Investing in an Individual Retirement Account (IRA) is a cornerstone of a robust retirement strategy for millions. Far more than just a savings account, an IRA is a powerful tax-advantaged investment vehicle designed to help individuals accumulate wealth for their later years. However, the mere act of opening an IRA is only the first step; the real magic happens when you strategically invest the funds within it. This comprehensive guide will demystify the process, offering insights into how to effectively invest your IRA for optimal long-term growth and a secure financial future.

Understanding Your IRA: The Foundation of Retirement Savings

Before diving into investment strategies, it’s crucial to grasp the fundamental nature of an IRA and the various types available, as each carries distinct implications for how and when you can benefit from your investments.

What is an IRA? Defining the Basics

An IRA is a personal savings plan that offers tax benefits to help you save for retirement. Contributions to an IRA can be invested in a wide range of assets, allowing your money to grow over time, often tax-deferred or tax-free, depending on the account type. Unlike employer-sponsored plans like 401(k)s, IRAs are self-directed, giving you complete control over your investment choices. This autonomy is a double-edged sword: it offers immense flexibility but also places the onus on you to make informed decisions.

Types of IRAs: Traditional vs. Roth vs. SEP vs. SIMPLE

The world of IRAs isn’t monolithic; there are several variations, each with unique tax treatments and eligibility requirements:

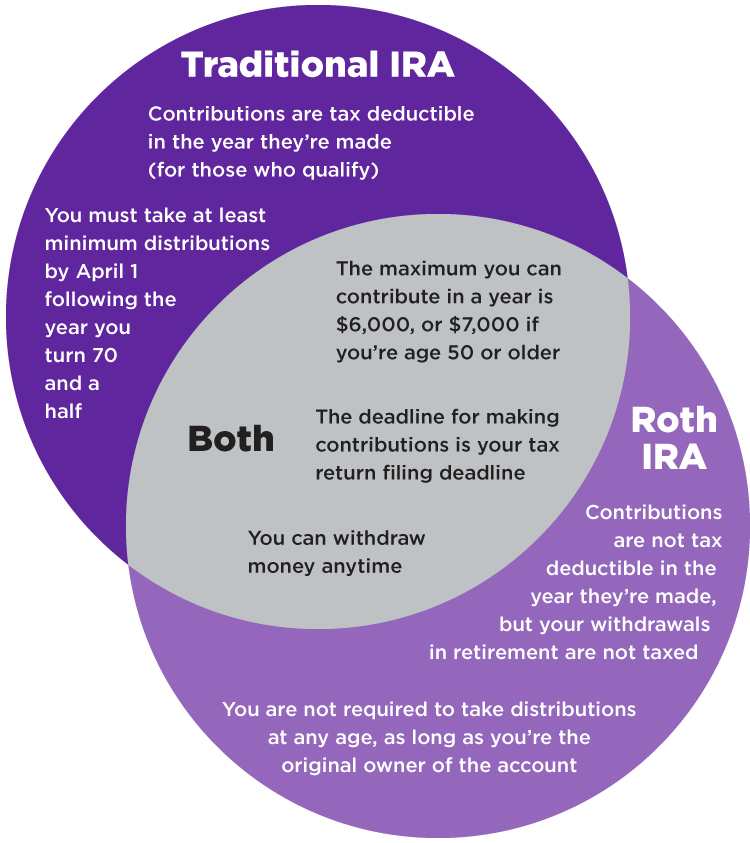

- Traditional IRA: Contributions may be tax-deductible, reducing your taxable income in the year you contribute. Earnings grow tax-deferred, meaning you don’t pay taxes until you withdraw funds in retirement. Withdrawals in retirement are taxed as ordinary income. This is ideal if you expect to be in a lower tax bracket in retirement than you are now.

- Roth IRA: Contributions are made with after-tax dollars, meaning they are not tax-deductible. The significant advantage here is that qualified withdrawals in retirement are entirely tax-free. This option is particularly attractive if you anticipate being in a higher tax bracket in retirement or simply prefer not to worry about taxes on your retirement income. Roth IRAs also have income limitations for direct contributions.

- SEP IRA (Simplified Employee Pension): Primarily for self-employed individuals and small business owners, a SEP IRA allows employers to contribute to their own and their employees’ retirement accounts. Contribution limits are significantly higher than Traditional or Roth IRAs, and contributions are tax-deductible for the employer.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): Another option for small businesses (100 or fewer employees), SIMPLE IRAs are less complex than 401(k)s but still offer both employer and employee contributions. They have lower contribution limits than SEP IRAs but are generally easier to administer.

Understanding which type of IRA aligns best with your current income, tax situation, and future financial goals is the bedrock upon which you build your investment strategy.

Key Benefits of Investing Through an IRA

Regardless of the type, IRAs offer compelling benefits that make them indispensable for retirement planning:

- Tax Advantages: Whether it’s tax-deductible contributions (Traditional), tax-free withdrawals (Roth), or tax-deferred growth, IRAs shield your investments from immediate taxation, allowing more of your money to compound over time.

- Investment Flexibility: Unlike some employer plans with limited investment menus, IRAs generally offer a vast universe of investment options, from individual stocks and bonds to mutual funds, exchange-traded funds (ETFs), and more.

- Compounding Growth: The longer your money remains invested, the more it benefits from compounding interest, where your earnings themselves begin to earn returns. The tax-advantaged nature of IRAs supercharges this effect.

- Portability: IRAs are personal accounts, meaning they move with you regardless of job changes, offering continuity in your retirement savings efforts.

Strategic Asset Allocation: Building a Diversified Portfolio

Once your IRA is established, the critical next step is deciding what to invest in. This isn’t a “set it and forget it” task; it requires thoughtful asset allocation—the process of dividing your investment portfolio among different asset categories.

Assessing Your Risk Tolerance and Time Horizon

Your investment strategy should be highly personalized, beginning with an honest assessment of two key factors:

- Risk Tolerance: How comfortable are you with the potential for your investments to lose value in the short term for the possibility of higher long-term gains? Are you a conservative investor who prioritizes capital preservation, or an aggressive investor willing to accept greater volatility?

- Time Horizon: How many years do you have until you plan to retire and begin withdrawing funds? Generally, younger investors with a longer time horizon can afford to take on more risk, as they have more time to recover from market downturns. Those closer to retirement typically shift towards more conservative investments.

These two factors will dictate the appropriate mix of growth-oriented (e.g., stocks) versus income-oriented or preservation-oriented (e.g., bonds, cash equivalents) assets in your IRA.

The Importance of Diversification Across Asset Classes

Diversification is the bedrock of intelligent investing. It involves spreading your investments across various asset classes, industries, and geographies to reduce overall risk. The principle is simple: if one part of your portfolio performs poorly, other parts may perform well, mitigating the impact on your overall returns.

Key areas for diversification include:

- Asset Classes: A mix of stocks (equities), bonds (fixed income), and potentially cash equivalents.

- Geographic Diversification: Investing in both domestic and international markets.

- Industry Diversification: Spreading investments across different sectors (e.g., technology, healthcare, consumer staples).

- Company Size: A mix of large-cap, mid-cap, and small-cap companies.

Common Investment Options for IRAs: Stocks, Bonds, Mutual Funds, ETFs

IRAs offer a wide array of investment choices to facilitate diversification:

- Stocks: Represent ownership stakes in individual companies. They offer the highest potential for long-term growth but also carry the most volatility. Investing in individual stocks requires significant research and a high degree of confidence in specific companies.

- Bonds: Essentially loans made to governments or corporations. They are generally less volatile than stocks and provide regular interest payments, making them suitable for income and capital preservation. However, their returns are typically lower than stocks.

- Mutual Funds: Professionally managed portfolios that pool money from many investors to invest in a diversified collection of stocks, bonds, or other securities. They offer instant diversification and professional management but typically come with expense ratios (fees).

- Exchange-Traded Funds (ETFs): Similar to mutual funds in that they hold a basket of securities, but they trade like individual stocks on an exchange throughout the day. ETFs often have lower expense ratios than actively managed mutual funds and can be a very cost-effective way to achieve diversification. Index ETFs, which track specific market indices like the S&P 500, are particularly popular for their low costs and broad market exposure.

Considering Alternative Investments (with caution)

While less common for the average investor, some IRA custodians allow for “self-directed IRAs” which can hold alternative assets like real estate, precious metals, or private equity. These can offer unique diversification benefits but typically come with higher fees, increased complexity, and often less liquidity. For most investors, sticking to traditional publicly traded securities within a standard IRA is more advisable due to simplicity and lower costs.

Investment Strategies for Long-Term Growth

Successful IRA investing is less about timing the market and more about consistent, disciplined application of proven long-term strategies.

Dollar-Cost Averaging: Mitigating Volatility

Dollar-cost averaging is a strategy where you invest a fixed amount of money at regular intervals (e.g., $200 every month) regardless of the asset’s price. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more shares. Over time, this averages out your purchase price, reduces the impact of market volatility, and prevents you from trying (and likely failing) to time the market’s ups and downs. This disciplined approach is particularly effective for consistent IRA contributions.

Rebalancing Your Portfolio: Maintaining Your Strategy

Over time, the market performance of your different asset classes will cause your portfolio’s original allocation to drift. For example, a strong bull market might cause your stock allocation to grow beyond its intended percentage. Rebalancing involves periodically adjusting your portfolio back to your target asset allocation. This typically means selling some of your outperforming assets and buying more of your underperforming ones. Rebalancing helps you manage risk, ensures your portfolio remains aligned with your risk tolerance, and encourages selling high and buying low—a valuable discipline.

The Power of Compounding: Starting Early and Staying Consistent

Compounding is often called the “eighth wonder of the world,” and it’s the most powerful force in long-term investing. It refers to the process where the returns you earn on your investments also start earning returns. The earlier you start investing in your IRA and the more consistently you contribute, the more time compounding has to work its magic. Even small, regular contributions can grow into substantial sums over decades due to this exponential growth.

Tax-Efficient Investing within Your IRA

One of the primary benefits of an IRA is its tax efficiency. For a Traditional IRA, you get a tax deduction upfront, and growth is tax-deferred. For a Roth IRA, growth and qualified withdrawals are tax-free. To maximize this, avoid unnecessary trading that incurs short-term capital gains, which would be subject to ordinary income rates if your investments were outside an IRA. Inside an IRA, you’re shielded from annual capital gains taxes, allowing your investments to grow unimpeded.

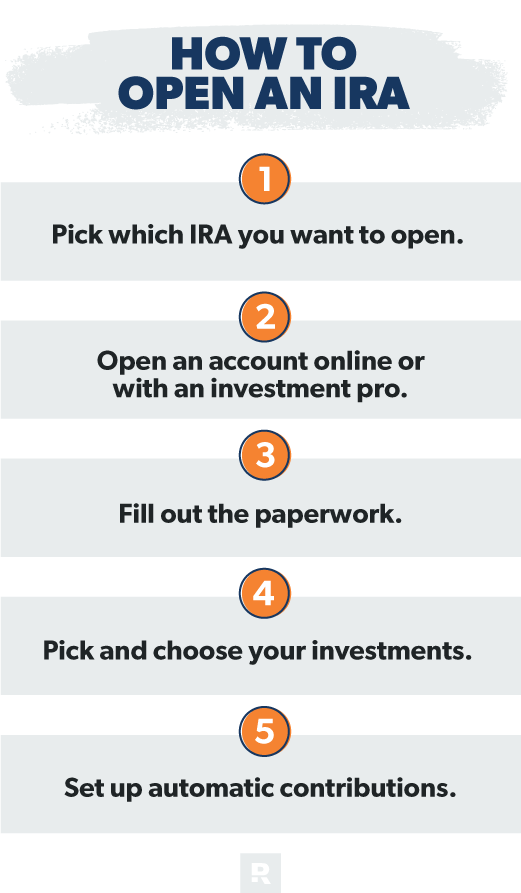

Choosing the Right Investment Platform and Professional Guidance

The practical implementation of your IRA investment strategy depends heavily on the platform you choose and whether you opt for professional assistance.

Robo-Advisors vs. Traditional Brokerages: Weighing Your Options

- Robo-Advisors: These digital platforms use algorithms to build and manage diversified portfolios based on your risk tolerance and financial goals. They are typically low-cost, easy to use, and excellent for investors who prefer a hands-off approach. Examples include Betterment and Wealthfront. They often invest in low-cost ETFs.

- Traditional Brokerages: Platforms like Fidelity, Vanguard, Charles Schwab, or E*TRADE offer a wide range of investment products and tools, allowing you to build and manage your portfolio directly. They cater to both self-directed investors who want full control and those who prefer access to human financial advisors. While offering maximum flexibility, they require more active decision-making.

Evaluating Fees and Expense Ratios

Fees can significantly erode your investment returns over time. Pay close attention to:

- Account Maintenance Fees: Some custodians charge annual fees for IRAs, though many waive them if you meet certain asset thresholds.

- Trading Commissions: Fees charged for buying or selling individual stocks or ETFs. Many brokerages now offer commission-free trading for most ETFs and stocks.

- Expense Ratios of Funds: The annual fee charged by mutual funds and ETFs, expressed as a percentage of your investment. Opt for low-cost index funds or ETFs whenever possible, as even a seemingly small difference in expense ratios can amount to tens of thousands of dollars over decades.

When to Seek Financial Advisor Support

While self-directed investing is increasingly accessible, there are times when a qualified financial advisor can be invaluable. If you have a complex financial situation, lack the time or confidence to manage your investments, or simply want a second opinion, a fee-only fiduciary advisor can help you develop a personalized investment plan, select appropriate investments, and ensure your IRA aligns with your broader financial goals. Always ensure your advisor operates under a fiduciary standard, meaning they are legally obligated to act in your best interest.

Monitoring and Adjusting Your IRA Investments

Your IRA strategy shouldn’t be static. Life changes, market conditions evolve, and your risk tolerance might shift over time. Periodically (e.g., annually or semi-annually), review your portfolio’s performance, rebalance as needed, and ensure your investments still align with your goals and risk profile. This continuous monitoring and adjustment are crucial for long-term success.

Navigating Distributions and Retirement Planning

Investing in your IRA is about more than just accumulation; it’s also about understanding how and when you’ll access those funds in retirement.

Understanding RMDs (Required Minimum Distributions)

For Traditional, SEP, and SIMPLE IRAs, the IRS mandates that you begin taking Required Minimum Distributions (RMDs) once you reach a certain age (currently 73, though subject to change by legislation). These distributions are taxable income. Failure to take RMDs can result in steep penalties. Roth IRAs, thankfully, do not have RMDs for the original owner.

Early Withdrawal Penalties and Exceptions

Withdrawing funds from your IRA before age 59½ typically incurs a 10% early withdrawal penalty, in addition to any ordinary income taxes (for Traditional IRAs). However, there are several exceptions, such as withdrawals for qualified higher education expenses, first-time home purchases (up to $10,000), unreimbursed medical expenses, or if you become totally and permanently disabled. It’s crucial to understand these rules to avoid unintended penalties.

Integrating Your IRA into Your Overall Retirement Plan

Your IRA is just one piece of your broader retirement puzzle. It should be considered alongside other retirement accounts (401(k), 403(b)), taxable investment accounts, Social Security benefits, and any other income streams. A holistic approach ensures that your IRA investments complement your other assets and contribute effectively to your desired retirement lifestyle.

In conclusion, investing your IRA is a critical component of building a secure and comfortable retirement. By understanding the different IRA types, strategically allocating your assets, employing smart long-term investment strategies, choosing appropriate platforms, and periodically reviewing your progress, you can harness the power of tax-advantaged growth to achieve your financial aspirations. Start early, stay disciplined, and watch your retirement nest egg flourish.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.