Securing a small business loan is often the most significant milestone in an entrepreneur’s journey. Whether it is to bridge a seasonal cash flow gap, invest in inventory, or scale operations through a major acquisition, capital is the lifeblood of any commercial enterprise. However, the lending landscape has evolved into a complex ecosystem of traditional institutions, government-backed programs, and digital-first fintech disruptors. Navigating this environment requires more than just a good idea; it requires a deep understanding of financial metrics, lender expectations, and strategic planning.

To successfully secure a loan, a business owner must transition from the role of a visionary to that of a meticulous financial strategist. This guide explores the essential phases of obtaining a small business loan, focusing on the financial foundations and the rigorous preparation needed to win over lenders.

1. Evaluating Your Financial Needs and Loan Varieties

Before approaching a lender, you must determine exactly how much capital you need and what specific type of debt instrument suits your business model. Over-borrowing can lead to unnecessary interest expenses and debt-service strain, while under-borrowing can leave your project incomplete and your cash flow vulnerable.

Identifying the Purpose of the Loan

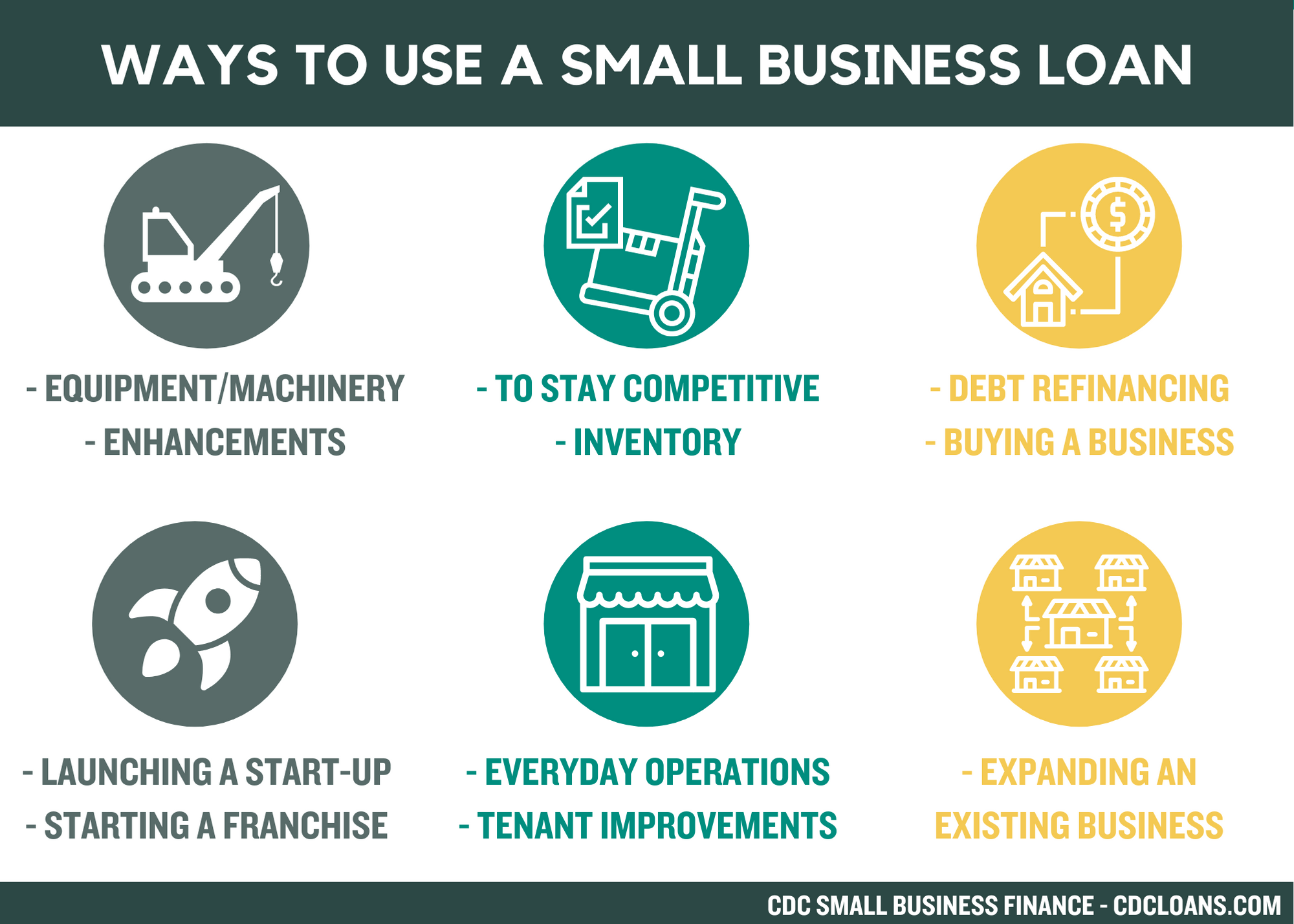

Lenders categorize risk based on how the money will be used. Working capital loans are designed to cover everyday operational expenses, such as payroll and rent, and are typically shorter in duration. In contrast, term loans are often used for long-term investments like purchasing real estate or heavy machinery. By clearly defining the “use of proceeds,” you demonstrate to the lender that you have a calculated plan for generating a return on their investment.

Traditional Term Loans vs. Lines of Credit

A traditional term loan provides a lump sum of cash upfront, which is repaid over a set period with a fixed or variable interest rate. This is ideal for one-time expansions. On the other hand, a business line of credit offers more flexibility. It allows you to draw funds as needed, up to a certain limit, and you only pay interest on the amount you use. This is a vital financial tool for managing the cyclical nature of many industries.

The SBA Loan Advantage

The U.S. Small Business Administration (SBA) does not lend money directly to small businesses. Instead, it provides guarantees to lenders, reducing their risk and making it easier for small businesses to access capital. Programs like the 7(a) and 504 loans offer competitive interest rates and longer repayment terms that are often unavailable through conventional market channels. However, the application process for SBA loans is notably rigorous and requires extensive documentation.

2. The Prerequisites: What Lenders Look For

Lenders use a standardized set of criteria to evaluate the creditworthiness of a business. Understanding the “Five Cs of Credit”—Character, Capacity, Capital, Collateral, and Conditions—is essential for any borrower.

Credit Scores: Personal and Business

For many small business owners, their personal credit history is the primary indicator of financial responsibility. Lenders typically look for a personal credit score of 680 or higher for conventional loans. As your business matures, it is equally important to build a business credit profile through bureaus like Dun & Bradstreet or Experian Business. A strong business credit score can unlock lower interest rates and higher borrowing limits, decoupling your personal finances from your corporate liabilities.

Financial Statements and Debt-Service Coverage Ratio (DSCR)

Lenders will scrutinize your financial health through three key documents: the balance sheet, the income statement (P&L), and the cash flow statement. They are specifically looking for your Debt-Service Coverage Ratio (DSCR), which is your net operating income divided by your total annual debt payments. A DSCR of 1.25 or higher is generally considered healthy, as it indicates the business generates 25% more income than is required to cover its debt obligations.

The Importance of Collateral

Collateral serves as a secondary source of repayment. This can include accounts receivable, inventory, equipment, or real estate. Secured loans, backed by collateral, generally offer more favorable terms. If your business lacks significant physical assets, you may need to look into unsecured loans, though these often come with higher interest rates and may require a personal guarantee, putting your personal assets at risk in the event of a default.

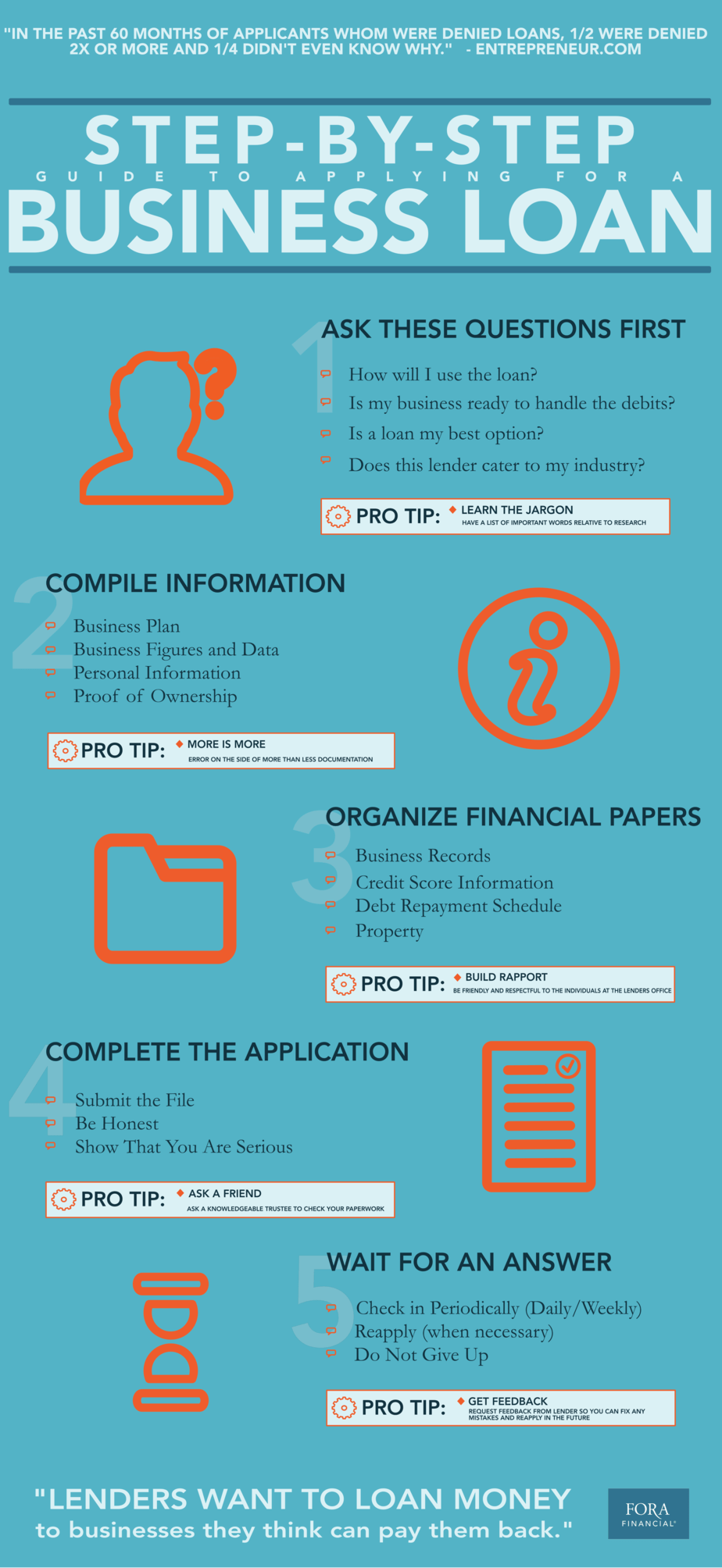

3. Navigating the Application Process

Once you have identified the right loan product and assessed your financial standing, the next phase is the formal application. This stage is where many businesses fail due to a lack of organization or an incomplete narrative.

Choosing the Right Lender

Not all financial institutions are created equal. Large national banks often have the lowest rates but the strictest requirements. Community banks and credit unions may be more willing to work with local businesses and offer a more personalized underwriting process. Alternatively, online lenders and fintech platforms offer speed and convenience, often funding loans within days, though usually at a higher Annual Percentage Rate (APR).

Preparing the Documentation Packet

A professional loan application is comprehensive. You should have at least two to three years of personal and business tax returns ready, along with current year-to-date financial statements. Additionally, you will need legal documents such as your Articles of Incorporation, business licenses, and any existing lease agreements. Presenting these in an organized digital or physical binder signals to the lender that your business is managed with professional rigor.

Crafting a Compelling Business Plan

For new businesses or those seeking significant expansion capital, a formal business plan is non-negotiable. This document should outline your market analysis, competitive advantages, and management team’s experience. Most importantly, it must include detailed financial projections. Your projections should include a “best-case,” “expected,” and “worst-case” scenario to show the lender that you have considered potential market volatility and have a plan to maintain debt payments even during a downturn.

4. Strategic Alternatives and Modern Lending Solutions

In recent years, the “Money” sector has seen a surge in alternative financing options that bypass the traditional banking system. These can be life-savers for businesses that do not fit the conventional lending mold.

Equipment Financing and Invoice Factoring

If your need for capital is tied specifically to assets, equipment financing allows the equipment itself to serve as collateral, often requiring a lower down payment. For businesses struggling with slow-paying clients, invoice factoring allows you to sell your accounts receivable to a third party at a discount. This provides immediate liquidity without taking on traditional debt, though the cost of capital is generally higher than a bank loan.

Merchant Cash Advances (MCA)

An MCA is not technically a loan but an advance against future credit card sales. While these are very easy to obtain and require no collateral, they are among the most expensive ways to borrow money. The “factor rate” can result in an effective APR of 40% to 100% or more. These should generally be viewed as a last resort for short-term emergency cash flow needs.

Revenue-Based Financing

A growing trend in business finance is revenue-based financing, where repayments are tied to a percentage of monthly revenue. During months where sales are high, you pay more; during slow months, your payment drops. This aligns the lender’s interests with the business’s performance and provides a safety net for seasonal businesses, though it requires a high level of transparency regarding your daily sales data.

Conclusion: Sustaining Financial Health Post-Funding

Securing a small business loan is not the end of the process; it is the beginning of a new phase of financial responsibility. Once the funds are in your account, the focus shifts to efficient capital allocation and meticulous debt management.

Successful entrepreneurs treat their loan as a tool for leverage, ensuring that every dollar borrowed generates more than a dollar in value. By maintaining a high DSCR, keeping accurate financial records, and communicating regularly with your lender, you not only ensure the success of your current project but also lay the groundwork for future credit needs. In the world of business finance, your reputation as a reliable borrower is one of your most valuable assets. Proper planning, a clear understanding of the “Money” niche, and a disciplined approach to debt will empower your business to reach its full potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.