In an era defined by rapid financial evolution, the question of “how to pay” has transcended the simple act of handing over physical currency. What was once a binary choice between cash and check has blossomed into a complex ecosystem of digital wallets, credit instruments, decentralized finance, and strategic debt management. How you choose to settle a transaction is no longer just a logistical necessity; it is a fundamental pillar of personal finance that dictates your creditworthiness, your exposure to fraud, and your long-term wealth accumulation.

Understanding the mechanics of modern payments requires a shift in perspective. Every time you “pay,” you are making a micro-decision about liquidity, opportunity cost, and financial security. This guide explores the strategic landscape of modern payments, offering a roadmap for navigating the various tools available to the contemporary consumer.

1. Choosing the Right Instrument: Credit, Debit, and Cash

The foundation of any payment strategy begins with the choice of medium. While the end result—the transfer of value—is the same, the financial implications of using a credit card versus a debit card or cash are vastly different.

The Power of Credit: Leverage and Rewards

For the financially disciplined, credit cards are perhaps the most powerful tool in the “how to pay” arsenal. Beyond the convenience of not carrying cash, credit cards offer a layer of consumer protection that is unmatched by other methods. Under regulations like the Fair Credit Billing Act, consumers are often protected against fraudulent charges and substandard goods.

Furthermore, the strategic use of credit cards allows for the accumulation of rewards—points, miles, or cashback—that effectively provide a discount on every purchase. When you pay with credit, you are essentially using the bank’s money for a short period. If the balance is paid in full every month, this “float” is interest-free, allowing your own capital to remain in high-yield savings accounts for longer.

Debit and Cash: The Psychology of Hard Limits

While credit offers leverage, debit and cash offer psychological friction. Behavioral economics suggests that the “pain of paying” is much higher when using physical cash or seeing an immediate deduction from a checking account. For those struggling with overspending, “how to pay” should prioritize these high-friction methods.

Debit cards provide the convenience of plastic without the risk of accumulating high-interest debt. They are direct links to your liquidity. Cash, meanwhile, remains the ultimate privacy tool and a foolproof way to adhere to a strict budget. If you only have $50 in your wallet, your spending is physically capped, eliminating the possibility of an impulsive, budget-busting purchase.

When to Use Which: A Decision Matrix

The savvy consumer uses a hybrid approach. High-value purchases and recurring bills are best handled via credit cards to maximize security and rewards. Daily incidental spending—like coffee or small groceries—might be better suited for debit or cash to maintain a realistic pulse on daily outflows. The goal is to align the payment method with the specific financial objective: protection, rewards, or discipline.

2. Navigating the Digital Frontier: Mobile Wallets and Modern Fintech

As technology matures, the “how” of payment has migrated into the digital realm. The rise of fintech has introduced layers of convenience that were unimaginable two decades ago, but these advancements come with new sets of rules for financial health.

The Rise of “Buy Now, Pay Later” (BNPL)

One of the most significant shifts in modern retail is the ubiquity of “Buy Now, Pay Later” services. These platforms allow consumers to split a purchase into interest-free installments. While this can be a useful tool for managing cash flow on essential large purchases, it carries a hidden danger: the “phantom debt” trap.

Because BNPL payments are often small and spread out, it is easy for a consumer to lose track of their total monthly obligations. From a money management perspective, BNPL should be treated with the same caution as a traditional loan. If not managed carefully, a series of $20 installments can quickly aggregate into a significant portion of one’s monthly income, squeezing the budget for essentials.

Mobile Wallets and Contactless Payments

Apple Pay, Google Pay, and Samsung Pay have revolutionized the point-of-sale experience. By using tokenization—a process that replaces sensitive card details with a unique digital identifier—these methods are actually more secure than swiping a physical card.

From a personal finance standpoint, mobile wallets facilitate better tracking. Most integrations offer real-time notifications and categorized spending reports. Integrating these tools into your financial routine allows for a more “hands-on” approach to monitoring where your money goes, despite the “contactless” nature of the transaction.

Security in the Digital Age: Protecting Your Assets

The ease of digital payments necessitates a heightened focus on digital hygiene. “How to pay” safely involves more than just picking a platform; it requires the use of two-factor authentication (2FA), unique passwords for financial institutions, and the avoidance of public Wi-Fi when conducting transactions. In the digital economy, your data is as valuable as your currency; protecting the former is the only way to ensure the safety of the latter.

3. Strategic Debt Management: How to Pay Off Obligations

Payment isn’t just about buying new things; it’s also about settling old ones. How you choose to pay down debt is perhaps the most critical factor in achieving financial freedom. Not all debts are created equal, and the strategy for repayment should reflect that.

The Snowball vs. Avalanche Methods

There are two primary schools of thought when it comes to paying off multiple debts. The “Debt Snowball” method focuses on psychological wins by paying off the smallest balances first. This creates momentum and a sense of accomplishment.

Conversely, the “Debt Avalanche” method is mathematically superior. It involves paying off debts with the highest interest rates first, regardless of the balance. This minimizes the total interest paid over time and shortens the path to being debt-free. Choosing between these methods depends on your personality: do you need the psychological boost of a closed account, or are you driven by the cold, hard logic of interest savings?

Consolidating High-Interest Debt

For those juggling multiple high-interest credit cards, “how to pay” might involve a debt consolidation loan or a balance transfer card. By moving high-interest debt to a lower-interest vehicle, more of your monthly payment goes toward the principal balance rather than interest. However, this is only a viable strategy if the underlying spending behavior has been corrected. Without a change in habits, consolidation can lead to a dangerous cycle of “double-dipping” into both the new loan and the newly cleared credit lines.

Negotiating with Creditors

Many consumers do not realize that the terms of their debt are often negotiable. If you are struggling to make payments, the most proactive “how to pay” strategy is to contact the creditor directly. Whether it’s a medical bill or a credit card balance, institutions are often willing to settle for a lump sum or move the debtor into a hardship program with lower interest rates. The key is to initiate the conversation before a default occurs.

4. Optimizing Recurring Payments and Subscriptions

In the modern “subscription economy,” a significant portion of our income is spoken for before the month even begins. Optimizing how we pay for recurring services is essential for maintaining a healthy savings rate.

The Subscription Trap: Audit and Automate

The convenience of “set it and forget it” payments is a double-edged sword. While it ensures bills are paid on time, it often leads to “subscription creep,” where consumers continue paying for services they no longer use. A quarterly audit of your bank and credit card statements is a mandatory practice for modern money management. Identify every recurring charge and ask: “Is the value I receive from this greater than the cost?” If the answer is no, cancel it immediately.

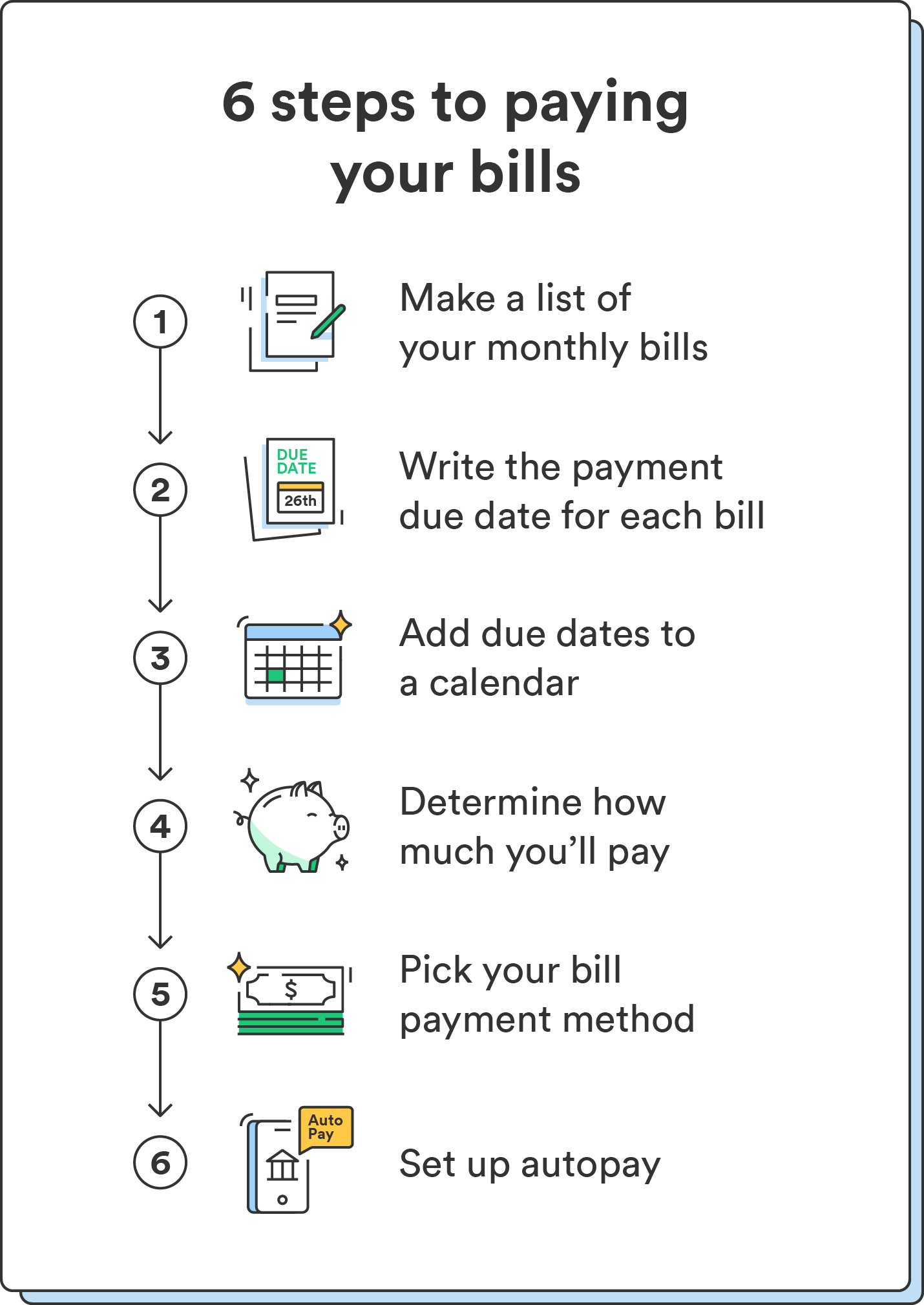

Effective Bill-Pay Strategies to Avoid Late Fees

Late fees and interest charges are the enemies of wealth. To optimize your payment schedule, align your bill due dates with your paycheck cycle. Most utility companies and credit card issuers allow you to change your billing cycle. By ensuring that your largest outflows occur shortly after your largest inflows, you minimize the risk of overdrafts and ensure that your obligations are met with the freshest capital.

Leveraging Corporate and Tax Incentives

Finally, consider “how to pay” in the context of your broader financial ecosystem. Are you paying for gym memberships that your health insurance would reimburse? Are you paying for professional development out of pocket when your employer has a tuition assistance program? Furthermore, using “pre-tax” payment methods, such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs), allows you to pay for healthcare and childcare expenses using untaxed dollars. This effectively gives you a 15% to 30% discount on these necessary costs, depending on your tax bracket.

Conclusion: The Philosophy of Intentional Payment

Ultimately, the question of “how to pay” is a question of intention. In a world designed to make spending as frictionless and invisible as possible, the most successful financial managers are those who reintroduce intentionality into their transactions.

Whether you are choosing a credit card for its travel rewards, using a “Debt Avalanche” to crush your student loans, or auditing your digital subscriptions to reclaim your cash flow, your payment methods should serve your larger financial goals. By treating every payment not as an isolated event but as a strategic move in a larger financial game, you move from being a passive consumer to an active architect of your own wealth. Money is a tool, and knowing exactly how to use it—and how to pay it out—is the hallmark of true financial literacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.