The journey toward homeownership is often viewed as a series of emotional milestones: the first time you browse listings online, the moment you walk through an open house that feels “right,” and the day you finally turn the key in the lock. However, before the emotional rewards can be reaped, a rigorous financial foundation must be laid. In the modern real estate market, that foundation begins with getting prequalified for a home loan.

Prequalification serves as the bridge between “just looking” and being a legitimate contender for a property. It provides a baseline of your purchasing power and signals to real estate agents and sellers that you have the financial discipline required to navigate a mortgage. This guide explores the intricacies of the prequalification process, the financial metrics that matter most, and the strategic steps you can take to secure the best possible terms for your future home.

Understanding Prequalification: The Foundation of Your Home Search

Before diving into paperwork, it is essential to understand exactly what prequalification is and—perhaps more importantly—what it is not. In the world of personal finance, terminology matters, and confusing “prequalified” with “pre-approved” can lead to significant hurdles later in the buying process.

What is Prequalification?

Prequalification is an initial assessment of a borrower’s creditworthiness by a lender. It is typically a quick process where you provide a snapshot of your financial health, including your income, assets, and debts. Unlike a formal loan application, prequalification is often based on self-reported data, though many modern lenders will perform a “soft” credit pull to verify your score without impacting it. The result is a non-binding estimate of how much the bank might be willing to lend you.

Prequalification vs. Pre-approval: Knowing the Difference

While the terms are often used interchangeably in casual conversation, they represent different levels of scrutiny.

- Prequalification is an “at-a-glance” look at your finances. It is excellent for determining your price range and discussing different mortgage types with a loan officer.

- Pre-approval is a much more rigorous process. It involves a “hard” credit pull and the official verification of your financial documents (tax returns, W-2s, and bank statements). A pre-approval letter is essentially a conditional commitment from the lender to grant you a loan, whereas a prequalification is simply an estimate.

Why Prequalification is Your Competitive Edge

In a competitive real estate market, sellers are wary of offers that might fall through due to financing issues. While not as ironclad as a pre-approval, a prequalification letter shows that you have already initiated a dialogue with a lender. It demonstrates that you are a serious buyer who understands the financial realities of the market, making your offer more attractive than a buyer who has not yet consulted a bank.

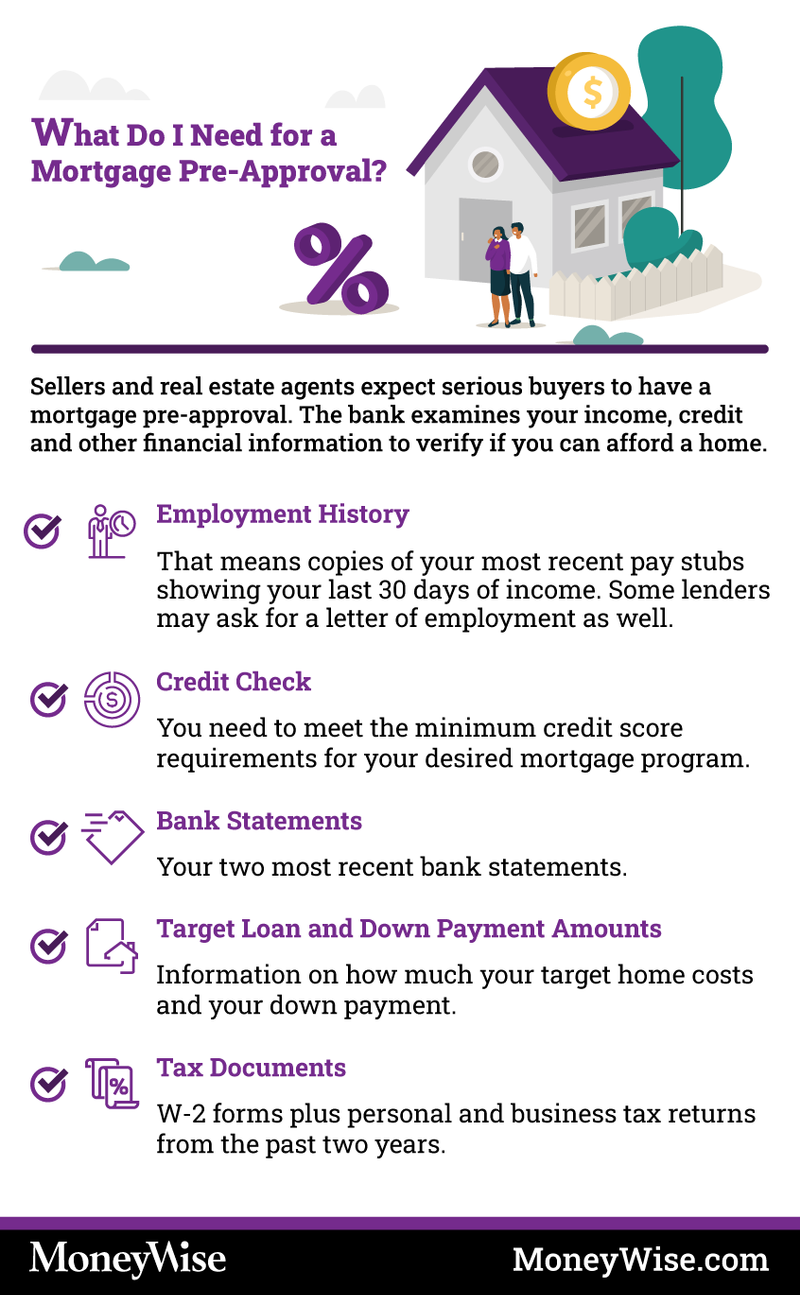

The Essential Checklist: Preparing Your Financial Profile

Lenders look at a specific set of financial indicators to determine how much risk you represent as a borrower. To get prequalified, you need to have a clear understanding of these three pillars: credit, debt, and income.

Assessing Your Credit Score and History

Your credit score is perhaps the most influential factor in your mortgage journey. It determines not only if you qualify for a loan but also the interest rate you will pay. For most conventional loans, a FICO score of 620 is the minimum, but higher scores (740+) unlock the most favorable rates. Before seeking prequalification, check your credit report for errors. Disputing a mistake on your report can lead to a quick score bump that could save you thousands of dollars over the life of a 30-year mortgage.

Calculating Your Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio is a mathematical formula lenders use to measure your ability to manage monthly payments. To calculate it, you divide your total monthly debt payments (student loans, car notes, credit card minimums) by your gross monthly income.

- Front-End Ratio: The percentage of your income that goes toward housing costs.

- Back-End Ratio: The percentage of your income that goes toward all recurring debt.

Lenders typically look for a back-end DTI of 43% or lower, though some programs (like FHA loans) may allow for higher ratios.

Documenting Your Income and Assets

Even in the prequalification stage, you should have your documentation organized. Lenders want to see a stable two-year work history. If you are a W-2 employee, this is straightforward. However, if you are self-employed or a “gig economy” worker, you will need to provide comprehensive tax returns to prove a consistent income stream. Additionally, you should account for your liquid assets—savings accounts, 401(k) balances, and brokerage accounts—as these prove you have the funds for a down payment and closing costs.

The Step-by-Step Process to Getting Prequalified

Once your financial house is in order, the actual process of getting prequalified is relatively swift, often taking anywhere from a few minutes to a couple of days.

Researching and Selecting the Right Lender

Don’t settle for the first bank you see. Personal finance is about shopping for the best value. Compare national banks, local credit unions, and online mortgage lenders. Credit unions often offer lower fees and more personalized service, while large national banks might have more diverse loan products. Look for a lender that offers a robust digital platform but also provides access to a responsive loan officer who can answer complex questions.

Submitting Your Application: Online vs. In-Person

Most modern lenders offer an online prequalification portal. You will enter your personal details, employment history, and an estimate of your assets. If you prefer a more hands-on approach, meeting with a loan officer at a local branch can be beneficial, especially if your financial situation is unique (e.g., you own multiple businesses or have complicated investment income). During this stage, be as honest as possible; providing inflated numbers now will only lead to a rejection during the more formal pre-approval or underwriting stages.

Navigating the “Soft” Credit Pull

During prequalification, most lenders will perform a “soft” credit inquiry. This allows them to see your credit score and high-level debt information without leaving a “ding” on your credit report. This is a significant advantage, as it allows you to get prequalified with multiple lenders to compare potential rates without damaging the very score you are relying on to buy a home.

Strategies to Improve Your Prequalification Odds

If your initial prequalification numbers aren’t what you hoped for, there are several levers you can pull to improve your standing.

Boosting Your Credit Score Before Applying

If you are on the cusp of a better credit tier, consider “rapid rescoring” or simply paying down credit card balances to lower your credit utilization ratio. Ideally, you want your credit card balances to be below 30% of your total limit. Lowering this ratio is often the fastest way to see a meaningful jump in your score within a single billing cycle.

Managing Existing Debt Obligations

If your DTI is too high, focus on paying off small, high-interest debts. Eliminating a $200 monthly car payment or a $50 monthly credit card minimum can significantly increase the amount a lender is willing to give you for a mortgage. In the eyes of a lender, “cash flow is king.” The more of your monthly income that is unencumbered by debt, the more house you can afford.

Saving for a Down Payment and Closing Costs

While some loan programs allow for as little as 3% or 3.5% down (and VA loans offer 0% down), having a larger down payment improves your prequalification terms. A larger “skin in the game” reduces the lender’s risk, which can lead to lower interest rates and the elimination of Private Mortgage Insurance (PMI) if you reach the 20% threshold.

What Happens After You Are Prequalified?

Receiving your prequalification letter is a major milestone, but it is a starting point, not the finish line.

Setting a Realistic Budget Based on Your Letter

Just because a bank says you can borrow $500,000 doesn’t mean you should. Use your prequalification amount as a ceiling, not a target. Factor in the “hidden” costs of homeownership: property taxes, homeowners insurance, maintenance, and utility increases. A professional financial plan ensures that you are “house-rich” rather than “house-poor,” allowing you to continue saving for retirement and other goals while paying your mortgage.

When to Move to the Pre-approval Phase

Once you have found a neighborhood you like and are ready to start making offers, it is time to convert that prequalification into a pre-approval. This is when the lender will verify every piece of data you’ve provided. Having your pre-approval letter in hand when you visit an open house makes you a formidable buyer, ready to move as soon as the right property hits the market.

Maintaining Your Financial Status During the Search

One of the most common mistakes buyers make is changing their financial profile after getting prequalified. Do not open new credit cards, do not buy a new car, and do not quit your job or change careers right before or during the home-buying process. Lenders look for stability. Any major change in your debt or income can invalidate your prequalification and lead to a loan denial at the eleventh hour.

By following these steps and maintaining a disciplined approach to your personal finances, getting prequalified for a home loan becomes a manageable and empowering part of the home-buying journey. It provides the clarity and confidence needed to navigate the complex real estate market and secures your path toward a sound financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.