Navigating the complexities of federal tax payments can seem daunting, but understanding the process is a fundamental aspect of sound personal and business finance. Annually, millions of taxpayers fulfill their obligation to the Internal Revenue Service (IRS), contributing to the nation’s infrastructure and services. For individuals and businesses alike, timely and accurate tax payment is not just a legal requirement but a cornerstone of financial responsibility, preventing penalties and maintaining good standing with the tax authorities. This guide demystifies the process, outlining who needs to pay, when, and through various approved methods, alongside strategic financial tips to manage your tax burden effectively.

Understanding Your Federal Tax Obligations

Before you can pay your taxes, it’s crucial to understand what you owe and why. The U.S. tax system is a “pay-as-you-go” system, meaning taxes are paid throughout the year as income is earned, rather than in one lump sum at year-end. This is typically achieved through payroll withholding for employees or estimated tax payments for the self-employed and those with other income sources not subject to withholding.

Who Needs to File and Pay?

Not everyone is required to file a federal income tax return, but most individuals and businesses earning above a certain threshold must. The requirement to file generally depends on your gross income, filing status (single, married filing jointly, head of household, etc.), and age. For instance, if your gross income exceeds the standard deduction for your filing status, you likely need to file. Even if your income is below the filing threshold, you might choose to file to claim refundable tax credits or receive a refund of taxes withheld. Businesses, regardless of income, generally have specific filing and payment obligations.

Key Deadlines to Remember

Adhering to IRS deadlines is critical to avoid penalties. The most prominent deadline for individual income tax returns (Form 1040) is typically April 15th each year, though this can shift if April 15th falls on a weekend or holiday. If you can’t file on time, you can request an extension, which typically grants an additional six months to file, but not to pay. Any tax owed is still due by the original deadline.

For self-employed individuals, small business owners, and those with significant income not subject to withholding, estimated taxes must be paid quarterly. These payments are due on:

- April 15th (for January 1 to March 31 income)

- June 15th (for April 1 to May 31 income)

- September 15th (for June 1 to August 31 income)

- January 15th of the following year (for September 1 to December 31 income)

Corporate tax deadlines vary based on the fiscal year-end, often aligning with the 15th day of the fourth month after the close of the tax year.

Types of Taxes You Might Owe

The IRS collects various types of taxes. For most individuals, the primary concern is income tax, which is levied on wages, salaries, investment income, and other earnings.

Self-employment tax is another significant obligation for independent contractors, freelancers, and small business owners. This covers Social Security and Medicare taxes, which are automatically withheld from employees’ paychecks but must be paid directly by the self-employed.

If you anticipate owing at least $1,000 in tax for the year (or $500 for corporations), you’ll generally need to pay estimated taxes quarterly to avoid underpayment penalties. Other taxes can include excise taxes, estate taxes, and gift taxes, though these apply to a smaller segment of the taxpayer population.

Preparing for Seamless Tax Payment

Effective tax payment begins long before the deadline. Proper preparation ensures accuracy, reduces stress, and helps you identify potential savings or avoid costly errors.

Gathering Essential Documentation

The foundation of accurate tax preparation is meticulous record-keeping. You’ll need a variety of documents, including:

- Income Statements: W-2s from employers, 1099 forms (1099-NEC for non-employee compensation, 1099-INT for interest, 1099-DIV for dividends, 1099-B for stock sales, etc.), K-1s from partnerships or S-corporations.

- Records of Deductions and Credits: Receipts for qualified business expenses, medical expenses, charitable contributions, student loan interest statements (1098-E), mortgage interest statements (1098), property tax records, and childcare expenses.

- Bank and Investment Statements: To verify income and deductions, and track capital gains or losses.

- Previous Year’s Tax Return: A useful reference for prior-year adjustments, carryovers, and general filing information.

Organizing these documents throughout the year, rather than scrambling at tax time, can significantly streamline the process.

Calculating Your Tax Liability

Once you have all your documents, the next step is to calculate how much tax you owe. This can be done in several ways:

- Tax Software: Popular software like TurboTax, H&R Block, and TaxAct guide you through the process, performing calculations and identifying deductions and credits. Many offer free versions for simple returns.

- Professional Help: A Certified Public Accountant (CPA) or enrolled agent can prepare and file your taxes, offering expert advice on complex financial situations, business taxes, or tax planning strategies. While there’s a cost involved, their expertise can often lead to greater savings or ensure compliance.

- IRS Forms and Instructions: For those comfortable with detailed instructions, you can manually complete IRS forms like Form 1040. The IRS website provides all necessary forms and publications.

- IRS Free File Program: If your adjusted gross income (AGI) is below a certain threshold, you may qualify to use guided tax preparation software from IRS partners for free.

Regardless of the method, double-checking your calculations is crucial before submitting your payment.

Official IRS Payment Methods

The IRS offers several convenient and secure ways to pay your federal taxes. Choosing the right method depends on your preferences, the amount you’re paying, and the type of tax.

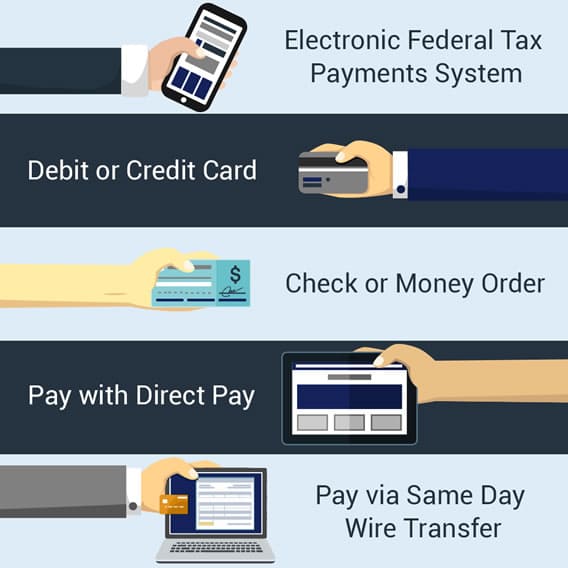

Direct Pay

IRS Direct Pay is a free, secure online service that allows you to pay directly from your checking or savings account. You can schedule payments up to 365 days in advance and receive immediate confirmation. This method is available for Forms 1040, 1040-ES (estimated taxes), and various business tax forms. It’s highly recommended for its ease of use and security.

Credit, Debit Card, or Digital Wallet

You can pay your taxes using a credit card, debit card, or digital wallet (e.g., PayPal, PayIt). This option is processed by third-party payment processors who charge a small fee, typically a percentage for credit cards and a flat fee for debit cards. While convenient, especially for those seeking rewards points or needing to defer payment for a short period, consider the processing fees compared to the benefits.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is a free service provided by the U.S. Department of the Treasury. It’s particularly useful for businesses, fiduciaries, tax professionals, and individuals who make estimated tax payments. You must enroll in EFTPS before you can use it, which involves a brief registration process where you receive a PIN. Payments can be scheduled up to 365 days in advance, and you receive an immediate confirmation number. It’s a robust system for managing regular tax payments.

For those who prefer traditional methods, you can pay by check or money order. Make your check or money order payable to the “U.S. Treasury.” Include your name, address, daytime phone number, Social Security number or Employer Identification Number (EIN), the tax year, and the related tax form or notice number on the payment. Do not staple or attach the payment to your tax return. Send your payment to the IRS address specified in the instructions for your tax form. Always ensure you mail it well before the deadline, considering postal delivery times.

Cash

While less common, you can pay your taxes with cash through IRS retail partners. This involves an online process to generate a payment barcode, which you then take to a participating retail location (e.g., 7-Eleven, Family Dollar) to make your cash payment. This option typically incurs a small service fee and is limited to payments under $500 per transaction.

Installment Agreements

If you owe taxes but cannot pay the full amount by the deadline, the IRS may allow you to make monthly payments through an installment agreement. You can apply for an installment agreement online, by phone, or by mail. While this option helps avoid immediate collection actions, interest and penalties may still apply until the full amount is paid. Setting up a payment plan is a responsible financial decision when facing a temporary inability to pay in full.

Navigating Payment Challenges and Penalties

Even with the best intentions, financial challenges can arise. Understanding how to address underpayment or non-payment can mitigate future complications.

What Happens If You Can’t Pay on Time?

Failure to pay taxes by the due date can result in penalties and interest.

- Failure-to-Pay Penalty: This is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, capped at 25% of your unpaid tax liability.

- Failure-to-File Penalty: If you don’t file on time, the penalty is generally 5% of the unpaid taxes for each month or part of a month your return is late, capped at 25%. If you file an extension, this penalty can often be avoided, but the failure-to-pay penalty will still apply to any unpaid taxes after the original due date.

- Interest: Interest is charged on underpayments and unpaid penalties. The interest rate can change quarterly and is based on the federal short-term rate plus 3 percentage points.

These charges can accumulate quickly, significantly increasing your overall tax burden.

Setting Up a Payment Plan

If you cannot pay your tax liability in full, the IRS offers several relief options:

- Short-Term Payment Plan: Allows up to 180 days to pay, though interest and penalties still apply.

- Offer in Compromise (OIC): An agreement between a taxpayer and the IRS that settles a tax liability for less than the full amount owed. An OIC may be an option if you can demonstrate you cannot pay your full tax liability or doing so would cause financial hardship.

- Installment Agreement: As mentioned, this allows you to make monthly payments for up to 72 months. You can set this up online if you owe a combined total of under $50,000 (tax, penalties, and interest) for individuals or $25,000 for businesses.

Proactively contacting the IRS or setting up a payment plan is always better than ignoring your tax obligation.

Avoiding Future Payment Issues

Preventative financial planning is key to avoiding future tax payment issues.

- Adjust Withholding: For employees, review your W-4 form with your employer to ensure the correct amount of tax is withheld from your paycheck. Use the IRS Tax Withholding Estimator tool to fine-tune your withholding.

- Make Estimated Tax Payments: If you’re self-employed or have other income not subject to withholding, regularly calculate and pay estimated taxes quarterly.

- Save for Taxes: Set aside a portion of your income specifically for taxes in a dedicated savings account. This acts as an emergency fund for your tax obligations.

Smart Strategies for Tax Planning and Financial Health

Effective tax payment is deeply intertwined with overall financial health. By adopting proactive strategies, you can minimize surprises and optimize your financial position.

Regular Financial Review

Conducting regular financial reviews is paramount. This involves not just tracking income but also categorizing expenses, monitoring investments, and reviewing your budget. A clear picture of your financial inflows and outflows throughout the year helps you anticipate tax liabilities, identify potential deductions, and adjust your financial strategy as needed. Integrating tax planning into your routine financial checks ensures that you’re always prepared.

Leveraging Tax Software and Professionals

For many, tax software offers an affordable and efficient way to prepare and pay taxes. These programs guide you step-by-step, flagging potential errors and identifying overlooked deductions or credits. For those with more complex financial situations—such as business owners, high-net-worth individuals, or those with significant investment activity—engaging a qualified tax professional is an invaluable investment. They can offer personalized advice, navigate intricate tax laws, and develop strategies that optimize your tax position while ensuring full compliance. The cost of a professional is often offset by the financial benefits they provide, from uncovering legitimate deductions to representing you in audits.

Proactive Estimated Tax Payments

For self-employed individuals, freelancers, gig workers, and those with substantial income from investments or other sources not subject to withholding, making proactive estimated tax payments is critical. Underpaying your estimated taxes can lead to penalties, even if you pay your final tax bill on time. Use Form 1040-ES worksheets to accurately estimate your income and deductions for the year, and commit to making those quarterly payments diligently. This approach avoids a large, unexpected tax bill at year-end and helps manage cash flow throughout the year.

Building an Emergency Fund

One of the most effective strategies for seamless tax payment is to maintain a robust emergency fund. An emergency fund, typically 3-6 months of living expenses, can also serve as a buffer for unexpected tax liabilities or when there’s a temporary dip in income that affects your ability to make payments. Having these funds readily available prevents financial distress, avoids high-interest credit card debt for tax payments, and ensures you can meet your obligations without compromising other financial goals.

Paying taxes to the IRS is an integral part of responsible financial management. By understanding your obligations, preparing diligently, utilizing the appropriate payment methods, and engaging in smart financial planning, you can navigate the tax landscape confidently and maintain a healthy financial standing.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.