Navigating the American tax system can be a daunting endeavor, particularly for those whose income is not subject to standard employer withholding. For freelancers, small business owners, investors, and high-net-worth individuals, the concept of “tax season” is not a once-a-year event in April; it is a quarterly commitment. The internal Revenue Service (IRS) operates on a “pay-as-you-go” basis, and failing to meet these periodic obligations can lead to significant penalties and interest.

Fortunately, the digital transformation of financial services has made fulfilling these obligations easier than ever. Understanding how to pay estimated taxes online is not just a matter of compliance; it is a critical component of professional financial management. This guide explores the “why,” the “when,” and the “how” of online estimated tax payments, ensuring you stay in the good graces of the IRS while maintaining optimal cash flow.

Understanding the Fundamentals of Estimated Tax Payments

Before diving into the technical steps of online payment, one must understand the underlying principles of estimated taxes. Unlike traditional W-2 employees, whose taxes are deducted from every paycheck, the self-employed and those with significant non-wage income must manually calculate and send their tax contributions to the government.

Who is Required to Pay?

The IRS generally requires individuals to make estimated tax payments if they expect to owe $1,000 or more when their return is filed. This typically applies to sole proprietors, partners in a business, and S-corporation shareholders. However, it also impacts individuals with significant income from interest, dividends, alimony, capital gains, or prizes. If your employer does not withhold enough tax from your salary or pension, you may also find yourself in the position of needing to make estimated payments to bridge the gap.

The “Pay-as-You-Go” Tax System Explained

The United States tax system is designed to collect revenue throughout the year as income is earned. This prevents the government from facing liquidity issues and prevents taxpayers from being hit with a massive, unmanageable bill at the end of the fiscal year. By paying quarterly, you are essentially pre-paying your income tax and self-employment tax. This systemic approach helps in maintaining personal financial discipline, as it prevents the “sticker shock” that often accompanies a poorly planned tax year.

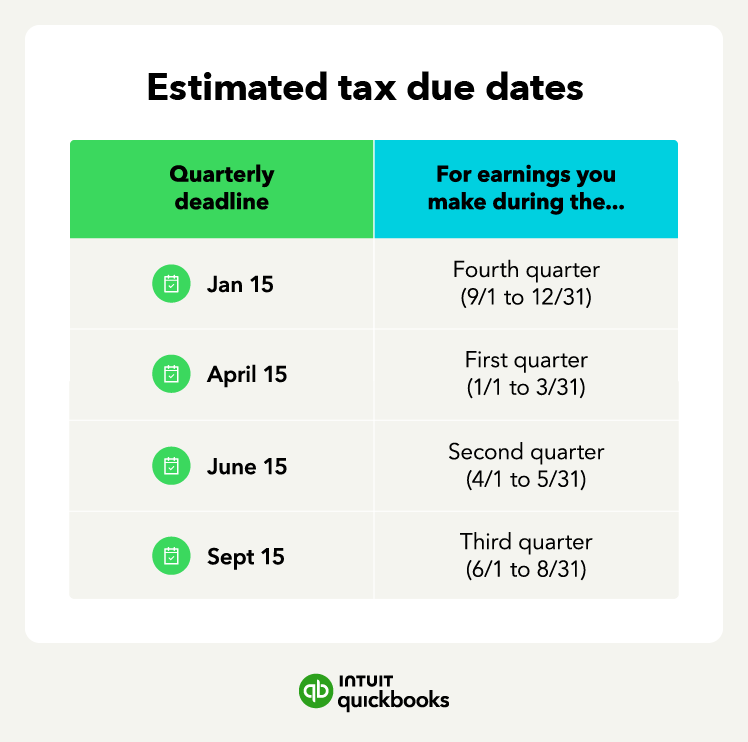

Deadlines You Cannot Afford to Miss

Estimated tax payments are divided into four distinct periods. Generally, the deadlines are April 15, June 15, September 15, and January 15 of the following year. If these dates fall on a weekend or a legal holiday, the deadline is pushed to the next business day. Missing these deadlines, even by a day, can result in underpayment penalties, even if you eventually pay the full amount due when you file your annual return. Online payment platforms are particularly beneficial here, as they provide instant confirmation and eliminate the “lost in the mail” risk associated with paper checks.

Essential Online Portals and Tools for Tax Payments

The IRS has invested heavily in its digital infrastructure to streamline the collection process. There are several primary methods to pay estimated taxes online, each catering to different needs and levels of technical comfort.

IRS Direct Pay: The Simplest Method

For most individual taxpayers, IRS Direct Pay is the gold standard for convenience. This service allows you to pay your estimated tax directly from your checking or savings account without any processing fees. One of the primary advantages of Direct Pay is that it does not require a lengthy registration process. You can simply verify your identity using information from a previous year’s tax return and complete your transaction in minutes. It is a secure, “one-and-done” solution for those who prefer not to manage another set of login credentials.

EFTPS: The Corporate and High-Volume Standard

The Electronic Federal Tax Payment System (EFTPS) is a more robust tool, often preferred by businesses and high-income individuals who want more control over their payment history. Unlike Direct Pay, EFTPS requires an initial enrollment process, which involves receiving a PIN via physical mail. Once registered, however, EFTPS offers superior features, such as the ability to schedule payments up to 365 days in advance and a comprehensive 16-month history of all payments made. For those who view tax management as a core part of their business finance strategy, EFTPS is the professional choice.

Paying via Debit or Credit Card

If you prefer to use a card—perhaps to earn travel rewards or to manage short-term cash flow—the IRS utilizes third-party payment processors like PayUSAtax or ACI Payments, Inc. While the IRS itself does not charge a fee for this, the processors do. These fees are usually a percentage of the total payment. From a financial strategy perspective, this method is only advisable if the value of the rewards earned outweighs the processing fee, or if using a credit card is a necessary temporary measure to avoid a more expensive IRS underpayment penalty.

Step-by-Step Guide to Using IRS Direct Pay

Since IRS Direct Pay is the most common route for individual estimated payments, understanding its workflow is essential for efficient financial management.

Selecting Your Payment Type

Upon arriving at the Direct Pay website, your first task is to select the “Reason for Payment.” For quarterly taxes, you must select “Estimated Tax.” You will then be prompted to select the specific form (1040-ES) and the tax year for which you are paying. Accuracy here is paramount; applying a payment to the wrong tax year can lead to an “unpaid” status for the current quarter and a complicated correction process later.

Verifying Your Identity

To ensure security, the IRS requires you to verify your identity using data from a tax return filed within the last five to six years. You will need to provide your Name, Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), Date of Birth, and the Filing Status used on that specific past return. This step acts as a digital signature, confirming that the person authorized to move funds is indeed the taxpayer.

Confirming and Documenting Your Payment

After entering your bank account details (Routing and Account numbers), you will reach a review screen. Professional financial hygiene dictates that you double-check every digit. Once you submit the payment, the system generates a confirmation number. Do not close the browser until you have saved this number. Whether you print it to a PDF or log it in your accounting software, this confirmation number is your primary evidence of compliance should the IRS ever claim a payment was missed.

Strategies for Calculating Your Quarterly Liability

Knowing how to pay is only half the battle; knowing how much to pay is where the real financial expertise comes into play. Overpaying ties up capital that could be invested, while underpaying leads to penalties.

Using the Safe Harbor Rule

The IRS provides a “Safe Harbor” provision to protect taxpayers from penalties. Generally, you will not face a penalty if you pay at least 90% of the tax you owe for the current year, or 100% of the tax shown on your return for the prior year (110% if your adjusted gross income was more than $150,000). For many, paying based on the prior year’s liability is the safest and simplest strategy, as it provides a fixed number to work with regardless of how much your income fluctuates in the current year.

Leveraging Accounting Software for Accuracy

In the modern era, manual ledger entries are becoming obsolete. Tools like QuickBooks, FreshBooks, or specialized tax software can track your income and expenses in real-time, providing an ongoing estimate of what you owe. By integrating your bank accounts with these financial tools, you can see a “tax due” widget that updates with every invoice paid. This level of insight allows for more precise payments than the Safe Harbor rule might suggest, keeping your capital more liquid.

Adjusting for Fluctuating Income

If your business is seasonal—for example, a retail business that makes 60% of its income in Q4—making four equal payments might not make sense. The IRS allows for the “Annualized Income Installment Method,” which lets you pay tax based on what you actually earned during each specific window. While this requires more complex record-keeping (Form 2210), it is a sophisticated financial move that aligns your tax outgoings with your actual cash inflows.

Common Pitfalls and How to Avoid Penalties

Even with the best intentions, errors can occur. Being aware of the most common mistakes can save you hours of administrative headaches and hundreds of dollars in interest.

Managing Underpayment Penalties

The underpayment penalty is calculated based on how much you owed and how long it remained unpaid. It is essentially an interest charge. If you realize mid-year that you have underpaid for the first two quarters, the best move is to pay the deficit as soon as possible through the online portals. You don’t have to wait for the next deadline. Paying early stops the “interest clock” from ticking further.

The Importance of Record Keeping

The IRS is an organization built on documentation. When you pay online, you receive digital receipts, but these should not exist in a vacuum. A professional approach involves maintaining a “Tax Folder” (either physical or digital) where every confirmation number is cross-referenced with your bank statements. When you file your annual return, you will need to list each quarterly payment date and amount precisely to ensure you receive full credit for the taxes you have already paid.

Avoiding Identity and Technical Errors

Small mistakes can have large consequences. Ensure that the SSN entered during the online payment matches the primary taxpayer listed on the return. If you are married filing jointly, it is usually best to make all estimated payments under the SSN of the spouse who will be listed first on the 1040 form. Additionally, ensure your bank account has sufficient funds before initiating a Direct Pay transaction; a “returned payment” for insufficient funds can carry its own set of IRS penalties, similar to a bounced check.

Conclusion

Mastering the process of paying estimated taxes online is a hallmark of financial maturity. By utilizing tools like IRS Direct Pay or EFTPS, staying disciplined with quarterly deadlines, and using sophisticated calculation strategies like the Safe Harbor rule, you transform a potentially stressful obligation into a routine administrative task. In the world of personal and business finance, clarity and consistency are the keys to long-term success. By staying ahead of your tax obligations, you ensure that your focus remains where it belongs: on growing your income and securing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.