Reducing your tax burden is a critical component of sound financial planning, allowing you to retain more of your hard-earned money and accelerate your financial goals. While tax codes can appear complex, understanding and strategically applying various deductions, credits, and investment vehicles can significantly lower your annual tax liability. This comprehensive guide explores actionable strategies to help individuals and businesses minimize their taxes legally and effectively.

Foundational Strategies for Tax Efficiency

Effective tax reduction begins with understanding basic principles and establishing disciplined habits. A proactive approach is key to identifying and leveraging every available opportunity.

Maximize Pre-Tax Retirement Contributions

One of the most powerful and accessible methods to reduce your taxable income is contributing to pre-tax retirement accounts. Contributions to traditional 401(k)s, 403(b)s, and traditional IRAs are made with pre-tax dollars, meaning the amount you contribute is subtracted from your gross income before taxes are calculated. This directly reduces your current year’s taxable income, potentially moving you into a lower tax bracket.

For example, if you earn $70,000 annually and contribute $10,000 to your traditional 401(k), your taxable income for the year drops to $60,000. Not only do these contributions lower your immediate tax bill, but your investments also grow tax-deferred until retirement, offering substantial long-term benefits. Understanding your employer’s matching contributions is also crucial, as failing to contribute enough to earn the full match is akin to leaving free money on the table, money that also grows tax-deferred.

Understand Tax Deductions vs. Tax Credits

Distinguishing between tax deductions and tax credits is fundamental to effective tax planning, as their impact on your tax liability differs significantly.

- Tax Deductions reduce your taxable income. They lower the amount of income on which you are taxed. For instance, a $1,000 deduction for someone in a 24% tax bracket would save them $240 ($1,000 * 0.24) in taxes. The benefit of a deduction depends on your marginal tax rate.

- Tax Credits, on the other hand, directly reduce the amount of tax you owe, dollar for dollar. A $1,000 tax credit means your tax bill is reduced by $1,000, regardless of your tax bracket. Credits are generally more valuable than deductions. Some credits are even refundable, meaning if the credit reduces your tax liability below zero, the government will send you a refund for the difference. Examples include the Child Tax Credit or the Earned Income Tax Credit. Knowing which deductions and credits you qualify for is the first step toward significant savings.

Keep Meticulous Records

The cornerstone of successful tax reduction and audit defense is thorough record-keeping. Whether it’s receipts for business expenses, donation records, medical bills, or investment statements, maintaining detailed and organized records is essential. Digital record-keeping, such as scanning receipts and storing them in cloud-based folders, can simplify this process and ensure accessibility. Without proper documentation, you may be unable to claim legitimate deductions or credits, potentially costing you hundreds or thousands of dollars. Good records also save time and stress come tax season.

Optimizing Personal Tax Savings

Beyond foundational strategies, individuals have numerous specific opportunities to reduce their tax burden by leveraging various deductions and credits tailored to personal circumstances.

Itemize When Advantageous

When filing your taxes, you have the choice between taking the standard deduction or itemizing your deductions. The standard deduction is a fixed dollar amount that reduces your taxable income, and it varies based on your filing status. Itemizing involves listing out specific deductible expenses. You should itemize if the total of your eligible itemized deductions exceeds the standard deduction amount for your filing status. Common itemized deductions include:

- State and Local Taxes (SALT): This includes property taxes and either income or sales taxes, capped at $10,000 per household.

- Mortgage Interest: Interest paid on home mortgage loans can be deductible, subject to certain limits.

- Medical Expenses: You can deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI).

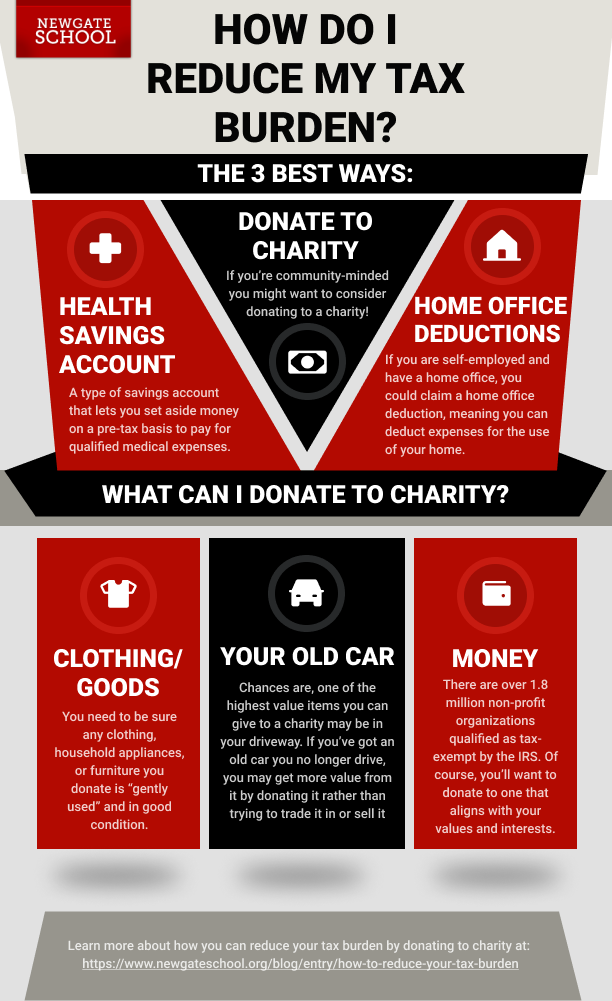

- Charitable Contributions: Cash and non-cash donations to qualified charities are deductible, subject to AGI limits.

Regularly assessing whether itemizing is more beneficial can lead to significant savings.

Utilize Health Savings Accounts (HSAs)

For individuals enrolled in a high-deductible health plan (HDHP), an HSA offers a unique “triple tax advantage”:

- Tax-deductible contributions: Contributions reduce your taxable income.

- Tax-free growth: Investments within the HSA grow free from federal income tax.

- Tax-free withdrawals: Qualified medical expenses can be paid for with tax-free withdrawals at any time.

HSAs are often referred to as “super IRAs” due to their unparalleled tax benefits, especially if contributions are invested and allowed to grow over time, to be used for medical expenses in retirement.

Education-Related Tax Benefits

The government offers several tax benefits to help offset the cost of higher education:

- American Opportunity Tax Credit (AOTC): A maximum credit of $2,500 per eligible student for the first four years of postsecondary education. Up to 40% of the credit may be refundable.

- Lifetime Learning Credit (LLC): A maximum credit of $2,000 per tax return for courses taken towards a degree or to acquire job skills.

- Student Loan Interest Deduction: You can deduct the amount of interest you paid during the year on a qualified student loan, up to a maximum of $2,500, subject to income limitations.

These credits and deductions can significantly reduce the financial burden of pursuing education.

Family-Related Credits

Families can benefit from several credits designed to support those with dependents:

- Child Tax Credit (CTC): Provides a credit of up to $2,000 per qualifying child, with a portion potentially refundable.

- Credit for Other Dependents: A non-refundable credit of up to $500 for dependents who don’t qualify for the CTC.

- Child and Dependent Care Credit: Helps offset the cost of care for a qualifying child or dependent so you can work or look for work.

Tax-Smart Investing and Asset Management

Strategic investment choices can profoundly impact your overall tax liability. By understanding how different investments are taxed, you can structure your portfolio for greater tax efficiency.

Capital Gains Management

When you sell an investment for a profit, you incur a capital gain, which is taxable. The tax rate depends on how long you held the asset:

- Short-term capital gains: For assets held one year or less, these are taxed at your ordinary income tax rates, which can be as high as 37%.

- Long-term capital gains: For assets held for more than one year, these are taxed at preferential rates (0%, 15%, or 20% for most taxpayers).

To minimize capital gains taxes, aim to hold investments for longer than a year. Additionally, tax-loss harvesting is a strategy where you sell investments at a loss to offset capital gains and potentially up to $3,000 of ordinary income in a given year. Any remaining losses can be carried forward to future years. Be mindful of the “wash-sale rule,” which prevents you from claiming a loss on a sale if you buy a substantially identical security within 30 days before or after the sale.

Tax-Advantaged Investment Accounts

Beyond traditional retirement accounts, other investment vehicles offer tax benefits:

- 529 Plans: Designed for education savings, contributions grow tax-free, and withdrawals are tax-free when used for qualified education expenses. Some states also offer state income tax deductions for contributions.

- Municipal Bonds: Interest earned on municipal bonds is generally exempt from federal income tax, and often from state and local taxes if you reside in the state where the bond was issued. This makes them attractive for high-income earners.

- Roth Accounts (IRA, 401(k)): While not offering an upfront tax deduction, Roth accounts provide tax-free withdrawals in retirement. This can be advantageous if you expect to be in a higher tax bracket in retirement than you are today.

Estate Planning for Future Tax Reduction

Strategic estate planning can help minimize taxes on inherited assets and ensure your wealth is distributed according to your wishes. Utilizing trusts, making annual tax-free gifts, and understanding estate tax exemptions can significantly reduce future tax burdens for your heirs. Consulting with an estate planning attorney is crucial to navigate these complex rules.

Business and Self-Employment Tax Advantages

For entrepreneurs, freelancers, and small business owners, numerous tax advantages are available to reduce the tax burden on business income.

Deductible Business Expenses

Virtually every legitimate expense incurred to operate your business can be deducted from your business income, reducing your overall tax liability. Common deductible business expenses include:

- Home Office Deduction: If you use a part of your home exclusively and regularly for business, you can deduct a portion of your rent/mortgage interest, utilities, insurance, and repairs.

- Business Travel and Meals: Expenses for business trips (transportation, lodging) and a portion of business meals (typically 50%).

- Equipment and Supplies: Purchases of office equipment, software, and supplies.

- Professional Development: Education, seminars, and subscriptions directly related to your business.

- Insurance Premiums: Health insurance (if self-employed), liability insurance, and other business-related coverage.

- Professional Services: Fees paid to accountants, lawyers, and consultants.

Keeping meticulous records of all business expenses is paramount for claiming these deductions.

Entity Selection

The legal structure of your business significantly impacts how it’s taxed.

- Sole Proprietorship/Partnership: Profits and losses are passed through to the owner’s personal tax return, subject to self-employment taxes (Social Security and Medicare).

- Limited Liability Company (LLC): Can be taxed as a sole proprietorship, partnership, S-Corp, or C-Corp.

- S-Corporation: Allows owners to pay themselves a reasonable salary and take the remaining profits as distributions, which are not subject to self-employment taxes. This can lead to substantial savings for profitable businesses.

- C-Corporation: The business is taxed separately from its owners, leading to potential “double taxation” (corporate profits are taxed, and then dividends paid to shareholders are taxed again at the individual level). However, C-corps offer other benefits like more comprehensive fringe benefits.

Choosing the right entity structure requires careful consideration of your business goals and revenue, often with the guidance of a tax professional.

Retirement Plans for the Self-Employed

Self-employed individuals have excellent options to save for retirement while also reducing their taxable income:

- SEP IRA (Simplified Employee Pension IRA): Allows employers (including self-employed individuals) to contribute a significant portion of their net self-employment earnings (up to 25% of compensation, with annual limits).

- SIMPLE IRA (Savings Incentive Match Plan for Employees IRA): Suitable for small businesses with up to 100 employees, including the self-employed. It involves elective deferrals and mandatory employer contributions.

- Solo 401(k): Offers both an employee deferral component and an employer profit-sharing component, allowing for potentially higher contributions than a SEP IRA, especially for those with no employees.

These plans provide substantial tax deductions while building a robust retirement nest egg.

Proactive Planning and Professional Guidance

Effective tax reduction is an ongoing process that benefits from foresight and expert advice, rather than a once-a-year scramble.

Year-End Tax Planning

Many tax-saving strategies are most effective when implemented before December 31st. This annual review offers an opportunity to:

- Accelerate Deductions: Pay next year’s January mortgage payment or property taxes in December. Make planned charitable contributions before the year ends.

- Defer Income: If possible, postpone receiving income until the next tax year, especially if you anticipate being in a lower tax bracket.

- Max Out Retirement Contributions: Ensure you’ve contributed the maximum allowable to your retirement accounts.

- Review Investment Portfolio: Consider tax-loss harvesting to offset gains.

Stay Informed on Tax Law Changes

Tax laws are dynamic and can change annually through new legislation. Staying informed about these changes is crucial for optimizing your tax strategy. Resources such as IRS publications, reputable financial news outlets, and tax professional updates can help you remain aware of new deductions, credits, or limitations that might affect your financial planning.

When to Consult a Tax Professional

While self-preparation tools are increasingly sophisticated, complex financial situations often warrant the expertise of a qualified tax professional (e.g., CPA, Enrolled Agent). This is especially true if you:

- Own a business or are self-employed.

- Have significant investment income or capital gains.

- Experienced major life changes (marriage, divorce, birth of a child, home purchase).

- Have international income or assets.

- Are facing an audit.

A professional can help you navigate intricate tax codes, identify overlooked deductions, ensure compliance, and develop a comprehensive tax plan tailored to your specific circumstances, often saving you more than their fees in the long run. Their insights can be invaluable in crafting a robust strategy for sustainable tax reduction.