Navigating the complexities of tax codes can often feel like deciphering an ancient language. For many individuals and businesses, taxes represent one of the largest annual expenses. However, with strategic planning, a deep understanding of available provisions, and consistent effort, it’s possible to significantly reduce your tax liability, freeing up more of your hard-earned money for savings, investments, or discretionary spending. This comprehensive guide will explore various legitimate strategies, from maximizing deductions and credits to leveraging tax-advantaged accounts and long-term financial planning, all aimed at helping you optimize your tax situation.

The goal isn’t to evade taxes, which is illegal, but to implement intelligent tax avoidance techniques that are entirely within the bounds of the law. This requires being proactive rather than reactive, making informed decisions throughout the year, and understanding how different financial actions impact your taxable income. By taking control of your tax planning, you empower yourself to retain more wealth and build a stronger financial future.

Maximizing Deductions and Credits

One of the most direct routes to reducing your tax burden is by taking full advantage of all eligible deductions and credits. These two mechanisms work differently but both serve to lower the amount of tax you owe. Deductions reduce your taxable income, while credits directly reduce the amount of tax you pay, dollar for dollar.

Understanding Standard vs. Itemized Deductions

When filing your taxes, you generally have a choice: take the standard deduction or itemize your deductions. The standard deduction is a fixed dollar amount set by the IRS, which varies based on your filing status (single, married filing jointly, head of household, etc.) and age/blindness. It simplifies the tax filing process for many.

Itemized deductions, on the other hand, allow you to list specific eligible expenses to reduce your taxable income. Common itemized deductions include state and local taxes (SALT) up to a certain limit, mortgage interest, medical expenses exceeding a certain percentage of your adjusted gross income (AGI), charitable contributions, and certain casualty and theft losses. To determine whether to itemize or take the standard deduction, you simply calculate the total of your eligible itemized deductions. If this total exceeds the standard deduction amount for your filing status, itemizing will result in a lower tax bill. Many taxpayers find that a significant mortgage or substantial charitable giving can push them past the standard deduction threshold. It’s crucial to keep meticulous records of all potential itemized expenses throughout the year to make an informed decision at tax time.

Leveraging Tax Credits

Tax credits are arguably more powerful than deductions because they directly subtract from your tax liability. A $1,000 deduction might save you $220 if you’re in the 22% tax bracket, but a $1,000 credit saves you the full $1,000. Credits can be non-refundable (meaning they can reduce your tax liability to zero, but you don’t get a refund for any leftover credit amount) or refundable (meaning if the credit amount exceeds your tax liability, you might get the difference back as a refund).

There’s a wide array of tax credits available, addressing various aspects of life. Some of the most common and impactful ones include:

- Child Tax Credit (CTC): A significant credit for eligible taxpayers with qualifying children.

- Education Credits: Such as the American Opportunity Tax Credit and the Lifetime Learning Credit, which help offset the costs of higher education.

- Earned Income Tax Credit (EITC): A refundable credit primarily for low to moderate-income working individuals and families.

- Child and Dependent Care Credit: For expenses incurred caring for a qualifying child or dependent while you work or look for work.

- Residential Energy Credits: For making energy-efficient improvements to your home.

- Retirement Savings Contributions Credit (Saver’s Credit): For eligible low- and moderate-income individuals contributing to retirement accounts.

It’s vital to research which credits you might qualify for, as they can significantly impact your tax bill. Eligibility requirements often involve income thresholds, so understanding these limits is key.

Strategic Use of Tax-Advantaged Accounts

Beyond immediate deductions and credits, strategic use of specific financial accounts designed with tax benefits can offer substantial long-term tax savings. These accounts generally fall into categories offering tax-deferred growth, tax-free withdrawals, or both.

Retirement Accounts

Retirement accounts are perhaps the most common and powerful tools for long-term tax reduction.

- Traditional 401(k) and IRA: Contributions to these accounts are typically tax-deductible in the year they are made, reducing your current taxable income. The money grows tax-deferred, meaning you don’t pay taxes on investment gains until you withdraw funds in retirement. This is particularly advantageous if you expect to be in a lower tax bracket in retirement than during your working years.

- Roth 401(k) and Roth IRA: Contributions to Roth accounts are made with after-tax dollars, meaning they are not deductible. However, the immense benefit is that qualified withdrawals in retirement are entirely tax-free. This is ideal if you anticipate being in a higher tax bracket in retirement or want to diversify your tax exposure in later years. The ability for investments to grow completely tax-free over decades can lead to substantial wealth accumulation.

- SEP IRA and Solo 401(k): For self-employed individuals and small business owners, these accounts offer higher contribution limits than traditional IRAs, allowing for more aggressive tax-deferred savings.

Maximizing contributions to these accounts not only builds your retirement nest egg but also immediately reduces your current year’s taxable income (for pre-tax accounts) or secures tax-free income in the future (for Roth accounts).

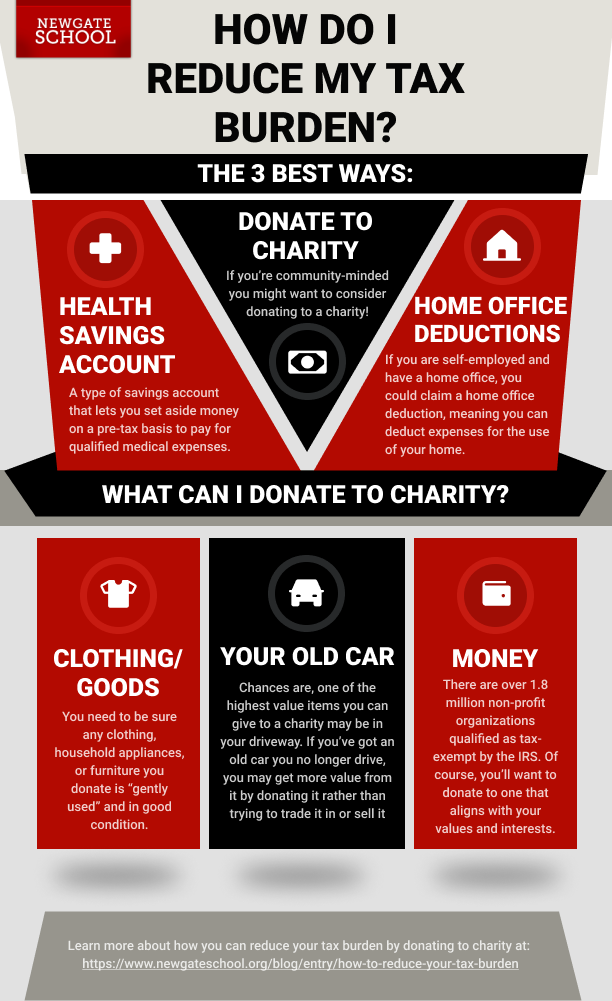

Health Savings Accounts (HSAs)

HSAs are often lauded as having a “triple tax advantage,” making them an incredibly powerful tool for those eligible. To contribute to an HSA, you must be covered by a High-Deductible Health Plan (HDHP).

- Tax-Deductible Contributions: Contributions are tax-deductible (or pre-tax if made through payroll deduction), reducing your taxable income.

- Tax-Free Growth: The money invested within the HSA grows tax-free.

- Tax-Free Withdrawals: Qualified withdrawals for medical expenses are entirely tax-free.

If you don’t use the funds for medical expenses, the money can be withdrawn for any purpose after age 65, subject to ordinary income tax (similar to a Traditional IRA), still benefiting from decades of tax-free growth. For those who are relatively healthy, an HSA can effectively function as a supplemental retirement account, with the added benefit of tax-free medical expense coverage.

529 College Savings Plans

While not directly reducing your federal income tax, 529 plans offer significant tax advantages for saving for education. Contributions grow tax-free, and withdrawals for qualified educational expenses (tuition, fees, books, room and board) are also federal tax-free. Many states also offer a state income tax deduction or credit for contributions to their 529 plans, providing an immediate tax benefit. By investing in a 529 plan, you ensure that the growth of your education savings isn’t eroded by annual taxes, allowing more money to compound over time for your children’s or your own future education costs.

Tax Planning for Businesses and Self-Employed Individuals

For entrepreneurs and small business owners, the opportunities for tax reduction are often more extensive and complex. Business operations naturally incur expenses that are deductible, and the choice of business structure itself can have profound tax implications.

Deducting Business Expenses

A fundamental aspect of business tax planning is understanding and meticulously tracking all ordinary and necessary business expenses. An “ordinary” expense is common and accepted in your industry, while a “necessary” expense is helpful and appropriate for your business. Examples include:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you can deduct a percentage of your housing costs (rent/mortgage interest, utilities, insurance, repairs).

- Travel and Meal Expenses: Business-related travel (flights, lodging) and a portion of business meals are deductible.

- Vehicle Expenses: Actual expenses (gas, oil, repairs, insurance, depreciation) or the standard mileage rate can be deducted for business use of your vehicle.

- Equipment and Supplies: Purchases of computers, software, office supplies, and tools are generally deductible.

- Professional Development: Education, seminars, and subscriptions directly related to maintaining or improving skills in your existing business can be deducted.

- Insurance Premiums: Health insurance premiums (if self-employed) and business liability insurance are deductible.

The key here is diligent record-keeping. Every receipt, invoice, and bank statement should be organized to substantiate your deductions in case of an IRS inquiry.

Choice of Business Structure

The legal structure of your business significantly impacts how you are taxed.

- Sole Proprietorship/Partnership: These are “pass-through” entities, meaning business income and losses are reported on the owner’s personal tax return (Schedule C for sole proprietorships). While simple to set up, owners are subject to self-employment taxes (Social Security and Medicare) on all business profits.

- Limited Liability Company (LLC): An LLC offers liability protection. For tax purposes, an LLC can elect to be taxed as a sole proprietorship, partnership, S-corporation, or C-corporation.

- S-Corporation: An S-Corp is also a pass-through entity, but it allows owners to be paid a “reasonable salary” and then take the remaining profits as distributions. Crucially, these distributions are generally not subject to self-employment taxes, which can lead to significant tax savings for profitable businesses. However, the IRS scrutinizes “reasonable salary” claims.

- C-Corporation: C-corps are taxed separately from their owners. They face “double taxation” – the corporation pays taxes on its profits, and then shareholders pay taxes again on dividends received. This structure is less common for small businesses focused on tax reduction, but it can be beneficial for businesses planning to retain earnings for growth or attract investors.

Consulting with a tax professional or business attorney before choosing a business structure is essential to align it with your tax reduction goals and operational needs.

Long-Term Tax Reduction Strategies

Effective tax reduction isn’t just about annual filing; it’s about incorporating tax awareness into your overall financial and estate planning, considering long-term implications.

Capital Gains Planning

Capital gains taxes apply to profits from selling assets like stocks, bonds, real estate, or other investments. The tax rate depends on how long you held the asset (short-term vs. long-term) and your income level.

- Long-Term vs. Short-Term: Assets held for more than one year are subject to lower long-term capital gains tax rates, which can be 0%, 15%, or 20% depending on your taxable income. Short-term capital gains are taxed at your ordinary income tax rates, which can be much higher. Holding onto investments for at least a year and a day before selling is a simple yet powerful strategy.

- Tax-Loss Harvesting: This strategy involves selling investments at a loss to offset capital gains and, if losses exceed gains, to deduct up to $3,000 against ordinary income annually. Any remaining losses can be carried forward indefinitely to offset future gains. This is a crucial year-end strategy for managing your investment portfolio efficiently.

- Qualified Charitable Distributions (QCDs): For individuals aged 70½ or older, a QCD allows you to directly transfer funds from your IRA to a qualified charity. These distributions count towards your Required Minimum Distributions (RMDs) but are excluded from your taxable income, a significant benefit for reducing your AGI.

Estate and Gift Tax Planning

While estate and gift taxes affect a smaller percentage of the population due to high exemption thresholds, proactive planning can minimize potential liabilities for wealthy individuals.

- Annual Gift Tax Exclusion: You can give a certain amount (e.g., $18,000 per recipient in 2024) to as many individuals as you wish each year without using up your lifetime gift tax exemption or incurring gift tax. This is a way to reduce the size of your taxable estate over time.

- Irrevocable Trusts: For larger estates, various types of irrevocable trusts can be established to transfer assets out of your taxable estate, provide for beneficiaries, and potentially reduce estate tax liability.

- Charitable Remainder Trusts/Lead Trusts: These complex trusts allow you to make a significant charitable contribution while also providing income for yourself or your heirs for a period, with various tax advantages.

These strategies often require the guidance of an estate planning attorney and a financial advisor due to their complexity and significant legal implications.

Charitable Giving Strategies

Beyond the direct deduction for charitable contributions, there are sophisticated ways to give that also offer tax benefits.

- Donating Appreciated Securities: Instead of cash, consider donating appreciated stocks or mutual funds held for more than a year to a qualified charity. You typically avoid paying capital gains tax on the appreciation, and you can deduct the fair market value of the securities (subject to AGI limits), potentially doubling your tax benefit compared to selling the stock and donating the cash.

- Donor-Advised Funds (DAFs): A DAF allows you to make an irrevocable charitable contribution of cash or appreciated assets to a public charity that sponsors the fund. You receive an immediate tax deduction for the full contribution, but then you can recommend grants to specific charities over time. This is excellent for separating the tax benefit from the actual disbursement of funds, especially if you have a high-income year.

The Importance of Professional Guidance and Timely Planning

While self-education is valuable, the complexity and dynamic nature of tax law mean that professional guidance is often indispensable for truly optimizing your tax situation.

When to Consult a Tax Professional

A qualified tax professional (such as a Certified Public Accountant – CPA, or an Enrolled Agent – EA) can provide personalized advice and ensure you don’t miss out on any eligible deductions or credits. You should consider consulting one if:

- Your financial situation changes significantly (marriage, divorce, new child, new job, retirement).

- You start a business or become self-employed.

- You buy or sell a home or other substantial assets.

- You have investments or complex financial portfolios.

- You receive an inheritance or significant gift.

- You want to implement advanced tax planning strategies like estate planning or complex charitable giving.

A good tax professional can not only help you file your taxes correctly but also provide proactive advice throughout the year to minimize your future tax burden.

Keeping Meticulous Records

The foundation of effective tax reduction and compliance is impeccable record-keeping. Without proper documentation, the IRS can disallow deductions or credits, leading to additional taxes, penalties, and interest.

- Organize everything: Keep all income statements (W-2s, 1099s), receipts for deductible expenses, bank statements, investment statements, and any other relevant financial documents organized.

- Digitalize: Consider scanning and storing documents digitally, backed up in multiple locations. Cloud storage services are excellent for this.

- Categorize: Use accounting software or spreadsheets to categorize income and expenses, especially for businesses.

- Retain for years: Keep tax returns and supporting documentation for at least three to seven years, or even longer for certain records like those related to asset purchases and sales.

Staying Informed About Tax Law Changes

Tax laws are not static. Congress frequently passes new legislation, and the IRS issues new regulations and guidance. What was deductible last year might not be this year, or new credits might become available. Subscribing to financial news outlets, following reputable tax blogs, and regularly consulting with your tax professional are all ways to stay abreast of changes that could impact your tax strategy. Proactive awareness allows you to adapt your financial planning and continue to optimize your tax position year after year.

Reducing your tax burden is an ongoing process that requires education, planning, and diligence. By understanding and strategically applying deductions, credits, tax-advantaged accounts, and long-term financial planning techniques, you can significantly enhance your financial well-being. It’s an investment of time that pays substantial dividends, allowing you to keep more of your money working for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.