Facing a tax bill you can’t immediately pay can be an intimidating prospect, often leading to stress and uncertainty. However, the Internal Revenue Service (IRS) is not an unforgiving entity; it provides several pathways for taxpayers to resolve their outstanding obligations through payment plans. Understanding these options, and the precise steps to secure one, is crucial for anyone navigating tax debt. Proactively addressing your tax liability can prevent more severe penalties, mitigate accumulating interest, and restore peace of mind. This comprehensive guide will walk you through the process of establishing a payment plan with the IRS, offering insights into each available option and how to successfully manage your tax debt.

Understanding Your Tax Debt and the IRS’s Approach

Before delving into the specifics of payment plans, it’s essential to grasp why tax debt might arise and how the IRS typically approaches collection. A clear understanding of these foundational elements empowers taxpayers to make informed decisions.

Why You Might Owe the IRS

Tax debt can originate from various situations, often unintentionally. Common scenarios include under-withholding from paychecks, unexpected income from investments or side hustles not adequately accounted for, or simply miscalculations on tax returns. Life events, such as job loss, medical emergencies, or significant business setbacks, can also leave individuals unable to meet their tax obligations even if their tax liability was correctly assessed. It’s important to remember that owing the IRS is not an uncommon occurrence, and the agency is prepared to work with taxpayers who demonstrate a willingness to comply.

The IRS’s Collection Process and Penalties

Ignoring a tax bill is perhaps the most detrimental action a taxpayer can take. When taxes are not paid on time, the IRS begins a structured collection process. Initially, notices are sent, detailing the amount owed, penalties, and interest. Penalties for failure to pay can be substantial, typically 0.5% of the unpaid taxes for each month or part of a month that the taxes remain unpaid, capped at 25%. Interest also accrues on the unpaid balance, including on penalties, and can change quarterly.

If payment attempts are unsuccessful, the IRS can employ more aggressive collection actions, such as filing a federal tax lien, which is a legal claim against your property, or issuing a levy, which can seize wages, bank accounts, or other assets. These actions can severely impact your credit, financial stability, and overall well-being. Establishing a payment plan is a proactive measure that can often prevent these harsh consequences and demonstrates your commitment to fulfilling your tax responsibilities.

Navigating Your IRS Payment Options

The IRS offers several distinct payment plans and relief options, each tailored to different financial situations. Identifying the most suitable option for your circumstances is key to effectively managing your tax debt.

Installment Agreements (IAs): The Most Common Solution

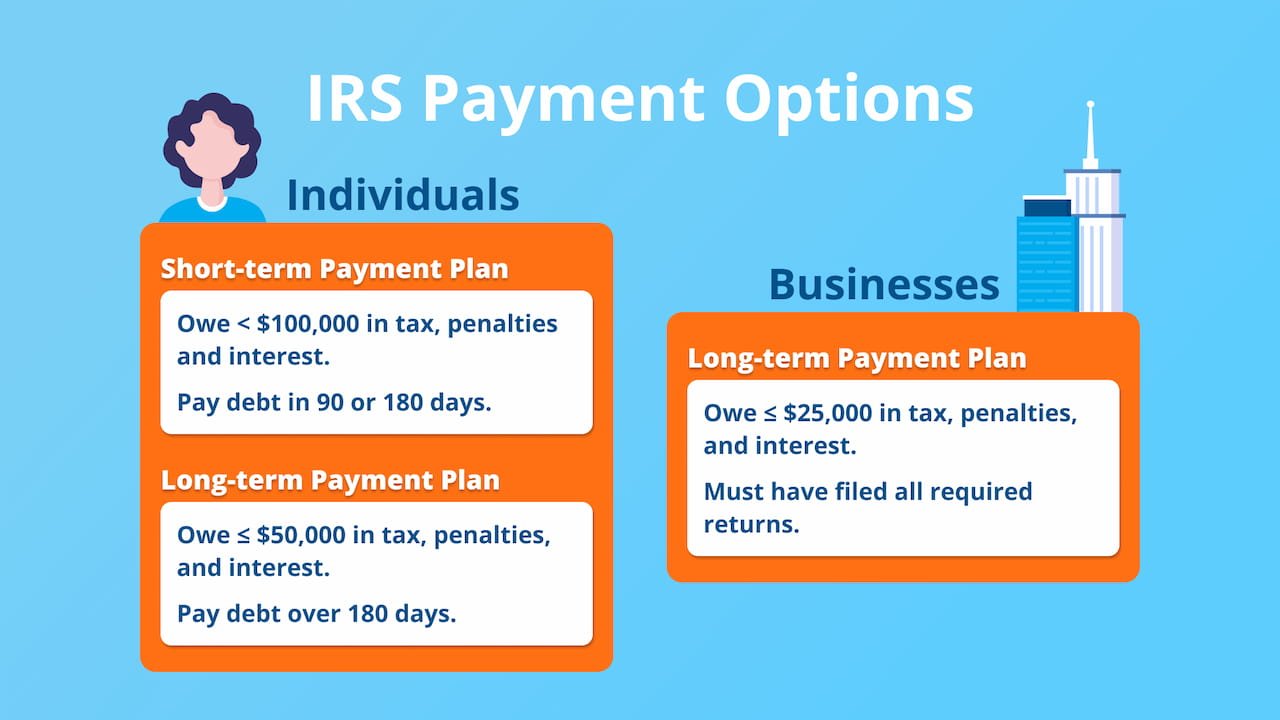

An Installment Agreement (IA) is the most frequently utilized payment plan. It allows taxpayers to make monthly payments for up to 72 months (six years). There are two primary types:

- Short-Term Payment Plans: If you can pay off your tax debt within 180 days, the IRS may grant you a short-term payment plan. While interest and penalties still apply, the setup fee is generally waived. This option is ideal for those who anticipate receiving a lump sum of money in the near future that will cover their tax liability.

- Long-Term Payment Plans (Streamlined Installment Agreement): For those needing more time, a long-term IA, also known as a monthly payment plan, is available. You may qualify for an online payment agreement if you owe a combined total of $50,000 or less (for individuals) or $25,000 or less (for businesses), consisting of tax, penalties, and interest. This allows for a simplified application process and typically incurs a setup fee, which can be reduced for low-income taxpayers. During the agreement, penalties and interest continue to accrue, albeit at a reduced failure-to-pay penalty rate.

Offer in Compromise (OIC): Settling for Less

An Offer in Compromise (OIC) allows certain taxpayers to settle their tax liability with the IRS for a lower amount than what they originally owe. The IRS considers an OIC when there’s doubt as to collectibility (you can’t pay the full amount), doubt as to liability (you believe you don’t actually owe the tax), or when collection would create economic hardship (effective tax administration).

An OIC is a rigorous process, and the IRS will thoroughly evaluate your ability to pay based on your income, expenses, asset equity, and future earning potential. Approval is not guaranteed, and the IRS aims for a settlement amount that maximizes its collection potential without causing undue hardship. While an OIC can offer significant relief, it’s typically a last resort for taxpayers facing severe financial difficulties and requires substantial documentation.

Currently Not Collectible (CNC) Status: A Temporary Reprieve

If the IRS determines that you cannot pay your tax debt due to financial hardship, it may temporarily place your account in “Currently Not Collectible” (CNC) status. This doesn’t forgive the debt; rather, it postpones collection activity. During this period, the IRS will not actively pursue collection, but penalties and interest will continue to accrue.

To qualify for CNC status, you must demonstrate that paying your tax liability would prevent you from meeting basic living expenses like food, housing, and medical care. The IRS will require a detailed financial statement (Form 433-F, Collection Information Statement) to assess your ability to pay. CNC status is reviewed periodically, and if your financial situation improves, the IRS may resume collection efforts. It’s a temporary solution for acute financial distress, providing breathing room but not a permanent waiver of debt.

Other Options: Penalty Abatement and Payment Deferral

Beyond formal payment plans, other relief options exist. Taxpayers may be able to request penalty abatement if they can demonstrate reasonable cause for not paying or filing on time (e.g., natural disaster, serious illness). The IRS also has a First Time Abate (FTA) policy for certain penalties if the taxpayer has a clean compliance history for the preceding three tax years.

In very specific, severe hardship cases, the IRS might consider a payment deferral, where the due date is postponed for a short period. This is less common than other options and is usually reserved for immediate, unforeseen circumstances.

The Application Process: Step-by-Step Guidance

Applying for an IRS payment plan requires careful attention to detail and thorough documentation. The process varies slightly depending on the type of plan you seek.

Gathering Necessary Documentation

Regardless of the plan, preparation is paramount. You’ll need accurate financial information at your fingertips, including:

- Proof of income: Pay stubs, bank statements, profit and loss statements if self-employed.

- Proof of expenses: Rent/mortgage statements, utility bills, medical expenses, car payments, food costs.

- Asset information: Bank account balances, investment statements, property deeds.

- Completed tax returns: All past-due tax returns must be filed and up-to-date. The IRS will not approve a payment plan if you have unfiled tax returns.

Having these documents organized will streamline the application process and help you accurately complete any required forms.

Applying for an Installment Agreement (Form 9465 or Online Payment Agreement)

For a long-term Installment Agreement, the easiest method for many individuals is the Online Payment Agreement (OPA) tool on the IRS website. This is available if you owe $50,000 or less (for individuals) or $25,000 or less (for businesses) in combined tax, penalties, and interest. The online application is quick, often provides immediate approval, and typically has a lower setup fee compared to applying by mail.

If you don’t qualify for the OPA or prefer to apply offline, you can submit Form 9465, Installment Agreement Request, with your tax return or separately. For short-term payment plans (up to 180 days), you can usually request this directly by calling the IRS or responding to an IRS notice.

Applying for an Offer in Compromise (Form 656)

Applying for an OIC is a more intensive process. You’ll need to submit Form 656, Offer in Compromise, along with Form 433-A (OIC), Collection Information Statement for Wage Earners and Self-Employed Individuals, or Form 433-B (OIC), Collection Information Statement for Businesses, depending on your situation. These forms require a comprehensive disclosure of your financial condition.

A non-refundable application fee is usually required (though waived for low-income taxpayers), and you’ll typically need to make an initial payment (if proposing a lump sum offer) or your first proposed monthly payment (if proposing a periodic payment offer) while the OIC is being considered. The IRS will conduct a thorough review of your finances to determine if your offer represents the maximum amount you can reasonably pay.

What to Expect After Application Submission

After submitting your application, the IRS will review your information. For Installment Agreements submitted online, approval is often immediate. For Form 9465, you typically receive a response within 30 days. OIC applications, due to their complexity, can take several months to process.

During the review period, it’s crucial to continue making any required payments and to respond promptly to any additional information requests from the IRS. If your application is denied, the IRS will send a letter explaining the reasons and outlining your appeal rights. You may have the opportunity to appeal the decision or pursue a different payment option.

Maintaining Your Agreement and Avoiding Future Issues

Securing a payment plan is a significant step, but maintaining compliance is equally critical to successfully resolving your tax debt.

Adhering to Payment Terms

Once an agreement is in place, it is paramount to make all payments on time and in full. Setting up direct debit from your bank account is often the most reliable way to ensure timely payments for an Installment Agreement. Failure to make payments or missing even one payment can lead to a default on your agreement.

The Impact of Future Non-Compliance

Defaulting on a payment plan carries serious consequences. The IRS can terminate the agreement and resume aggressive collection actions, including liens and levies. The full amount of the original tax debt, plus all accrued penalties and interest, becomes immediately due. Additionally, you may lose the opportunity to enter into another payment plan for a period of time, making your financial situation even more precarious.

Seeking Professional Assistance

Navigating IRS payment plans can be complex, especially with Offer in Compromise applications or if your financial situation is particularly challenging. A qualified tax professional, such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA), can provide invaluable assistance. They can help you:

- Understand which payment option is best for your situation.

- Prepare and submit all necessary forms and documentation accurately.

- Communicate with the IRS on your behalf.

- Negotiate the terms of an agreement.

- Represent you in appeals if an application is denied.

Their expertise can save you time, reduce stress, and potentially secure a more favorable outcome.

Strategies for Future Tax Planning

The best way to avoid future tax debt is through diligent tax planning. This includes:

- Adjusting W-4 withholding: Review your W-4 annually, especially after major life changes, to ensure the correct amount of tax is withheld from your paycheck.

- Making estimated tax payments: If you’re self-employed or have significant income not subject to withholding, make quarterly estimated tax payments to avoid underpayment penalties.

- Saving for taxes: If you anticipate owing money, set aside funds throughout the year in a dedicated savings account.

- Maintaining accurate records: Keep meticulous records of all income and expenses to ensure accurate tax preparation.

Facing tax debt can be daunting, but the IRS provides structured solutions for taxpayers committed to resolving their obligations. By understanding your options, carefully preparing your application, and diligently adhering to the terms of your agreement, you can effectively manage your tax debt and pave the way for a more stable financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.