The journey toward financial independence is rarely a sprint; it is a disciplined marathon fueled by strategic decision-making and the utilization of the right financial vehicles. Among the various tools available to the modern investor, few are as potent or as mathematically advantageous as the Roth IRA. Named after Senator William Roth, this individual retirement account has revolutionized the way Americans save for the future by shifting the tax burden from the end of the journey to the beginning.

Investing in a Roth IRA is more than just opening a bank account; it is a strategic move to shield your future wealth from the uncertainties of rising tax rates. By contributing after-tax dollars today, you effectively “lock in” your current tax rate in exchange for a lifetime of tax-free growth and tax-free withdrawals in retirement. This guide provides an exhaustive roadmap on how to navigate the complexities of the Roth IRA, from initial eligibility to advanced portfolio construction.

Understanding the Fundamentals of a Roth IRA

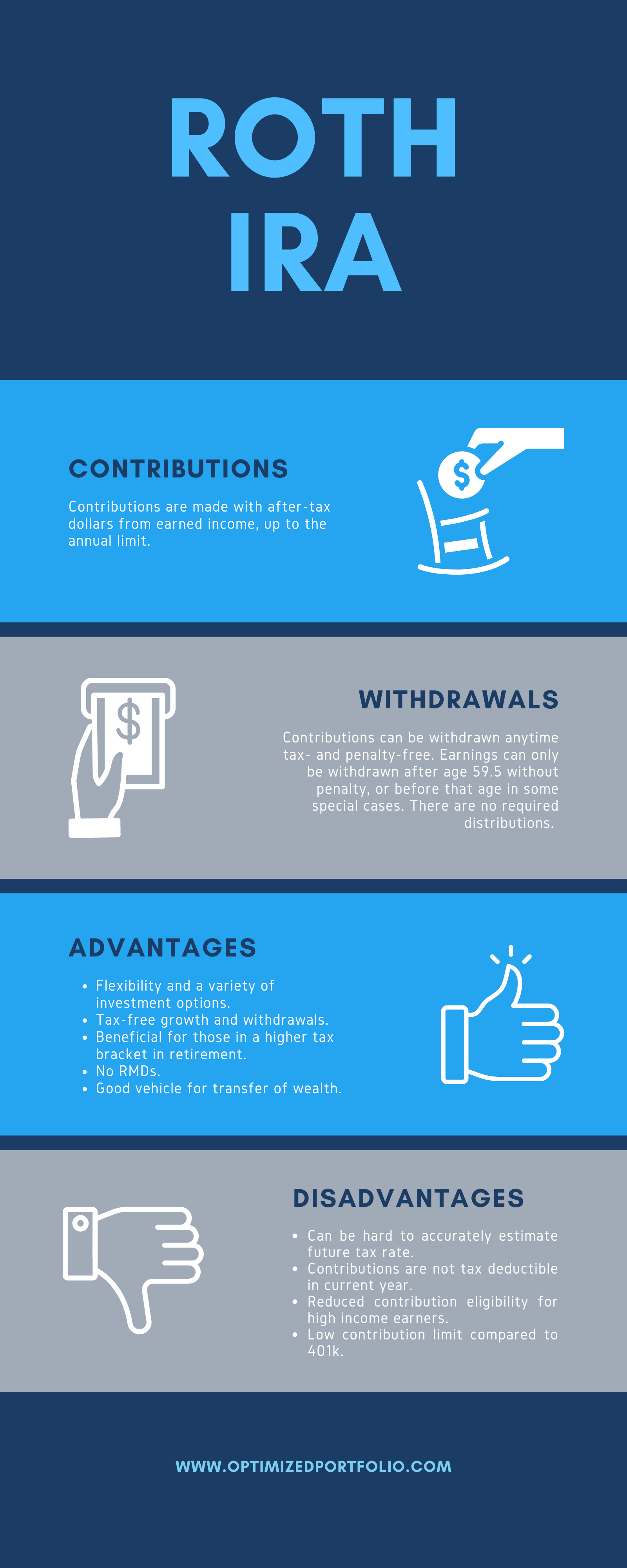

Before depositing a single dollar, it is crucial to understand the structural mechanics of a Roth IRA and how it differs from other retirement accounts. Unlike a Traditional IRA or a 401(k), where you receive a tax deduction upfront, the Roth IRA offers no immediate tax break. Instead, its power lies in the back end.

What Makes a Roth IRA Unique?

The primary differentiator of the Roth IRA is its “tax-free” status rather than “tax-deferred.” In a Traditional IRA, your investments grow, but you owe ordinary income tax on every dollar you withdraw in retirement. In a Roth IRA, as long as you follow the distribution rules, the IRS cannot touch your capital gains, dividends, or interest. This makes the Roth IRA particularly attractive for younger investors who expect to be in a higher tax bracket later in life or for those who believe that national tax rates will inevitably rise in the coming decades.

Eligibility and Income Limits

The IRS imposes strict limitations on who can contribute directly to a Roth IRA based on their Modified Adjusted Gross Income (MAGI). For 2024, the phase-out range for single filers is between $146,000 and $161,000. For married couples filing jointly, the range is $230,000 to $240,000. If your income exceeds these thresholds, your ability to contribute directly is reduced or eliminated. Understanding these boundaries is the first step in determining if the Roth IRA is the right fit for your current financial profile.

Contribution Limits and Deadlines

For the 2024 tax year, the maximum contribution limit is $7,000 for those under age 50, and $8,000 for those 50 and older (which includes a $1,000 “catch-up” contribution). One of the most flexible aspects of the Roth IRA is the contribution timeline. You have until the tax filing deadline—usually April 15th of the following year—to make contributions for the previous year. This allows investors to assess their total annual income before finalizing their investment strategy.

Step-by-Step Guide to Opening Your Account

Once you have determined your eligibility, the physical process of opening a Roth IRA is relatively straightforward, yet it requires careful selection of a custodian. The “custodian” is the financial institution that holds your assets and ensures they meet IRS regulations.

Choosing the Right Brokerage

Not all brokerages are created equal. When selecting where to house your Roth IRA, consider three main factors: fees, investment options, and user experience.

- Discount Brokerages: Firms like Charles Schwab, Fidelity, and Vanguard are industry leaders known for low-to-zero commissions and a vast array of low-cost index funds.

- Robo-Advisors: Platforms like Betterment or Wealthfront are ideal for “hands-off” investors. They use algorithms to manage your asset allocation for a small annual fee.

- Fintech Apps: Newer entries like Robinhood or M1 Finance offer streamlined mobile experiences, though they may lack the deep research tools of traditional firms.

The Application and Onboarding Process

Opening the account typically takes less than 15 minutes online. You will need your Social Security number, employment information, and bank account details for funding. During this process, you will also be asked to designate beneficiaries. This is a critical step in estate planning, as Roth IRAs are excellent vehicles for transferring wealth to heirs due to their tax-free nature.

Funding Your Account

After the account is open, you must move money into it. This can be done via a one-time electronic transfer or by setting up recurring contributions. Many financial advisors recommend “dollar-cost averaging”—the practice of investing a set amount every month (e.g., $583 per month to hit the $7,000 limit). This strategy mitigates the risk of “timing the market” and ensures consistent growth regardless of short-term volatility.

Strategic Asset Allocation within a Roth IRA

A common mistake new investors make is thinking that a Roth IRA is the investment. In reality, a Roth IRA is simply a “bucket.” Once the money is in the bucket, you must choose which assets to purchase. Because the Roth IRA is a tax-advantaged environment, it is the ideal place to hold assets that would otherwise trigger high tax bills.

Low-Cost Index Funds and ETFs

For the majority of investors, the core of a Roth IRA should consist of low-cost, broad-market index funds or Exchange-Traded Funds (ETFs). These funds track indices like the S&P 500 or the Total Stock Market. Because you aren’t taxed on capital gains within the Roth, the frequent rebalancing or dividend payouts of these funds won’t create a “tax drag” on your performance.

Target-Date Funds for Hands-Off Investors

If you prefer not to manage your own asset allocation, Target-Date Funds (TDFs) are a logical choice. You simply select the fund with the year closest to your expected retirement (e.g., Target 2060). The fund automatically shifts from an aggressive, equity-heavy stance to a conservative, bond-heavy stance as you age. This “glide path” ensures that your risk is managed appropriately without requiring daily oversight.

The Role of Individual Stocks and Dividend Investing

Because dividends are 100% tax-free within a Roth IRA, this account is a “gold mine” for dividend growth investors. In a standard brokerage account, you would owe taxes on every dividend check received. Inside a Roth, you can reinvest those dividends to purchase more shares, compounding your wealth at a much faster rate. For those with a higher risk tolerance, the Roth IRA is also an excellent place for high-growth individual stocks, as the massive gains often seen in the tech or biotech sectors will never be subject to capital gains tax.

Advanced Strategies and Rules for Long-Term Success

To truly master the Roth IRA, you must look beyond simple contributions and understand the nuances of the “Backdoor” method and withdrawal regulations.

The Backdoor Roth IRA Strategy

For high earners who exceed the income limits mentioned earlier, the “Backdoor Roth” is a perfectly legal maneuver to get money into a Roth account. It involves contributing to a Traditional IRA (which has no income limits for contributions) and then immediately converting those funds into a Roth IRA. While this requires careful tax reporting (Form 8606), it allows wealthy investors to continue reaping the benefits of tax-free growth despite their high income.

Navigating the Five-Year Rule

While Roth IRA contributions can be withdrawn at any time without penalty (because you already paid taxes on them), the earnings on those contributions are subject to the “Five-Year Rule.” To withdraw earnings tax-free and penalty-free, the account must have been open for at least five years, and you must be at least 59½ years old. There are exceptions for first-time home purchases (up to $10,000) and certain educational expenses, but generally, the Roth is a “look but don’t touch” vehicle until retirement.

Rebalancing and Portfolio Maintenance

Investing in a Roth IRA is not a “set it and forget it” endeavor. At least once a year, you should review your asset allocation. If your stocks have performed exceptionally well, they may now represent a larger percentage of your portfolio than you intended, increasing your risk. Rebalancing involves selling some of the “winners” and buying more of the underperforming assets (like bonds or international stocks) to return to your target allocation. Within a Roth IRA, this selling and buying triggers zero tax consequences, making it the most efficient environment for active portfolio management.

Conclusion: The Path to Financial Freedom

Investing in a Roth IRA is one of the most impactful financial decisions an individual can make. By choosing to pay taxes on the “seed” rather than the “harvest,” you create a sanctuary of wealth that the IRS cannot diminish in your later years. Whether you are a novice investor starting with $50 a month or a high-earner utilizing the backdoor strategy, the principles remain the same: start early, contribute consistently, and choose diversified, low-cost investments.

The ultimate strength of the Roth IRA lies in its flexibility and its protection against future uncertainty. In an era where tax laws are constantly shifting, having a pool of assets that is strictly “hands-off” for the government provides a level of security that few other investments can match. Start your Roth IRA journey today, and let the power of tax-free compounding work in your favor for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.