Navigating the complexities of tax season can be daunting, but understanding how to properly submit your tax payments to the Internal Revenue Service (IRS) is a fundamental aspect of financial responsibility. For individuals, small businesses, and large corporations alike, timely and accurate payment is crucial to avoid penalties and maintain good standing with federal tax authorities. This comprehensive guide will demystify the various payment methods available, offer insights into managing your tax obligations, and provide essential tips to ensure your payments are processed smoothly and securely.

The IRS offers a multitude of payment options, catering to diverse preferences and financial situations. From swift electronic transactions to more traditional mail-in methods, the key is to select the option that best suits your needs while adhering to critical deadlines. Ignoring or mishandling tax payments can lead to interest accruals and penalties, impacting your financial health. Therefore, a proactive and informed approach is not just advisable, but essential.

Understanding Your Tax Obligations and Payment Due Dates

Before even considering how to pay, it’s paramount to understand when and what you owe. Tax obligations are not a one-size-fits-all scenario, varying significantly based on income sources, business structure, and personal circumstances. Missing key deadlines can trigger penalties, making proactive planning a cornerstone of sound financial management.

Key Tax Deadlines for Individuals and Businesses

The most widely known tax deadline for individuals is April 15th (or the next business day if it falls on a weekend or holiday) for filing federal income tax returns and paying any taxes due. However, this is just one of several critical dates. Businesses, especially those organized as corporations or partnerships, have their own set of filing and payment deadlines, often varying by fiscal year end.

For self-employed individuals and those with significant income not subject to withholding (e.g., rental income, investment income), estimated tax payments are typically due quarterly. These payments are crucial to avoid underpayment penalties. The standard due dates for estimated taxes are:

- April 15: For income earned January 1 to March 31.

- June 15: For income earned April 1 to May 31.

- September 15: For income earned June 1 to August 31.

- January 15 of next year: For income earned September 1 to December 31.

It is vital to mark these dates on your calendar and consult IRS Publication 505, “Tax Withholding and Estimated Tax,” or a qualified tax professional to ensure you are meeting all your specific obligations.

Estimated Taxes and Underpayment Penalties

Many taxpayers find themselves in the position of needing to make estimated tax payments throughout the year. This applies particularly to freelancers, gig workers, small business owners, and individuals with significant investment income. The IRS operates on a pay-as-you-go system, meaning taxes should be paid as income is earned. If you don’t pay enough tax throughout the year through withholding or estimated payments, you could face an underpayment penalty.

To avoid this, taxpayers generally need to pay at least 90% of their current year’s tax liability or 100% of their prior year’s tax liability (110% if your adjusted gross income in the prior year was over $150,000) through a combination of withholding and estimated payments. Regularly reviewing your income and expenses, and adjusting estimated payments accordingly, is a wise financial practice.

What to Do If You Can’t Pay on Time

Life happens, and sometimes, despite best intentions, taxpayers find themselves unable to pay their full tax liability by the deadline. It’s crucial not to panic or, worse, ignore the situation. The IRS encourages communication and offers several options for taxpayers facing financial hardship.

Firstly, always file your return on time, even if you can’t pay. Failing to file can result in a failure-to-file penalty that is significantly higher than the failure-to-pay penalty. Once filed, you can explore options such as:

- Short-Term Payment Plan: You might be granted up to 180 additional days to pay your tax liability in full, though interest and penalties still apply.

- Offer in Compromise (OIC): This allows certain taxpayers to settle their tax debt for a lower amount than what they originally owed if they meet specific eligibility criteria, typically demonstrating significant financial difficulty.

- Installment Agreement: If you can’t pay within the short-term window, an installment agreement allows you to make monthly payments for up to 72 months. While interest and penalties continue to accrue, they might be reduced once an agreement is in place.

Proactive engagement with the IRS is key. Ignoring a tax debt will only compound interest and penalties over time.

Navigating the IRS’s Electronic Payment Options

In today’s digital age, the IRS has significantly expanded and streamlined its electronic payment methods, making it easier and often more secure for taxpayers to fulfill their obligations. These options are generally the fastest, most convenient, and provide immediate confirmation of payment.

IRS Direct Pay: The Easiest Option

IRS Direct Pay is arguably the most straightforward way for individuals to pay their federal taxes directly from their checking or savings account. It’s free, secure, and available 24/7. You can pay your income tax, estimated tax, or other tax bills in minutes without pre-registration. All you need is your bank account number and routing number, along with some personal identifying information to verify your identity. This method offers immediate email confirmation of your payment submission, providing peace of mind.

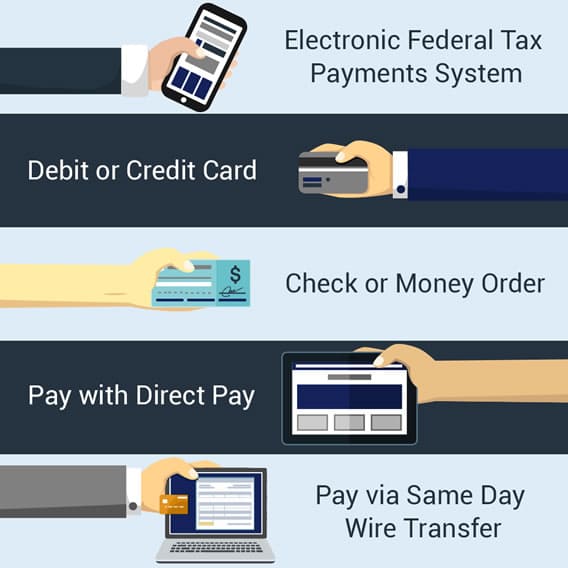

Electronic Federal Tax Payment System (EFTPS): For Businesses and Frequent Payers

The Electronic Federal Tax Payment System (EFTPS) is the ideal choice for businesses, payroll service providers, and individual taxpayers who make recurring tax payments. Unlike Direct Pay, EFTPS requires pre-enrollment, which can take several business days to complete. Once enrolled, however, you can schedule payments up to 365 days in advance and review your payment history for up to 15 months. This system is particularly beneficial for businesses that need to make various types of federal tax payments, including payroll taxes, corporate income taxes, and excise taxes, providing a robust tracking and management tool.

Paying by Debit Card, Credit Card, or Digital Wallet

For those who prefer the convenience of plastic or digital solutions, the IRS allows payments via debit cards, credit cards, and digital wallets through third-party payment processors. While these methods offer flexibility and may allow you to earn rewards points on your card, be aware that the processors charge a convenience fee. This fee varies by processor and card type, so it’s wise to compare options if you choose this route. The IRS does not receive any portion of these fees. This method can be especially useful for those needing to make a last-minute payment or who prefer to use a credit line to manage cash flow.

Electronic Funds Withdrawal (EFW) during E-filing

When you file your federal tax return electronically, either through tax software or a tax professional, you often have the option to authorize an electronic funds withdrawal (EFW). This allows the IRS to automatically deduct the amount you owe directly from your designated bank account on a specified date (usually the filing deadline). It’s a convenient, secure, and free option that integrates seamlessly with the e-filing process, eliminating the need for a separate payment step.

Traditional Payment Methods

While electronic payments are highly recommended, the IRS still provides traditional avenues for those who prefer them or do not have access to digital banking.

Paying by Check or Money Order

For taxpayers who prefer physical payments, sending a check or money order through the mail remains an option. When paying by check or money order, ensure you follow these critical steps:

- Make your check or money order payable to the “U.S. Treasury.”

- Write your name, address, daytime phone number, Social Security number (SSN) or Employer Identification Number (EIN), tax year, and related tax form number (e.g., “2023 Form 1040”) on the check or money order.

- Do not staple or attach your payment to your tax return.

- Mail your payment with a Form 1040-V (Payment Voucher) to the correct IRS address, which varies depending on your location and the form you are filing. Always check the IRS website or your tax instruction booklet for the correct mailing address to avoid delays.

This method requires careful attention to detail and consideration for postal transit times, especially as deadlines approach.

Paying with Cash (Retail Partners)

Believe it or not, you can even pay your federal taxes with cash. The IRS partners with various retail stores across the country, allowing taxpayers to make cash payments in person. This typically involves an initial online registration process with a third-party payment processor (e.g., PayNearMe or Official Payments) to generate a payment code or barcode. You then take this code to a participating retail location (like 7-Eleven or CVS) and make your payment. There might be a small processing fee for this service, and daily limits can apply. This option is particularly useful for those who deal primarily in cash or lack traditional banking access.

Special Circumstances and Payment Strategies

Beyond the standard payment methods, the IRS offers programs and strategies for managing tax liabilities under specific financial conditions.

Installment Agreements and Offers in Compromise

As mentioned earlier, if you cannot pay your full tax debt immediately, an Installment Agreement allows you to make monthly payments over time. This can be a vital lifeline for taxpayers facing temporary financial strain. An Offer in Compromise (OIC) is a more advanced option, allowing certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owed. An OIC is typically considered when there’s doubt about the taxpayer’s ability to pay, the amount of the tax, or when collecting the full amount would create economic hardship. Both options require careful application and adherence to terms, and it’s often advisable to seek professional tax assistance when pursuing these routes.

Payment Plans for Businesses

Businesses, particularly small and medium-sized enterprises, can also find themselves in situations where immediate full payment of taxes isn’t feasible. The IRS offers similar relief options, including short-term payment plans and installment agreements tailored for business taxes. These plans are critical for businesses to maintain operations while fulfilling their tax obligations without facing severe penalties or business disruption. Understanding these options is a key component of business financial planning and risk management.

Withholding Adjustments for Future Payments

A proactive strategy to avoid tax underpayment in the future is to adjust your tax withholding. If you’re an employee, you can do this by submitting a new Form W-4 to your employer. By increasing your withholding, more tax is taken out of each paycheck, reducing the likelihood of owing a large sum at year-end. For self-employed individuals, regularly reviewing your income and expenses and adjusting your estimated tax payments quarterly can prevent surprises and penalties. The IRS Tax Withholding Estimator tool is an excellent resource for fine-tuning your withholding or estimated payments.

Essential Tips for Seamless IRS Payments

Regardless of the method you choose, a few universal best practices can help ensure your tax payments are handled efficiently and without issues.

Double-Checking Your Information

Accuracy is paramount when making tax payments. Before finalizing any payment, meticulously double-check all details: your Social Security number or EIN, the tax year, the payment amount, and bank account information (if paying electronically). A single digit error can cause significant delays, misapplication of payments, or even lead to penalties. Take the extra moment to verify everything.

Keeping Meticulous Records

For every tax payment you make, maintain thorough records. This includes confirmation numbers for electronic payments, copies of checks (front and back), certified mail receipts for mailed payments, and transaction records for cash payments. These records are invaluable if there’s ever a question about whether a payment was made or correctly applied. Store them securely with your other tax documents for at least three years, or longer if you’ve had specific tax events.

Avoiding Scams and Fraud

Unfortunately, tax season is a prime time for fraudsters. Be vigilant against IRS impersonation scams, which often demand immediate payment via unusual methods like gift cards or wire transfers. The IRS will never demand immediate payment without giving you an opportunity to question or appeal the amount, nor will they typically threaten legal action or arrest for non-payment over the phone. All official communications regarding payments will come through legitimate channels. If you receive a suspicious communication, always verify directly with the IRS through their official website or phone numbers, not through links or numbers provided in the suspicious message.

In conclusion, paying your taxes to the IRS is a critical financial responsibility that doesn’t have to be a source of stress. By understanding your obligations, utilizing the various electronic and traditional payment methods available, and employing smart financial strategies, you can ensure your payments are made accurately, on time, and securely. Proactive planning, meticulous record-keeping, and an awareness of potential scams are your best tools for a smooth tax payment experience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.