Navigating the landscape of tax obligations can often feel daunting, yet making your IRS tax payment is a fundamental aspect of financial responsibility for individuals and businesses alike. While the idea of paying taxes might not spark joy, understanding the various methods available to satisfy your IRS debt is crucial for maintaining compliance, avoiding penalties, and managing your personal or business finances effectively. In an era where digital transactions are prevalent, the IRS has significantly expanded its payment options, moving beyond traditional paper checks to embrace electronic methods that offer convenience, speed, and enhanced security.

This comprehensive guide will demystify the process, offering a clear roadmap to understanding your payment obligations, exploring the myriad of payment avenues, and outlining best practices for ensuring your payments are made accurately and on time. From direct electronic transfers to more traditional approaches and even options for those facing financial hardship, we’ll cover the essential details you need to confidently manage your federal tax payments, keeping you firmly in control of your financial well-being.

Understanding Your Tax Obligation and Deadlines

Before diving into how to pay, it’s essential to understand what you’re paying and when it’s due. A clear grasp of your tax obligations and the relevant deadlines is the first line of defense against penalties and unnecessary stress.

Types of IRS Payments

The IRS collects various types of payments, and the method suitable for one might be different for another. The most common payments include:

- Income Tax (Annual Filing): This is the tax you owe when you file your annual federal income tax return (Form 1040, 1120, etc.). It typically covers the previous tax year’s earnings.

- Estimated Tax: If you earn income not subject to withholding (e.g., self-employment income, interest, dividends, rent, alimony), you generally need to pay estimated tax throughout the year in quarterly installments. This prevents a large tax bill and potential penalties at year-end.

- Extension Payments: If you file for an extension of time to file your return, you must still pay any tax due by the original deadline to avoid penalties and interest. An extension only grants more time to file, not to pay.

- Payroll Taxes: Businesses with employees are responsible for withholding and paying payroll taxes (Social Security, Medicare, and federal income tax withholding) on behalf of their employees.

- Excise Taxes: Certain businesses may be required to pay excise taxes on specific goods, services, or activities.

Key Tax Deadlines to Remember

While specific dates can shift slightly due to weekends or holidays, the primary tax deadlines are generally consistent:

- April 15th: The most famous deadline for individual income tax returns (Form 1040) and payment of any tax due for the prior year. This is also the deadline for the first quarterly estimated tax payment.

- June 15th: Second quarterly estimated tax payment deadline.

- September 15th: Third quarterly estimated tax payment deadline.

- January 15th (of next year): Fourth and final quarterly estimated tax payment deadline for the current year.

- Business Tax Deadlines: Corporations (Form 1120) and partnerships (Form 1065) have different filing and payment deadlines, typically March 15th or April 15th, depending on their fiscal year.

Penalties for Late or Underpayment

The IRS imposes penalties for various transgressions, including:

- Failure to Pay: A penalty for not paying the tax you owe by the due date. This is typically 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, capped at 25%.

- Failure to File: A penalty for not filing your tax return by the due date. This is usually 5% of the unpaid taxes for each month or part of a month that a return is late, capped at 25% of your unpaid tax. If both apply, the failure-to-file penalty may be reduced by the failure-to-pay penalty.

- Underpayment of Estimated Tax: If you don’t pay enough tax throughout the year through withholding or estimated payments, you could face a penalty. The IRS generally requires you to pay at least 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% for high-income earners) to avoid this penalty.

Understanding these penalties underscores the importance of timely and accurate payments as a critical component of sound financial management.

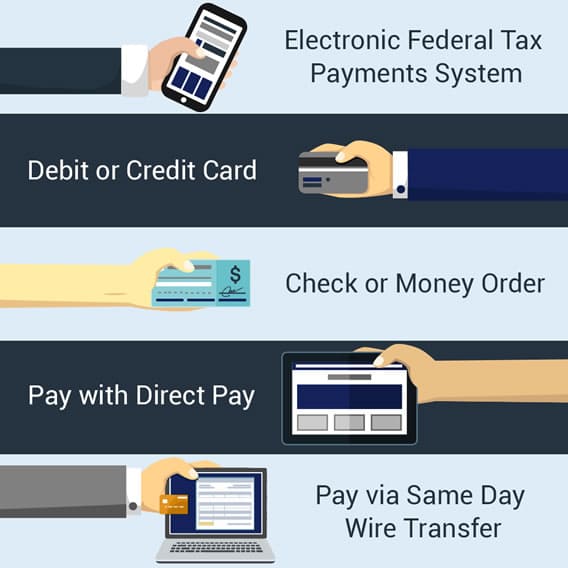

Common Electronic Payment Methods

In today’s digital age, electronic payment methods have become the preferred way to pay the IRS, offering convenience, security, and often instant confirmation. These methods are generally faster and reduce the risk of lost mail or delays.

IRS Direct Pay: The Free and Easy Way

IRS Direct Pay allows you to pay your tax bill or make estimated tax payments directly from your checking or savings account. It’s a free, secure, and user-friendly service provided by the IRS.

- Benefits: No fees, available 24/7, receive immediate confirmation number, can schedule payments up to 365 days in advance, and can cancel or change payments up to two business days before the scheduled date.

- How to Use: Access it directly on the IRS website (IRS.gov/directpay). You’ll need to verify your identity using basic tax information from a prior year’s return.

Electronic Federal Tax Payment System (EFTPS): For Businesses and Frequent Payers

EFTPS is a free service specifically designed for businesses and individuals who need to make federal tax payments frequently, such as payroll taxes or regular estimated tax payments.

- Benefits: Highly secure, robust system suitable for recurring payments, allows scheduling payments up to 365 days in advance, provides an audit trail.

- How to Use: Requires enrollment and an enrollment PIN, which is mailed to you. Once enrolled, you can pay online or by phone. It’s often mandated for businesses with certain tax liabilities.

Debit Card, Credit Card, or Digital Wallet Payments

The IRS partners with third-party payment processors to accept payments via debit card, credit card, or digital wallets (like PayPal, Click to Pay, or Apple Pay).

- Pros: Offers convenience, potential for earning credit card rewards, and flexibility.

- Cons: Third-party processors charge a fee, which varies depending on the processor and payment type (usually a flat fee for debit and a percentage for credit cards, typically 1.87% to 2.25%). These fees can add up for large payments.

- How to Use: You’ll select a processor from the IRS website, which will then direct you to their site to complete the transaction.

Electronic Funds Withdrawal (EFW) During E-File

When you electronically file your federal tax return (e-file) through tax software or a tax professional, you have the option to authorize an electronic funds withdrawal (EFW) directly from your bank account.

- Benefits: Integrates payment seamlessly with filing, no extra steps, confirms payment date during filing.

- How to Use: Simply select this option within your tax software or tell your tax preparer you wish to pay this way. You’ll provide your bank account details, and the payment will be debited on the due date.

Traditional Payment Options

While electronic payments offer unparalleled convenience, the IRS still provides traditional methods for those who prefer them or are unable to use digital solutions.

Paying by Check, Money Order, or Cashier’s Check

This is the classic method of payment. If you choose to pay by check, money order, or cashier’s check:

- How to: Make it payable to the “U.S. Treasury.” Write your name, address, daytime phone number, Social Security number (SSN), the tax year, and the related tax form or notice number on the check or money order.

- Mailing: Do not staple or attach the payment to your return. Mail it with a payment voucher (Form 1040-V for individuals) to the appropriate IRS address. The correct address depends on your location and the form you are filing, which can be found in the instructions for your tax form or on IRS.gov. Ensure it’s postmarked by the due date.

Paying with Cash

Paying with cash is possible, but it requires an extra step and is generally less convenient than other methods.

- How to: The IRS doesn’t accept cash payments directly at its offices. Instead, you can use a retail partner (like 7-Eleven or Family Dollar) to process your cash payment. You’ll need to go to IRS.gov/paywithcash to generate a payment barcode. You then take this barcode to a participating retail store to complete the payment.

- Limitations: There might be daily limits on cash payments, and processing can take a few business days. Always keep your receipt as proof of payment.

Installment Agreements and Offers in Compromise (When You Can’t Pay in Full)

If you find yourself unable to pay your tax liability in full by the due date, don’t ignore it. The IRS offers options to help taxpayers manage their debt, but it’s crucial to contact them or apply for these options proactively.

- Installment Agreement (IA): This allows you to make monthly payments for up to 72 months. You may apply online (for balances up to $50,000) or by mail using Form 9465, Installment Agreement Request. Interest and penalties still apply but may be reduced.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. The IRS generally approves an OIC when there is doubt as to collectibility, meaning they believe you cannot pay the full amount due. This is a more complex process and typically requires Form 656, Offer in Compromise.

- Temporary Delay in Collection (Currently Not Collectible Status): If you can prove that paying your taxes would cause significant financial hardship, the IRS might temporarily delay collection until your financial situation improves.

Verifying Your Payment and Record Keeping

Making a payment is only half the battle; ensuring it’s properly recorded and keeping meticulous records are vital steps in effective financial management.

Confirming Your Payment Was Received

After making a payment, especially via electronic methods, it’s wise to verify its receipt.

- IRS Direct Pay/EFTPS: These systems provide immediate confirmation numbers. Retain these numbers as proof of payment. You can also view your payment history within these platforms.

- Debit/Credit Card: The third-party processor will provide a confirmation. Your bank or credit card statement will also show the transaction.

- Check/Money Order: Keep a copy of your check or money order, and monitor your bank statement to ensure it clears. The IRS will send a confirmation notice if there are any issues.

- IRS Online Account: You can create or access your IRS online account to view your payment history and current balance due for the past three years. This is an excellent tool for verification.

Importance of Keeping Records

Thorough record-keeping is not just good practice; it’s a necessity for tax compliance and dispute resolution.

- What to Keep: Always keep copies of all tax returns, supporting documents (W-2s, 1099s, receipts), and records of all payments made to the IRS. This includes confirmation numbers, bank statements showing debits, and postal receipts if you mailed a payment.

- Why It Matters: These records serve as your proof of compliance. If there’s ever a discrepancy or an IRS inquiry, your accurate records will be invaluable in demonstrating that you met your obligations. Keep records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later.

What to Do if You Made a Payment Error

Mistakes can happen. If you realize you’ve made an error in your payment (e.g., incorrect amount, wrong tax year):

- Overpayment: If you overpaid, the IRS will typically apply the excess to your next year’s tax liability or issue a refund. For larger, unintentional overpayments, you may be able to contact the IRS to request a refund, though this process can be lengthy.

- Underpayment: If you underpaid, pay the difference as soon as possible to minimize additional interest and penalties.

- Incorrect Bank Account/Payment Method: If an electronic payment fails due to incorrect bank information, the IRS will notify you. You will then need to resubmit the payment using the correct details.

- Contact the IRS: For any significant payment errors or if you’re unsure how to proceed, contact the IRS directly via their taxpayer assistance lines or consult with a tax professional.

Strategic Considerations for Tax Payments

Beyond merely fulfilling an obligation, strategically managing your tax payments can have a positive impact on your overall financial health.

Timing Your Payments for Cash Flow

For businesses and self-employed individuals, timing estimated tax payments can be crucial for cash flow management.

- Spread Out Payments: Instead of one large lump sum, utilize quarterly estimated payments to align with income generation, preventing a sudden drain on capital.

- Pre-Payment: If you anticipate a large tax bill, making additional payments throughout the year, even beyond estimated payment requirements, can help avoid a significant year-end surprise and associated penalties.

- Withholding Adjustments: For employees, regularly reviewing and adjusting your W-4 form with your employer can fine-tune your tax withholding, aiming for a balance that avoids both a massive refund (which is essentially an interest-free loan to the government) and a significant amount due.

Utilizing Tax Software for Seamless Payments

Modern tax software (e.g., TurboTax, H&R Block, FreeTaxUSA) not only helps prepare your return but also streamlines the payment process.

- Integrated Payment Options: Most software allows you to choose from various electronic payment methods (EFW, credit/debit card, IRS Direct Pay setup) directly within the application.

- Error Reduction: By linking payment directly to your prepared return, the software helps ensure the correct amount, tax year, and identifying information are associated with your payment, reducing manual errors.

- Reminders: Some software also offers reminders for estimated tax payments, helping you stay on schedule.

The Role of Tax Professionals in Payment Strategies

A qualified tax professional (CPA, Enrolled Agent, tax attorney) can provide invaluable guidance, especially for complex financial situations.

- Estimated Tax Calculations: They can help accurately calculate your estimated tax obligations to minimize underpayment penalties.

- Payment Planning: A professional can integrate your tax payment strategy into your broader financial plan, considering investments, business income, and potential deductions.

- Resolving Issues: If you face difficulties paying or have received IRS notices, a tax professional can intercede on your behalf, negotiate payment plans, or address discrepancies. Their expertise can save you time, money, and stress.

Paying your IRS tax payment doesn’t have to be a source of anxiety. By understanding the various methods available, adhering to deadlines, and employing smart financial practices, you can fulfill your tax obligations efficiently and confidently. Utilizing the array of electronic options, maintaining meticulous records, and seeking professional advice when needed are key steps toward mastering this essential aspect of personal and business finance. Staying proactive and informed ensures that your relationship with the IRS remains compliant and your financial house stays in order.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.