anyone who has ever seen one of your checks knows it—it is a vital component of your financial identity that must be guarded.

Is a Routing Number Sensitive Information?

By itself, a routing number is not particularly dangerous; after all, it is the same for every customer at your branch. However, when combined with your account number, it becomes a powerful tool. With both numbers, an unauthorized individual could theoretically print “demand drafts” (fake checks) or initiate unauthorized ACH withdrawals from your account. Therefore, you should only provide your routing and account numbers to trusted, verified entities.

Preventing Fraud in Digital Transactions

In the age of fintech, many apps (like Venmo, PayPal, or Robinhood) ask you to link your bank account using your routing and account numbers. To stay safe:

- Use “Instant Verification” tools like Plaid when possible, which allow you to link accounts via your bank login rather than typing in your numbers manually.

- Monitor your account daily for small “micro-deposits.” These are often used by hackers to verify that an account is active before attempting a larger theft.

- Never send your routing and account numbers via unencrypted email or text message.

What to Do If Your Bank Merges or Changes

The banking industry is in a constant state of consolidation. If your bank is acquired by another institution, your routing number will likely change. Generally, banks will allow a “grace period” of 6 to 12 months where the old routing number will still work, automatically redirecting funds to the new system. However, it is your responsibility as a savvy financial manager to update your direct deposits and automated bill payments as soon as the new routing number is issued. Failing to do so can result in “Returned Item” fees or missed payments once the old number is officially retired.

Conclusion

The routing number may appear to be a relic of a bygone era of paper banking, but it remains the indispensable DNA of the American financial system. By understanding how to decode its structure, locate it across various platforms, and apply it correctly to different types of transfers, you gain greater control over your personal wealth.

In a world where financial speed and accuracy are paramount, knowing your routing number is more than just a clerical necessity—it is an essential skill for navigating the complexities of modern money management. Whether you are building a business, saving for retirement, or simply managing daily expenses, the routing number is the key that unlocks the seamless movement of your hard-earned capital.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.