Discovering that you owe the Internal Revenue Service (IRS) can be a source of significant psychological and financial stress. Whether it results from an honest mistake on a return, an unexpected capital gain, or a shortfall in self-employment tax withholding, the “tax bill” is a hurdle that requires a strategic approach. In the realm of personal finance, managing tax debt is just as critical as managing a mortgage or an investment portfolio.

The IRS is often cited as the world’s most powerful creditor, equipped with tools that private lenders do not possess. However, the agency also offers a variety of structured pathways for taxpayers to settle their obligations. This guide explores the logistical, legal, and financial frameworks of repaying the IRS, ensuring you can settle your accounts while maintaining your financial health.

Understanding Your IRS Debt and Taking the First Steps

Before you can formulate a repayment strategy, you must clearly understand the nature of your liability. The IRS typically initiates communication via a series of notices, the most common being the Notice CP14. This document outlines exactly how much you owe, including any initial penalties and interest.

Deciphering the IRS Notice and Verifying Accuracy

The moment you receive a notice, the clock begins to tick. Your first step should not be panic, but verification. IRS records are not infallible. You should compare the notice against your original tax filing and your personal records (W-2s, 1099s, and receipts). Ensure that all payments you previously made were credited and that the IRS hasn’t overlooked any deductions or credits you were eligible for. If there is a discrepancy, you have the right to dispute the amount before entering into a repayment agreement.

The Cost of Procrastination: Penalties and Interest

In the world of money management, procrastination is expensive. The IRS charges a “Failure to Pay” penalty, which is generally 0.5% of the unpaid taxes for each month or part of a month the tax remains unpaid, up to a maximum of 25%. Additionally, the IRS charges underpayment interest that adjusts quarterly. Because these rates are often higher than what you might earn in a high-yield savings account, the financial incentive to pay quickly is immense. Understanding that interest compounds daily is a vital realization for any taxpayer looking to minimize their total loss.

Prioritizing Tax Debt in Your Financial Hierarchy

Not all debt is created equal. While a student loan might have a low fixed rate, IRS debt carries the threat of federal tax liens and levies on wages or bank accounts. Within your personal finance hierarchy, IRS debt should generally take precedence over low-interest consumer debt. Ignoring the IRS can lead to a damaged credit profile and the seizure of assets, which can take years to recover from.

Immediate and Short-Term Payment Options

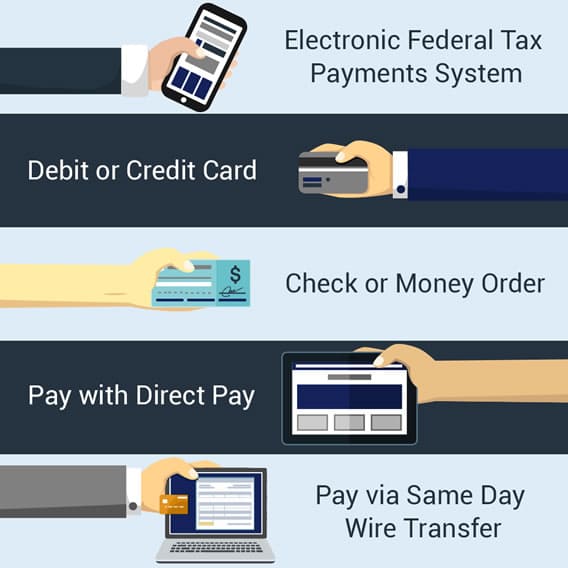

If you have the liquidity to pay your debt in full or over a very short period, you should do so to minimize interest. The IRS has modernized its systems, providing several digital gateways to facilitate rapid payments.

Leveraging IRS Direct Pay and EFTPS

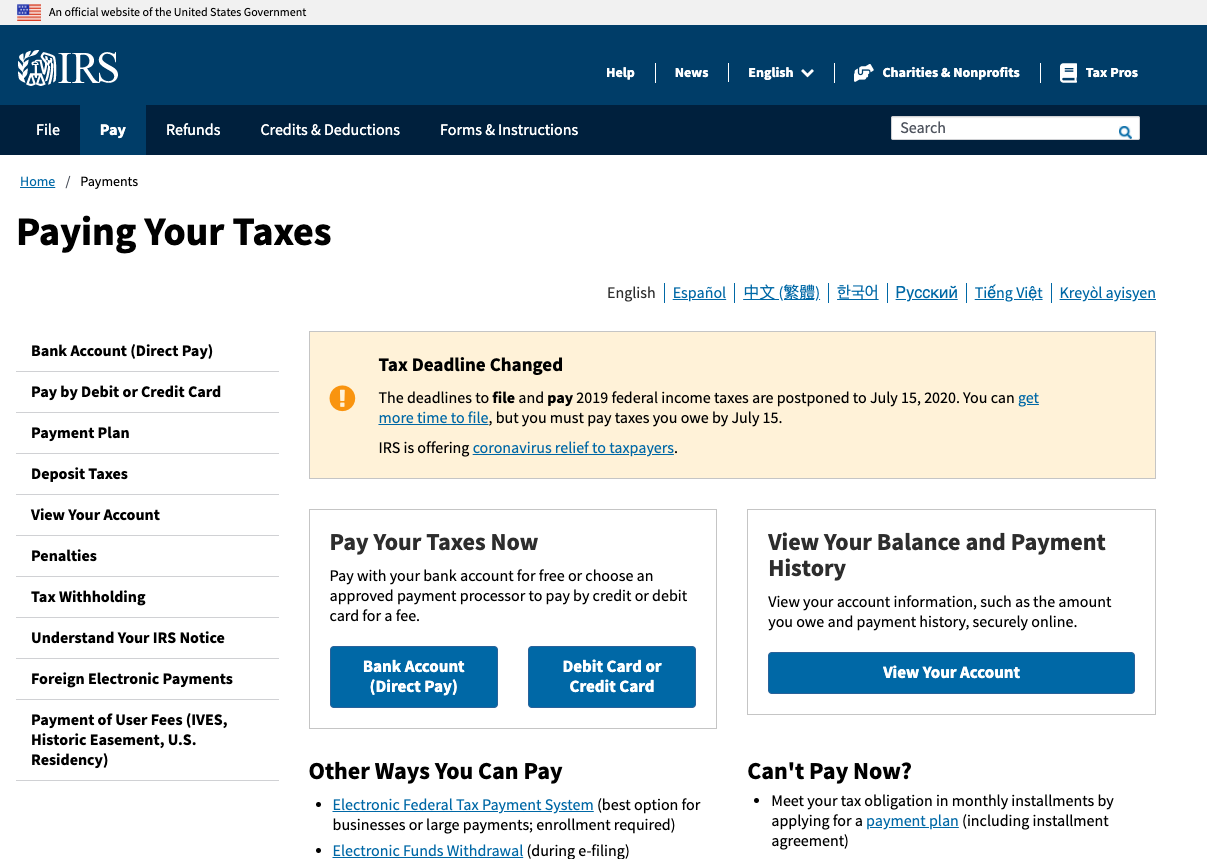

For individual taxpayers, IRS Direct Pay is the most efficient tool. It allows you to pay directly from your checking or savings account without any processing fees. It provides instant confirmation, which is crucial for record-keeping. For business owners or those with recurring large liabilities, the Electronic Federal Tax Payment System (EFTPS) is a more robust alternative. While it requires a separate registration process, it allows for scheduled payments and provides a comprehensive history of federal tax deposits.

The Pros and Cons of Credit and Debit Card Payments

While the IRS does not charge a fee for credit card payments, the third-party processors they use do. These fees typically range from 1.8% to 2% of the payment amount. From a financial strategy perspective, paying with a credit card only makes sense if:

- You are chasing a significant “sign-up bonus” on a new card that outweighs the processing fee.

- Your credit card’s interest rate is lower than the IRS penalty and interest rate (which is rare).

- You intend to pay off the credit card balance immediately to avoid high-interest revolving debt.

Short-Term Payment Plans (The 180-Day Rule)

If you cannot pay today but can pay within six months, the IRS offers a short-term payment plan. This is an informal agreement where you are granted up to 180 days to pay the liability in full. The primary advantage of this route is that there is typically no setup fee, unlike long-term installment agreements. However, interest and the late-payment penalty still accrue during this window, so paying as much as possible as early as possible remains the best strategy.

Long-Term Solutions for Significant Tax Liabilities

When the debt is too large to handle in six months, you must look toward structured, long-term options. These pathways are designed to help taxpayers satisfy their obligations over several years without facing aggressive collection actions like wage garnishments.

Installment Agreements: The 72-Month Framework

The most common solution is the Long-Term Payment Plan (Installment Agreement). For individual debts under $50,000, you can usually apply online for a “Streamlined Installment Agreement.” This allows you to pay off the debt over a period of up to 72 months.

- Financial Insight: While this makes the monthly payment manageable, it is important to calculate the total cost over six years. You may find that taking out a personal bank loan with a fixed interest rate is cheaper than the combined IRS penalty and interest rates.

Offer in Compromise (OIC): The “Settlement” Option

The Offer in Compromise is perhaps the most misunderstood tool in tax finance. Often advertised by “tax relief” companies as a way to pay “pennies on the dollar,” it is actually a very stringent program. To qualify, you must prove that you cannot possibly pay the full amount before the statute of limitations on collection expires. The IRS examines your “Reasonable Collection Potential,” looking at your assets, future income, and necessary living expenses. If you have significant equity in a home or a healthy 401(k), the IRS is unlikely to accept an OIC.

Currently Not Collectible (CNC) Status

If your financial situation is dire—meaning that paying even a small amount toward your tax debt would prevent you from meeting basic living expenses (rent, food, utilities)—you can request “Currently Not Collectible” status. While this stops active collection efforts like levies, it does not erase the debt. Interest continues to accrue, and the IRS will review your income annually to see if your financial situation has improved.

Navigating Hardship and Professional Assistance

Repaying the IRS is not just a mathematical exercise; it is a procedural one. Knowing when to handle it yourself and when to call in experts is a hallmark of sound financial management.

The Role of the Taxpayer Advocate Service (TAS)

The TAS is an independent organization within the IRS that acts as a voice for the taxpayer. If you are experiencing economic harm, such as being unable to pay for medical care because of a tax levy, the TAS can intervene. This is a free resource that every taxpayer should be aware of. They help ensure that your rights are protected and that the IRS follows its own internal procedures.

Knowing When to Hire a CPA or Tax Attorney

If your debt exceeds $25,000 or involves complex issues like payroll tax or international income, professional representation is vital. A Certified Public Accountant (CPA) or an Enrolled Agent (EA) can represent you before the IRS, often negotiating better terms than an individual could on their own. For matters involving potential criminal charges or extreme legal disputes, a Tax Attorney is necessary. The fees for these professionals should be viewed as an investment in mitigating long-term financial damage.

Avoiding “Tax Relief” Scams

The “Money” niche is unfortunately rife with predatory services. Many firms promise to “wipe out” your tax debt for a large upfront fee. A red flag is any company that guarantees an Offer in Compromise before even seeing your financial documents. Always check the credentials of a firm and look for reviews from the Better Business Bureau. Authentic tax help focuses on compliance and structured repayment, not “magic” erasers.

Future-Proofing Your Finances to Avoid IRS Debt

The ultimate goal of any repayment strategy is to ensure that you never find yourself in this position again. Financial health requires a proactive stance on tax liability throughout the year, not just in April.

Adjusting Withholdings and Estimated Payments

If you are an employee, use the IRS Withholding Estimator to ensure your employer is taking out the correct amount. If you are a freelancer or business owner, you must master the art of Estimated Tax Payments. Paying quarterly (in April, June, September, and January) prevents the “tax shock” that occurs when you realize you owe thousands of dollars at year-end. Setting aside 25-30% of every paycheck into a dedicated “Tax Savings” account is a best practice for any modern worker.

Record Keeping and Tax Planning Software

In the digital age, there is no excuse for poor record-keeping. Utilize software that integrates with your bank accounts to track deductible expenses in real-time. By the time tax season arrives, your documentation should be complete. This reduces the likelihood of errors that lead to audits and subsequent debt. High-quality financial software can also project your year-end liability, allowing you to make “catch-up” payments if you’ve had a particularly profitable year.

The Psychology of Financial Compliance

Finally, treat taxes as a fixed business expense rather than a variable “leftover.” When you view the money you owe the government as “never yours to begin with,” the emotional burden of repayment diminishes. Successful wealth building is built on a foundation of compliance. By mastering the art of IRS repayment and future prevention, you secure your financial legacy and ensure that your hard-earned assets remain protected from the reach of the tax collector.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.