For millions of graduates, student loan debt is the most significant financial hurdle of early-to-mid adulthood. While these loans represent an investment in human capital, the resulting monthly obligations can stifle other financial goals, such as purchasing a home, investing in the stock market, or building an emergency fund. Navigating the complexities of repayment requires more than just making minimum payments; it demands a sophisticated understanding of interest mechanics, federal protections, and strategic capital allocation.

To successfully retire student debt, one must treat it as a core component of a broader personal finance strategy. This guide explores the multifaceted landscape of student loan repayment, providing a roadmap for borrowers to minimize interest costs and accelerate their path to financial freedom.

Understanding Your Loan Portfolio: The Foundation of Repayment

Before implementing a repayment strategy, a borrower must conduct a comprehensive audit of their debt. Not all student loans are created equal, and the rules governing them vary significantly based on their origin and terms.

Federal vs. Private Loans: Knowing the Difference

The most critical distinction in your portfolio is between federal and private loans. Federal loans, funded by the government, offer unique protections such as income-driven repayment (IDR) plans, deferment, forbearance, and various forgiveness programs. These loans generally have fixed interest rates set by federal law.

Private loans, conversely, are issued by banks, credit unions, or online lenders. They lack the safety nets of federal debt and often feature variable interest rates that fluctuate with market conditions. Because private lenders are profit-driven, their terms are less flexible. Identifying which loans fall into which category determines your eligibility for specific relief programs and informs whether you should prioritize one over the other.

Analyzing Interest Rates and Capitalization

Interest is the “cost of waiting.” To minimize this cost, you must understand how your interest accrues and when it capitalizes. Interest capitalization occurs when unpaid interest is added to the principal balance, increasing the amount upon which future interest is calculated. This often happens after a grace period, a period of deferment, or when leaving certain repayment plans. By making interest-only payments during school or grace periods, borrowers can prevent capitalization and significantly reduce the total cost of the loan over its lifetime.

Federal Repayment Plans: Matching Payments to Income

The U.S. Department of Education offers several repayment structures designed to prevent the debt from becoming a hardship. Choosing the right plan is a balance between monthly cash flow and total interest paid.

Income-Driven Repayment (IDR) Plans

For many federal borrowers, IDR plans—such as the SAVE (Saving on a Valuable Education) plan, PAYE, and IBR—are the most powerful tools available. These plans cap monthly payments at a percentage of the borrower’s discretionary income, often 5% to 10%.

The primary advantage of IDR plans is that they ensure payments remain affordable regardless of career fluctuations. Furthermore, after 20 or 25 years of qualifying payments, any remaining balance is forgiven. The SAVE plan, in particular, is a game-changer because it prevents interest from accruing beyond the monthly payment amount, ensuring that the balance does not grow as long as the borrower meets their calculated obligation.

The Standard and Graduated Repayment Options

The Standard Repayment Plan is the default option, featuring fixed payments over 10 years. While this results in the highest monthly payments, it is often the cheapest route in terms of total interest paid because the debt is retired quickly.

The Graduated Repayment Plan starts with lower payments that increase every two years. This is designed for borrowers who expect their income to rise steadily. However, borrowers should be cautious: by paying less in the early years, you may end up paying significantly more in interest over the life of the loan.

Acceleration Strategies: Reducing Principal and Saving on Interest

For those with the financial capacity to pay more than the minimum, several strategies can shave years off a repayment timeline and save thousands of dollars in interest.

The Debt Avalanche vs. Debt Snowball Method

In the realm of personal finance, two primary philosophies dominate debt acceleration: the Debt Avalanche and the Debt Snowball.

The Debt Avalanche is the mathematically superior method. Under this strategy, the borrower makes minimum payments on all loans but directs every extra dollar toward the loan with the highest interest rate. By attacking the most expensive debt first, you minimize the total interest paid over time.

The Debt Snowball method focuses on psychological wins. Here, the borrower pays off the smallest balances first to build momentum. While this may feel rewarding, it is often more expensive in the long run if the larger balances carry higher interest rates. For most disciplined borrowers, the Avalanche method is the recommended financial choice.

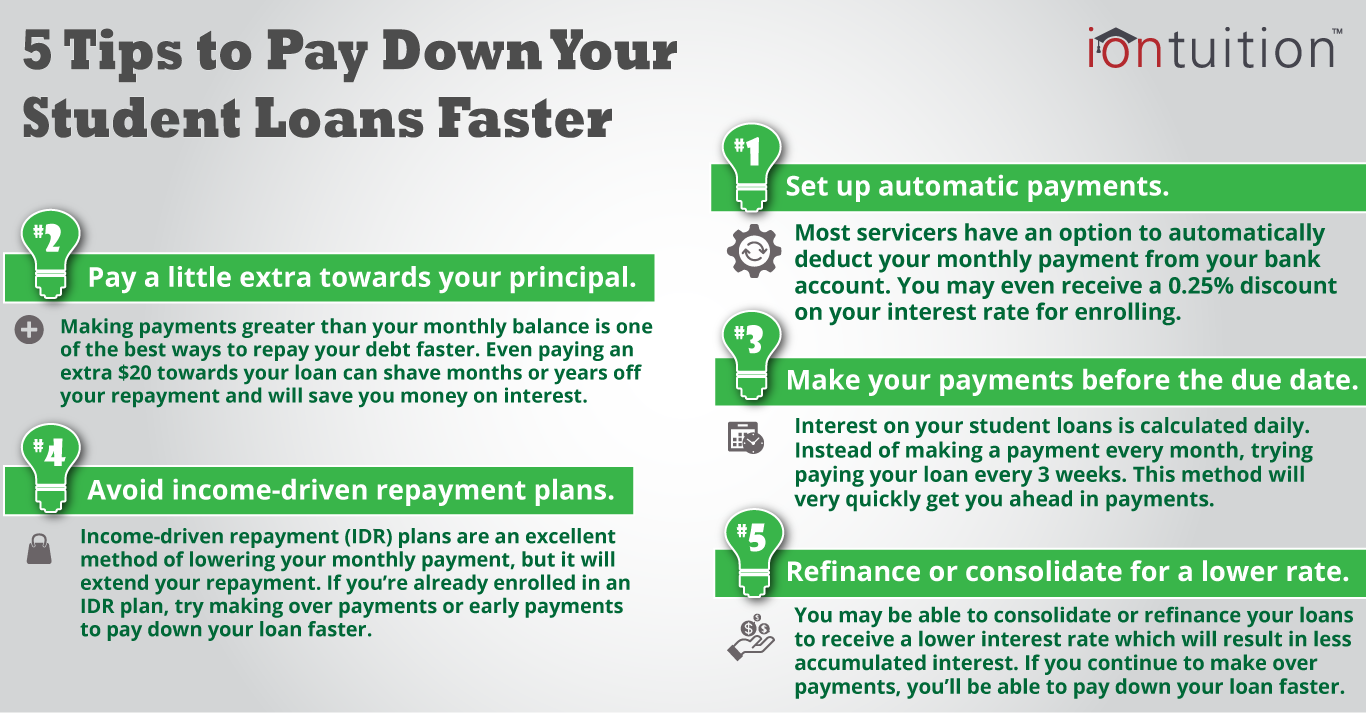

Automating Payments and Bi-Weekly Schedules

Most federal and private loan servicers offer a 0.25% interest rate deduction for enrolling in auto-pay. While a quarter of a percent may seem negligible, on a large balance over a decade, it results in substantial savings.

Additionally, consider a bi-weekly payment schedule. By paying half of your monthly obligation every two weeks, you effectively make 13 full payments a year instead of 12. This extra payment goes directly toward the principal, compounding the interest savings over time without significantly impacting your monthly budget.

Forgiveness, Discharge, and Employer Assistance

Not all debt must be paid back in full by the borrower. Several programs exist to reward public service or leverage corporate benefits.

Public Service Loan Forgiveness (PSLF)

PSLF is perhaps the most significant benefit for federal loan holders. It allows employees of government organizations and 501(c)(3) non-profits to have their remaining balance forgiven tax-free after making 120 qualifying monthly payments under an IDR plan. To maximize this benefit, borrowers should ensure their employment is certified annually and that they are not overpaying, as the goal is to have the largest possible balance forgiven at the end of the 10-year period.

Leveraging Employer-Sponsored Student Loan Benefits

The “Money” landscape is shifting, with more corporations offering student loan assistance as a recruitment and retention tool. Under current tax laws (specifically provisions expanded by the SECURE 2.0 Act), employers can contribute up to $5,250 annually toward an employee’s student loans tax-free. Furthermore, some employers now offer 401(k) matching contributions based on an employee’s student loan payments, allowing borrowers to pay down debt without sacrificing their retirement savings.

Refinancing and Consolidation: When Does It Make Sense?

As you progress in your career and your credit score improves, you may find opportunities to alter the structure of your debt through consolidation or refinancing.

The Pros and Cons of Private Refinancing

Refinancing involves taking out a new loan with a private lender to pay off existing student loans, ideally at a lower interest rate. This is most effective for borrowers with high-interest private loans or federal borrowers with high incomes and stable jobs who do not need federal protections.

However, refinancing federal loans into private loans is a one-way street. Once you refinance, you permanently lose access to IDR plans, PSLF, and federal discharge options. Therefore, this should only be done if the interest rate reduction is significant and you have a robust emergency fund to cover payments in case of job loss.

Timing the Market: Interest Rates and Credit Scores

To secure the best refinancing rates, borrowers must optimize their financial profile. Lenders look at the debt-to-income (DTI) ratio and credit score. Before applying for a refinance, ensure your credit report is accurate and that you have reduced other revolving debts, such as credit card balances. Timing is also key; in a high-interest-rate environment, it may be better to stay with federal loans and wait for market rates to drop before locking in a private fixed-rate loan.

Conclusion: The Long-Term Wealth Perspective

Repaying student loans is not a sprint; it is a marathon that requires consistent discipline and periodic reassessment. The “best” way to repay your debt depends entirely on your specific financial ecosystem—your income, your career trajectory, and your other investment goals.

By understanding the mechanics of your loans, choosing the most efficient repayment plan, and staying informed about legislative changes and employer benefits, you can transform a daunting debt burden into a manageable part of your financial journey. The ultimate goal is not just to reach a zero balance, but to do so in a way that preserves your ability to build long-term wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.