Managing your Chase credit card payments effectively is a cornerstone of sound personal finance. Timely payments not only help you avoid late fees and maintain a healthy credit score but also contribute significantly to your overall financial well-being. Chase, as one of the largest credit card issuers, offers a variety of convenient methods to ensure you can make your payments easily and on time. Understanding these options, along with key strategies for financial management, is essential for every Chase cardholder.

Understanding Your Chase Credit Card Statement and Due Dates

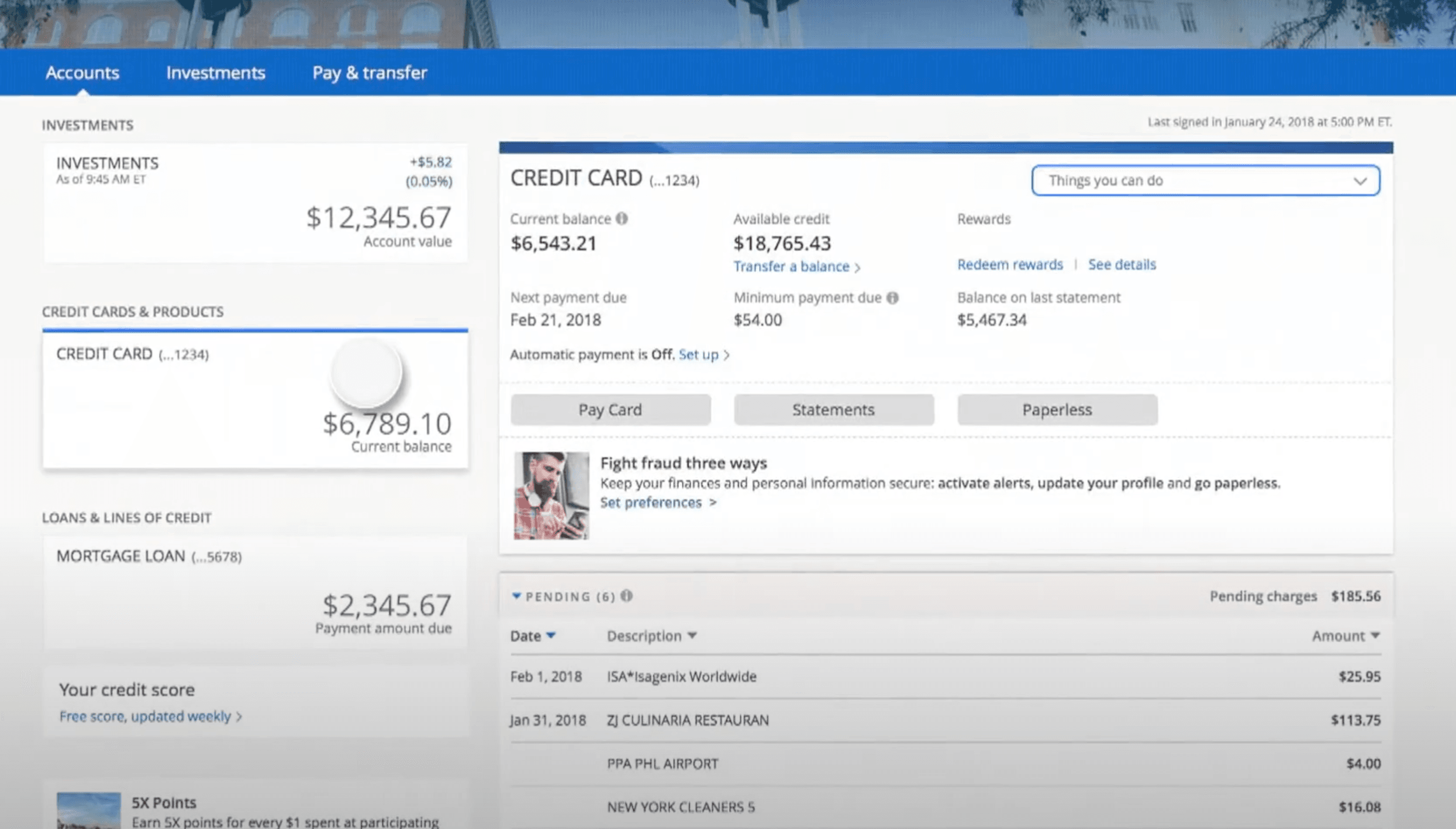

Before diving into payment methods, it’s crucial to understand the information presented on your monthly Chase credit card statement. This document is more than just a bill; it’s a comprehensive overview of your spending, payments, and account status.

Decoding Your Monthly Statement

Your Chase credit card statement provides critical details you need to review each month. Key sections typically include:

- Previous Balance: The amount you owed at the end of the last billing cycle.

- New Charges/Credits: A detailed list of all purchases, cash advances, balance transfers, and any returns or adjustments made during the current billing cycle.

- Payments Received: A record of any payments you made since your last statement.

- New Balance: The total amount you currently owe, calculated by adding new charges to the previous balance and subtracting payments and credits.

- Minimum Payment Due: The lowest amount you must pay by the due date to avoid late fees and penalties. While paying only the minimum might seem appealing, it can lead to higher interest charges and a longer repayment period.

- Payment Due Date: The deadline by which your payment must be received by Chase. Missing this date can result in late fees and a potential negative impact on your credit score.

- Interest Rate (APR): The annual percentage rate applied to different types of balances (purchases, cash advances, balance transfers).

- Rewards Summary: If your card earns rewards, this section details how many points, miles, or cash back you’ve earned.

Thoroughly reviewing your statement each month helps you track your spending, identify any unauthorized transactions, and plan your payments accordingly. Understanding the components allows for better financial oversight and helps you catch potential errors before they become significant issues.

Importance of Payment Due Dates and Grace Periods

The payment due date is perhaps the most critical piece of information on your statement. Chase, like most issuers, provides a grace period—the time between the end of your billing cycle and the payment due date—during which interest is not charged on new purchases if you pay your entire statement balance in full by the due date. If you carry a balance from month to month, or if you don’t pay your full statement balance, you will generally be charged interest on new purchases from the date they are posted. Always aim to pay at least the minimum amount by the due date to avoid late fees and protect your credit score. Ideally, paying the full statement balance is the best strategy to avoid interest charges entirely. Setting up reminders or using automatic payments can significantly help in meeting these crucial deadlines consistently.

Convenient Methods to Pay Your Chase Credit Card Bill

Chase offers a robust suite of payment options, catering to various preferences and situations. Choosing the method that best suits your routine can streamline your financial management.

Online Payment via Chase.com

Paying online through Chase.com is one of the most popular and efficient methods. Once logged into your Chase account, you can easily navigate to your credit card dashboard. Here, you’ll find options to “Make a Payment.” You can choose to pay the minimum amount due, the statement balance, your current balance, or a custom amount. Payments can be scheduled for immediate processing or a future date, and you can link a checking or savings account from Chase or another financial institution. This method provides immediate confirmation and allows you to view your payment history, offering transparency and control. For those who manage multiple Chase accounts, the platform provides a consolidated view, making it easy to manage all your financial products in one place. Ensure you initiate payments with enough lead time, especially if paying from an external bank, as it might take a few business days for the funds to fully clear.

Chase Mobile App Payments

For on-the-go convenience, the Chase Mobile app is an excellent tool. Available for both iOS and Android devices, the app allows you to manage your accounts, view transactions, and make payments from virtually anywhere. After logging in with your secure credentials, select your credit card account and tap the “Pay” or “Make a Payment” option. Similar to the website, you can select the payment amount and the funding account. The mobile app also offers features like setting up payment reminders, viewing your credit score, and managing reward points, making it a comprehensive financial management tool in your pocket. The app typically offers a streamlined user experience, making payments quick and intuitive, often just a few taps away.

Automated Phone System Payments

If you prefer to pay by phone, Chase provides an automated phone system. You can call the customer service number typically found on the back of your credit card or on your statement. Follow the prompts to make a payment using your checking or savings account. This method is available 24/7 and can be a good option if you don’t have internet access or prefer to use a phone. Ensure you have your credit card number, bank account number, and routing number ready when you call. While efficient, always listen carefully to the prompts and confirmation details to ensure your payment is processed correctly.

Mail-In Payments

For those who prefer traditional methods, you can still mail a check or money order. Your monthly statement will include a payment coupon and the correct mailing address. It’s crucial to mail your payment several business days before your due date to account for postal delivery times. Delays in mail can result in a late payment, even if you mailed it on time. Always write your credit card account number on your check or money order to ensure it’s applied correctly to your account. This method, while slower, remains a viable option for some cardholders.

In-Branch Payments

If you have a Chase bank branch near you, you can make a payment in person. Simply bring your credit card statement or account number, along with your payment (check, cash, or money order), to a teller. Payments made in-branch are typically processed immediately, offering peace of mind. This option can be particularly useful if you have questions about your statement or need to discuss your account with a representative. It combines the immediacy of an electronic payment with the personal touch of face-to-face assistance.

Third-Party Bill Pay Services

Many banks and credit unions offer their own online bill pay services that allow you to set up payments to various creditors, including Chase. You’ll typically need to add Chase as a payee, providing your credit card account number and the Chase payment address (which can usually be found on your statement). While convenient for consolidating all your bill payments in one place, be mindful of the processing times, as third-party services might take an extra day or two to send the payment to Chase. Schedule these payments well in advance of your due date to avoid any issues.

Setting Up Automatic Payments for Peace of Mind

One of the most effective strategies for ensuring timely payments and avoiding late fees is setting up automatic payments. This feature allows Chase to automatically deduct a specified amount from your linked bank account on a recurring basis.

How to Enroll in Autopay

Enrolling in Autopay for your Chase credit card is straightforward and can be done through Chase.com or the Chase Mobile app. Navigate to your credit card account, look for a “Payments” or “Autopay” section, and follow the instructions. You’ll typically be asked to:

- Select Payment Amount: You can choose to pay the minimum payment due, the full statement balance, the current balance, or a fixed amount each month. Paying the full statement balance is highly recommended to avoid interest charges.

- Choose Payment Date: While Chase generally schedules Autopay for your due date, you may have some flexibility to select a date slightly before or on the due date.

- Link Bank Account: Provide the routing number and account number for the checking or savings account you wish to use for payments.

Once set up, you’ll usually receive a confirmation email. Autopay takes the hassle out of remembering due dates and manually initiating payments each month, providing a reliable safety net against oversights.

Benefits and Considerations of Autopay

The primary benefit of Autopay is convenience and peace of mind. It ensures your payments are always made on time, helping you avoid late fees and maintain a positive payment history, which is a major factor in your credit score. For those who frequently travel or have busy schedules, Autopay is an invaluable tool.

However, there are considerations. If you choose to pay the full statement balance, ensure that your linked bank account always has sufficient funds to cover the payment. An insufficient funds (NSF) situation could lead to fees from both your bank and Chase. Regularly review your statements, even with Autopay, to monitor spending and catch any discrepancies. If your income or spending habits fluctuate significantly, you might prefer to manually review and adjust your payment amount each month, or at least ensure your autopay settings align with your financial capacity.

Managing Your Autopay Settings

Your Autopay settings are not set in stone. You can modify them at any time through Chase.com or the mobile app. This includes changing the payment amount (e.g., from minimum to full balance), updating your linked bank account, or even canceling Autopay if your financial situation changes. It’s a good practice to review your Autopay settings periodically, especially if you get a new bank account or want to adjust your payment strategy. Be aware that changes typically require a few days to take effect, so plan accordingly if a payment is due soon.

Strategies for Timely Payments and Financial Health

Beyond the mechanics of making a payment, adopting smart financial habits can profoundly impact your relationship with your Chase credit card and your overall financial health.

Budgeting for Credit Card Payments

Integrating your credit card payments into your monthly budget is fundamental. Treat your credit card bill as a fixed expense, just like rent or utilities. Allocate funds specifically for your credit card payment each month, aiming to cover the full statement balance whenever possible. Using budgeting apps, spreadsheets, or even a simple pen-and-paper system can help you track your income and expenses, ensuring you always have sufficient funds available when your Chase bill is due. A well-structured budget provides clarity and prevents payment surprises, promoting responsible credit usage.

Paying More Than the Minimum

While paying the minimum amount due prevents late fees, it is rarely the best financial strategy. Paying only the minimum can extend your repayment period significantly and result in substantially more interest paid over time, especially if you carry a high balance. Whenever feasible, strive to pay your full statement balance. If that’s not possible, pay as much as you can above the minimum. Even an extra $50 or $100 can make a notable difference in reducing your principal balance faster, thus lowering the total interest accrued and accelerating your path to debt-free status. This proactive approach improves your debt-to-income ratio and strengthens your financial standing.

Consolidating Due Dates

If you have multiple credit cards, especially multiple Chase cards, you might find it beneficial to consolidate their due dates. While Chase doesn’t typically allow you to change your assigned billing cycle start date, you can sometimes request to adjust your payment due date to better align with your paychecks or other bills. Having all your credit card payments due around the same time can simplify your financial calendar, making it easier to remember and manage multiple obligations. Contact Chase customer service to inquire about adjusting your due date for individual cards. This can reduce the mental load of remembering several disparate deadlines.

Payment Reminders and Alerts

Leverage technology to your advantage. Chase offers various alerts and notifications that can remind you when your payment due date is approaching, when your statement is available, or when your payment has been posted. You can customize these alerts through your online account or the mobile app. Additionally, many personal finance apps and calendar tools can be used to set up recurring reminders. Combining these with Autopay provides an extra layer of protection against missed payments, reinforcing good financial habits without constant manual effort.

What Happens If You Miss a Payment?

Missing a payment, even by a single day, can have several negative consequences. Understanding these repercussions can underscore the importance of consistent, timely payments.

Late Fees and Penalty APRs

The most immediate consequence of a missed payment is a late fee, which Chase will typically charge once your payment is not received by the due date. The amount of the late fee is usually specified in your cardholder agreement and on your statement. Beyond a single late fee, chronic late payments can trigger a penalty APR (Annual Percentage Rate). This is a significantly higher interest rate that can be applied to your existing balance and future purchases. A penalty APR can dramatically increase the cost of carrying a balance, making it much harder to pay off your debt. This increased rate often remains in effect for a period, typically six months, or until you make several consecutive on-time payments.

Impact on Credit Score

Your payment history is the single most important factor in calculating your credit score (accounting for 35% of your FICO score). A payment that is 30 days or more overdue will likely be reported to the major credit bureaus (Experian, Equifax, and TransUnion) and will appear on your credit report. This negative mark can significantly lower your credit score, making it harder to qualify for new loans, mortgages, or even certain jobs or insurance policies in the future. The impact of a late payment can linger on your credit report for up to seven years. Even a single 30-day late payment can have a more severe effect than a high credit utilization ratio, highlighting the criticality of on-time payments.

Seeking Assistance from Chase

If you anticipate difficulty making a payment on time, or if you’ve already missed one, it’s always best to contact Chase customer service as soon as possible. While they are not obligated to waive fees or alter terms, explaining your situation proactively might lead to some leniency, especially if you have a good payment history. They might offer options such as a payment arrangement, temporary hardship program, or a one-time late fee waiver. Ignoring the issue will only worsen the situation. Being transparent and seeking help demonstrates responsibility, which can be viewed favorably.

Paying your Chase credit card bill is a fundamental aspect of financial management. By understanding your statement, utilizing the various convenient payment methods, embracing automation, and practicing sound financial habits, you can maintain a healthy credit score, avoid unnecessary fees, and ensure your financial well-being remains on track.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.