Tax season is often viewed through a lens of administrative burden, yet for the savvy taxpayer, it represents the most significant financial event of the year. Maximizing a tax return is not merely about finding a few forgotten receipts in April; it is an exercise in comprehensive financial engineering. It requires an understanding of how the tax code incentivizes specific economic behaviors—from investing in your future to supporting your family and growing a business.

Whether you are a W-2 employee, a freelancer in the gig economy, or a high-net-worth investor, the objective remains the same: to minimize your tax liability and ensure that every dollar you are legally entitled to keep remains in your pocket. By shifting from a reactive “filing” mindset to a proactive “planning” mindset, you can transform your tax return from a modest check into a powerful tool for wealth accumulation.

Mastering the Art of Deductions and Credits

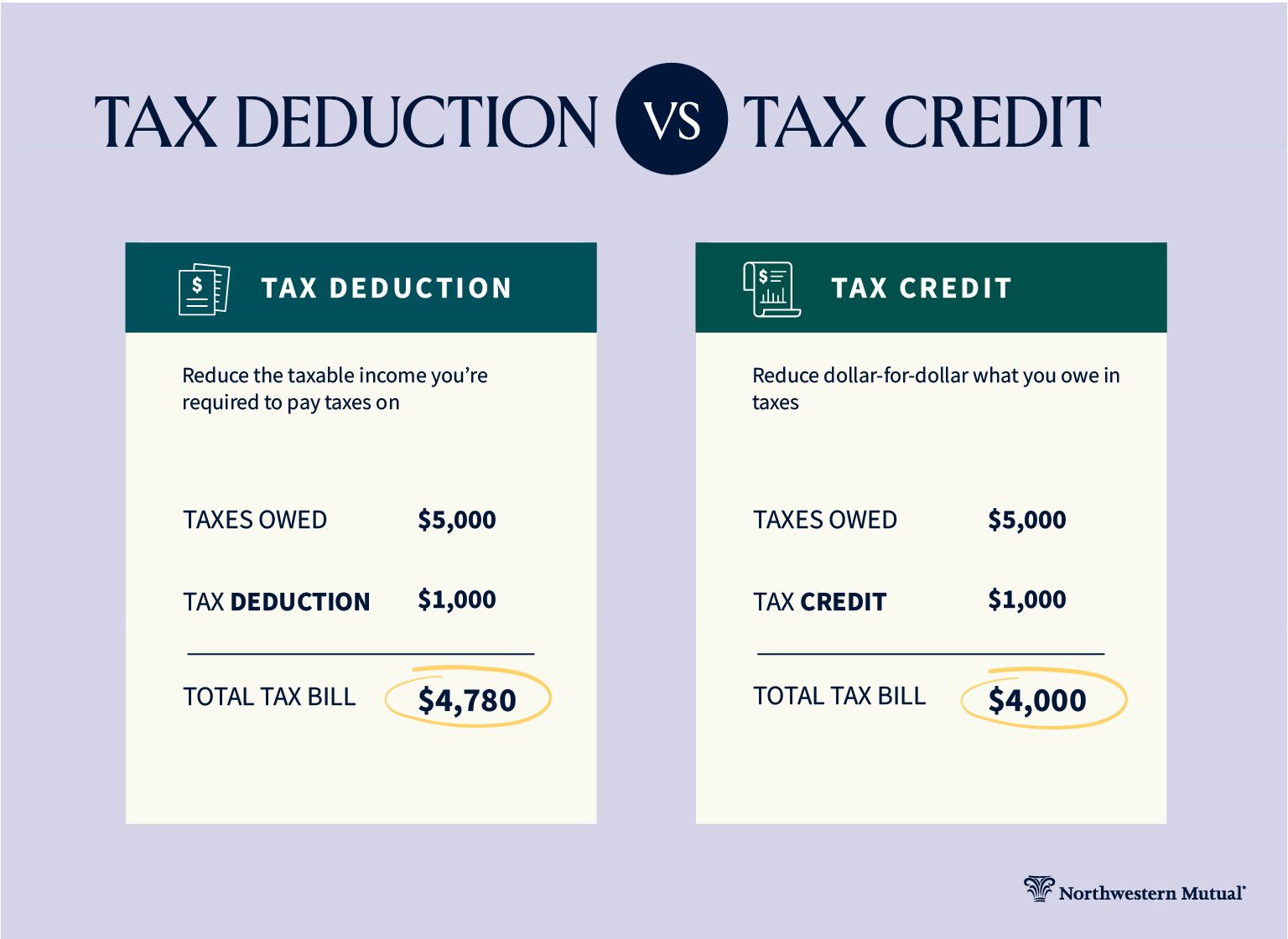

The foundation of any successful tax strategy lies in the distinction between deductions and credits. While both reduce your overall tax burden, they do so in fundamentally different ways. Deductions lower your taxable income, while credits provide a dollar-for-dollar reduction in the actual tax you owe. To maximize your return, you must master the application of both.

Standard vs. Itemized Deductions

The first major decision every taxpayer faces is whether to take the standard deduction or to itemize. Since the passage of the Tax Cuts and Jobs Act (TCJA), the standard deduction has nearly doubled, making it the most efficient choice for the majority of Americans. However, if your qualifying expenses—such as mortgage interest, state and local taxes (SALT) up to $10,000, medical expenses exceeding 7.5% of your adjusted gross income (AGI), and charitable contributions—exceed the standard threshold, itemizing is essential.

A strategic “bunching” strategy can be particularly effective here. By concentrating two years’ worth of charitable donations or elective medical procedures into a single tax year, you may surpass the standard deduction limit in “Year A” while taking the standard deduction in “Year B,” thereby maximizing your total tax savings over a 24-month period.

Maximizing Family and Education Credits

Tax credits are the most potent tools for increasing a refund because they directly offset your tax bill. The Child Tax Credit (CTC) remains a cornerstone for families, but many overlook the Child and Dependent Care Credit, which can help recoup costs associated with daycare or summer camps.

For those investing in their own or their children’s future, education credits are vital. The American Opportunity Tax Credit (AOTC) provides a credit for the first four years of post-secondary education, while the Lifetime Learning Credit (LLC) is available for an unlimited number of years, including for professional development courses. Understanding the eligibility phase-outs for these credits is crucial for high-earning households seeking to optimize their returns.

The Earned Income Tax Credit (EITC)

Often overlooked by those whose income fluctuates, the EITC is a refundable credit designed for low-to-moderate-income working individuals and couples, particularly those with children. Because it is refundable, it can result in a refund even if you owe zero taxes. If your income dropped significantly during the year due to a career change or a period of unemployment, checking your eligibility for the EITC can result in one of the largest single boosts to your tax return.

Utilizing Tax-Advantaged Investment Vehicles

One of the most effective ways to lower your taxable income—and thus increase your refund—is to “hide” your money in plain sight through tax-advantaged accounts. This strategy serves the dual purpose of building long-term wealth while providing immediate fiscal relief.

Front-Loading Retirement Contributions

Contributions to a traditional 401(k) or 403(b) through an employer are made with pre-tax dollars, which lowers your reported income on your W-2. If you find yourself in a higher tax bracket than expected toward the end of the year, increasing your contribution percentage can lead to significant savings. Similarly, contributions to a Traditional IRA may be tax-deductible depending on your income level and whether you have access to a workplace retirement plan. By contributing to these accounts, you are essentially paying your future self while simultaneously reducing the amount the government can claim today.

The Power of Health Savings Accounts (HSAs)

The HSA is arguably the most powerful financial tool in the tax code. If you have a High Deductible Health Plan (HDHP), contributions to an HSA are 100% tax-deductible (or pre-tax via payroll), the funds grow tax-free, and withdrawals for qualified medical expenses are tax-free. Unlike a Flexible Spending Account (FSA), HSA funds roll over indefinitely. For those looking to maximize a tax return, maximizing an HSA contribution is an “above-the-line” deduction that reduces your AGI regardless of whether you itemize or take the standard deduction.

Capital Gains and Tax-Loss Harvesting

For investors with taxable brokerage accounts, the end of the year is the time for “tax-loss harvesting.” This involves selling underperforming assets at a loss to offset capital gains realized elsewhere in your portfolio. If your losses exceed your gains, you can use up to $3,000 of the excess loss to offset your ordinary income. This move not only cleanses your portfolio of “dead wood” but also serves as a direct lever to lower your taxable income and increase your refund.

Optimizing Taxes for Small Business Owners and Freelancers

The rise of the “side hustle” and freelance economy has opened new avenues for tax maximization that were previously reserved for corporations. If you earn any income outside of a traditional W-2 job, you are effectively a business owner in the eyes of the IRS, which allows you to deduct a wide array of “ordinary and necessary” expenses.

Tracking Home Office and Operational Expenses

The home office deduction is a powerful, yet often misunderstood, benefit. If you use a portion of your home exclusively for business, you can deduct a percentage of your rent, mortgage interest, utilities, and insurance. While the “simplified method” ($5 per square foot up to 300 square feet) is easier, the “actual expense method” often yields a much higher deduction for those living in high-cost-of-living areas. Furthermore, everyday costs such as internet service, professional software, and even a portion of your cellphone bill can be deducted to lower your business profit.

The Qualified Business Income (QBI) Deduction

Introduced under the TCJA, the Section 199A deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income from their taxes. This is a “below-the-line” deduction that reduces your taxable income but not your self-employment tax. Because the rules surrounding QBI are complex and subject to income thresholds and “specified service” limitations, optimizing your business structure to qualify for this deduction can be the difference between a standard return and a massive windfall.

Equipment Depreciation and Section 179

If your business requires equipment—be it a laptop, a vehicle, or specialized machinery—you don’t necessarily have to deduct the cost over several years. Section 179 of the tax code allows businesses to deduct the full purchase price of qualifying equipment in the year it was placed in service. For a freelancer who had a high-income year, purchasing necessary equipment before December 31st can provide a significant deduction that drastically reduces the tax liability for that year.

Year-Round Strategies for Long-Term Tax Efficiency

The most successful taxpayers do not wait until February to think about their return. They treat tax planning as a year-round discipline. By maintaining a constant pulse on your financial life, you avoid the “scramble” and ensure that no opportunities for savings are missed.

Adjusting Withholding via the W-4

While a large tax refund feels like a win, from a pure personal finance perspective, it represents an interest-free loan you gave to the government. If you consistently receive a massive refund, you may want to adjust your W-4 withholding with your employer. By bringing more of that money home in each paycheck and investing it in a high-yield savings account or the stock market, you can earn interest on that money throughout the year. Conversely, if you find you are always owing money, adjusting your withholding early in the year prevents a stressful tax bill and potential underpayment penalties.

Record-Keeping and Digital Financial Management

The difference between a deduction taken and a deduction missed is documentation. In the event of an audit, the IRS requires proof of expenses. Utilizing financial tools to track expenses in real-time—categorizing receipts as they happen—ensures that you capture every possible penny of deductible spend. Professionalism in your record-keeping translates directly into confidence in your filing, allowing you to take aggressive (but legal) positions on your deductions.

When to Hire a Professional Tax Strategist

As your income grows and your financial life becomes more complex (incorporating rental properties, K-1s from partnerships, or stock options), the ROI on hiring a Certified Public Accountant (CPA) or a tax strategist increases. A tax preparer tells you what you owed last year; a tax strategist tells you how to owe less next year. The fees paid for professional advice are often eclipsed by the savings they discover through sophisticated strategies like corporate restructuring, defined benefit plans, or advanced estate planning.

In conclusion, maximizing your tax return is a multifaceted process that blends meticulous record-keeping with strategic investment and a deep understanding of the current tax code. By viewing your taxes as a component of your broader wealth-building strategy, you can ensure that you are not just “filing,” but winning.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.