In the evolving landscape of digital finance, the boundary between traditional banking and online payment processing has blurred. PayPal, once a simple intermediary for eBay transactions, has transformed into a robust financial hub that offers tools comparable to major retail banks. Among its most potent offerings are its physical cards—the PayPal Cashback Mastercard, the PayPal Business Debit Mastercard, and the PayPal Prepaid Mastercard.

For the modern consumer, freelancer, or small business owner, obtaining a PayPal card is more than a matter of convenience; it is a strategic move to streamline cash flow, earn rewards, and integrate digital earnings into the physical economy. This guide provides a deep dive into the financial implications, application processes, and strategic advantages of incorporating a PayPal card into your personal or business finance toolkit.

Understanding the PayPal Card Ecosystem: Which One Suits Your Financial Needs?

Before initiating an application, it is crucial to identify which card aligns with your specific financial goals. PayPal offers several distinct products, each catering to different spending habits and income structures.

The PayPal Cashback Mastercard

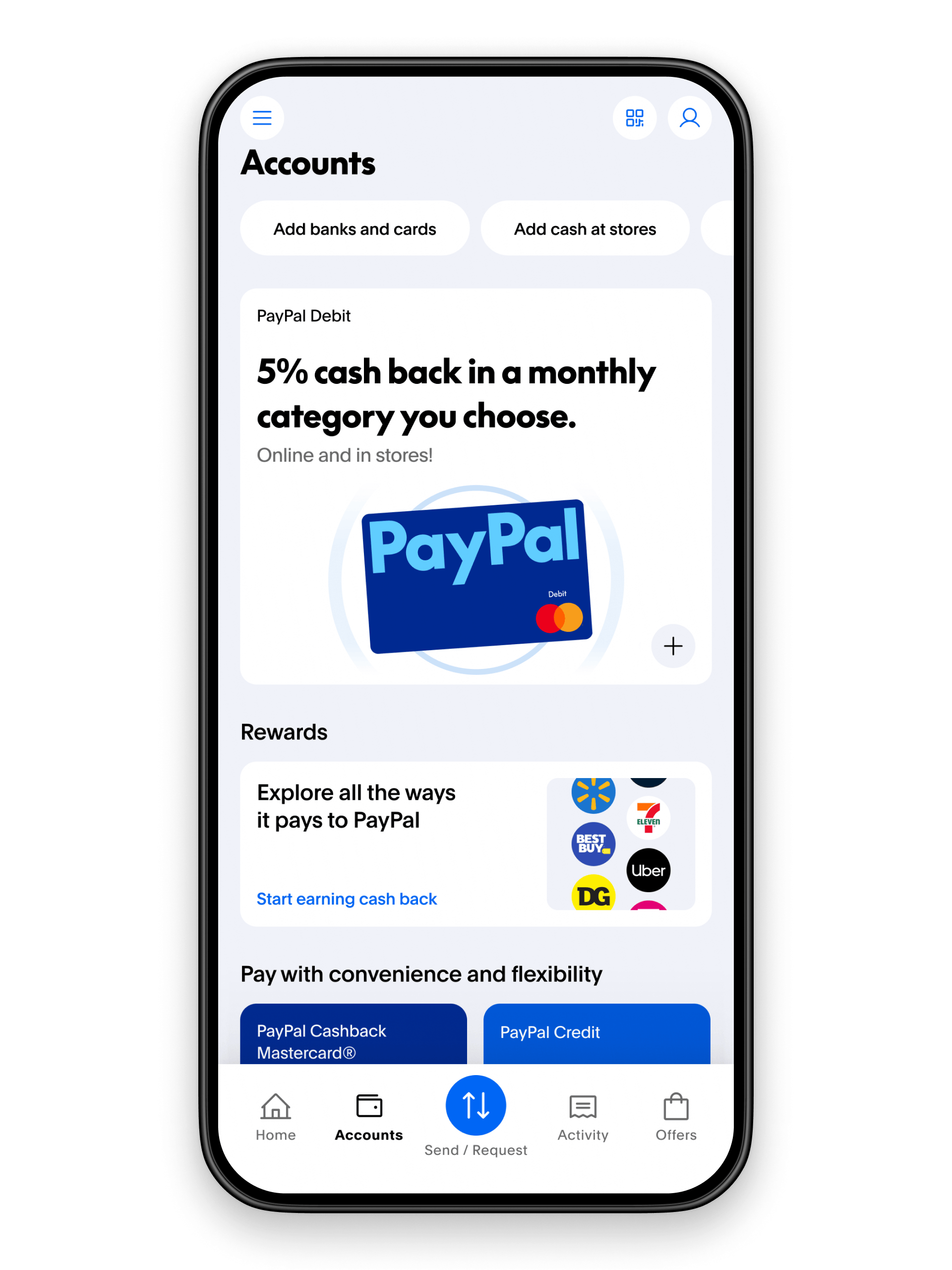

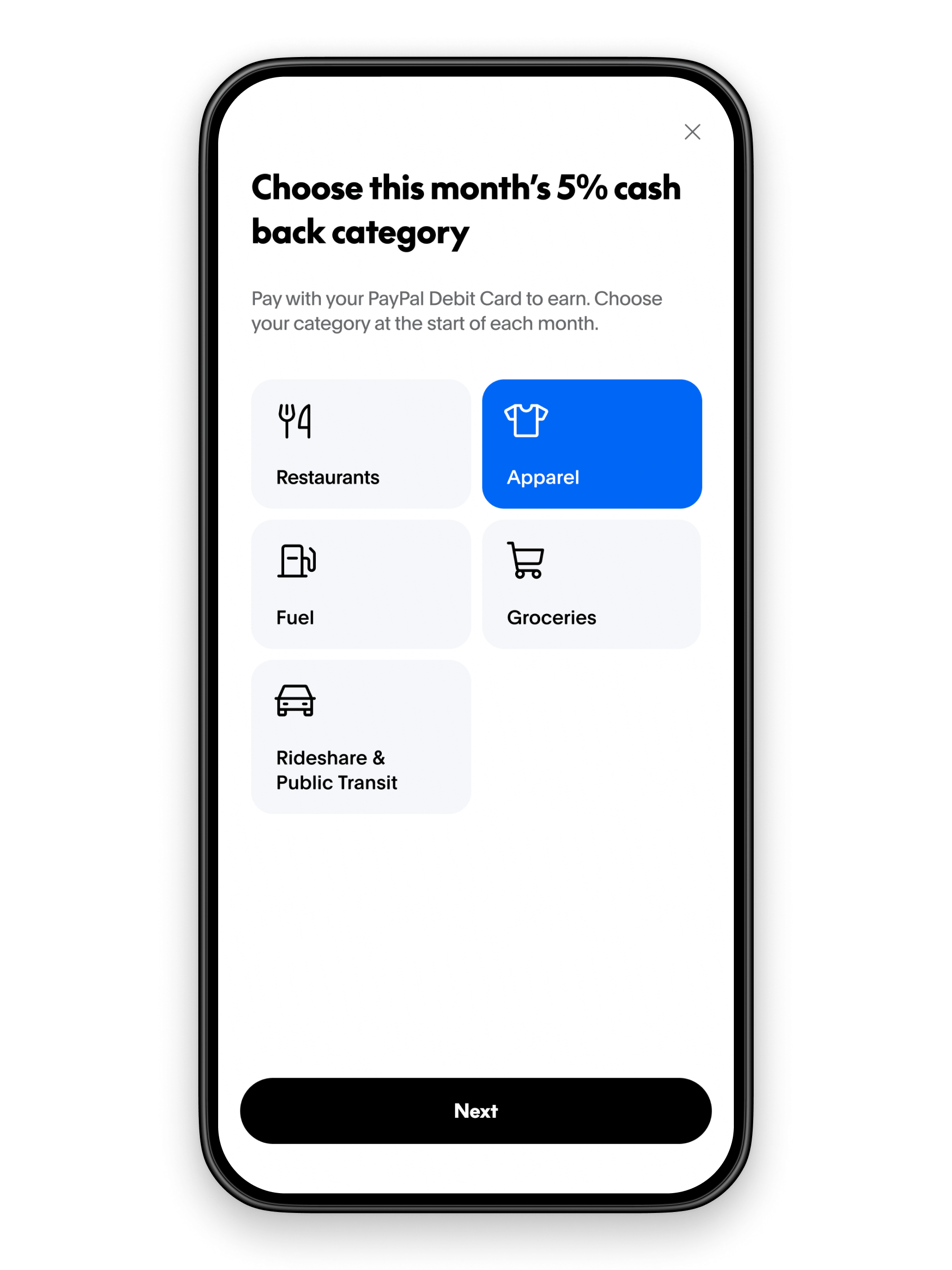

This is a traditional credit card designed for individuals looking to maximize their personal finance rewards. Unlike many entry-level credit cards, this option often provides a high percentage of cashback on all purchases, with an even higher tier for purchases made through the PayPal checkout. From a financial planning perspective, this card is ideal for those who have a solid credit history and wish to consolidate their spending to earn passive income through rewards.

The PayPal Business Debit Mastercard

Designed specifically for entrepreneurs and gig workers, this card links directly to a PayPal Business account. Its primary financial utility is “instant liquidity.” When a client pays you via PayPal, the funds are immediately accessible via the debit card at point-of-sale terminals or ATMs. This eliminates the 1–3 day waiting period for standard bank transfers, which is a critical advantage for managing small business cash flow.

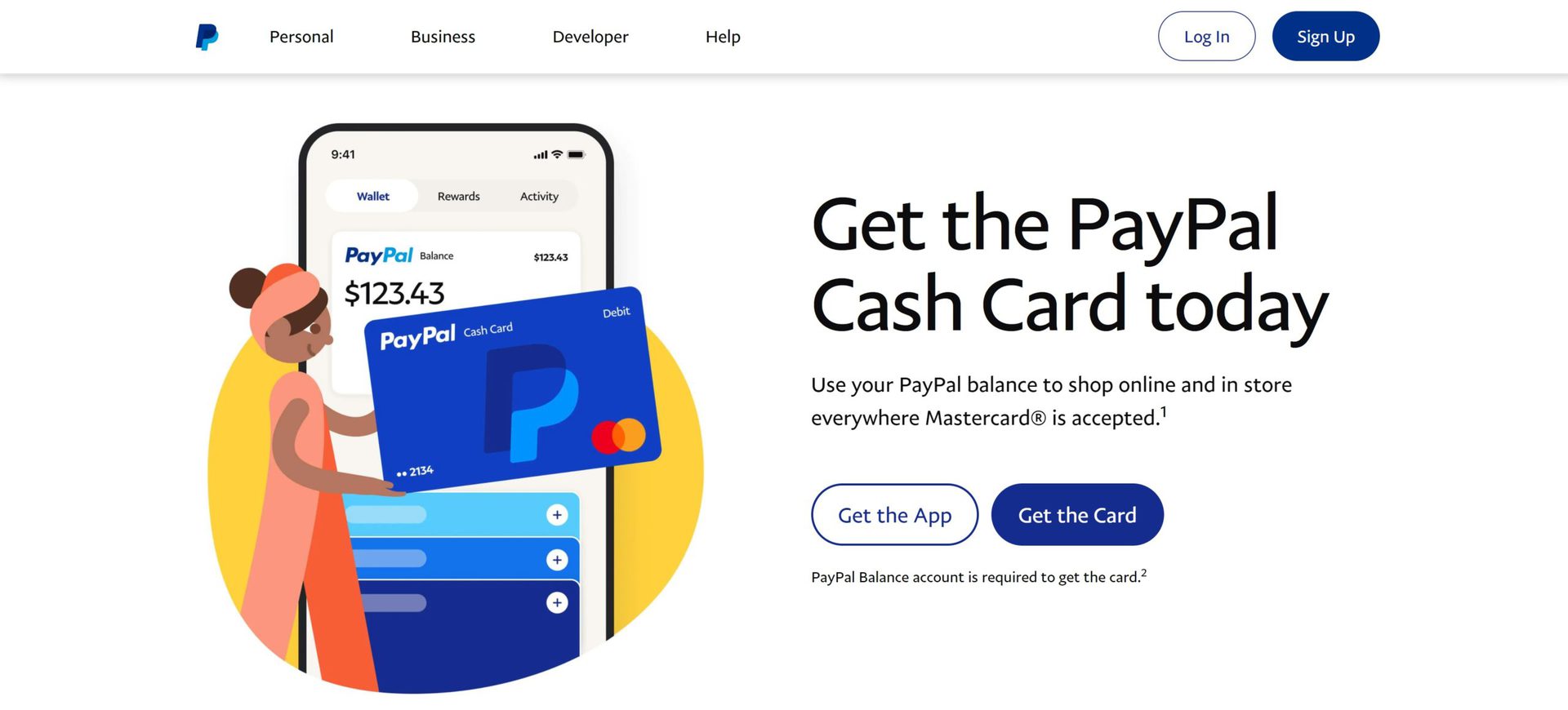

The PayPal Prepaid Mastercard

The prepaid option serves as a bridge for those who prefer not to use credit or who want to maintain a strict “envelope-style” budgeting system. You transfer a set amount of money from your PayPal balance to the card, ensuring that you cannot overspend. It is a disciplined tool for those focusing on debt reduction or strict discretionary spending limits.

The Step-by-Step Acquisition Process: From Application to Activation

The process of obtaining a PayPal card is digital-first, emphasizing efficiency and verification. However, because these are financial instruments, the requirements are rigorous to ensure compliance with global “Know Your Customer” (KYC) and Anti-Money Laundering (AML) regulations.

Pre-requisites for Application

Before you can apply for any card, your PayPal account must be in good standing. This involves:

- Identity Verification: You must provide a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Account Confirmation: Your email and phone number must be verified.

- Linked Funding Source: While not always mandatory for the debit version, having a confirmed bank account or external credit card linked to your profile increases your internal “trust score” within the PayPal algorithm.

Navigating the Application Portal

To apply, navigate to the “Money” or “Wallet” section of your PayPal dashboard. For the Cashback Mastercard, the process involves a hard credit inquiry, which may impact your credit score temporarily. The Business Debit card, conversely, generally does not require a hard credit check but does require you to have a “Business” account profile, which can be toggled in your settings if you are currently a “Personal” user.

Activation and Virtual Card Access

Upon approval, PayPal often provides a virtual version of the card within the app. From a financial management standpoint, this is a significant benefit, allowing you to begin using the line of credit or your balance for online bill payments immediately while the physical card is in transit (usually 7–10 business days).

Maximizing Your Personal Finance Strategy with PayPal Cards

Simply owning the card is the first step; the second is integrating it into a broader wealth-management strategy. Using these cards effectively requires an understanding of interest rates, reward tiers, and fee structures.

Optimizing Cashback and Rewards

The Cashback Mastercard is a powerful tool for those who practice “credit card laddering.” By using the card for fixed expenses—such as utility bills, groceries, and insurance—and then paying the balance in full each month, you effectively receive a 2% to 3% discount on the cost of living. This “found money” can then be redirected into a high-yield savings account or a brokerage account to fuel long-term investment goals.

Fee Mitigation and ATM Strategy

For debit and prepaid users, the primary financial drain comes from ATM fees and foreign transaction fees. To optimize your money, it is vital to use “In-Network” ATMs. PayPal’s partnership with networks like MoneyPass allows for surcharge-free withdrawals. Understanding these geographic and network limitations ensures that your hard-earned money stays in your pocket rather than being eroded by micro-transactions.

Budgeting via Sub-Accounts

The PayPal Prepaid card allows for the creation of a “Savings Account” through a partner bank (such as Pathward, N.A.). This allows users to move money out of their main spending balance into a protected space, often earning a competitive APY (Annual Percentage Yield). This feature transforms a simple payment card into a comprehensive tool for short-term emergency fund building.

Business and Side Hustle Optimization: Using the PayPal Business Debit Mastercard

For the freelancer or small business owner, the PayPal Business Debit Mastercard is more than a payment tool; it is a simplified accounting system.

Separating Personal and Business Expenses

One of the cardinal rules of business finance is the separation of entities. Using a PayPal card exclusively for business purchases—software subscriptions, inventory, or marketing ads—creates a clean paper trail for tax season. This reduces the administrative burden of sorting through personal bank statements to find deductible business expenses.

Instant Access to Earnings and “Back-Up” Funding

A unique financial feature of the PayPal Business Debit card is “Back-up Funding.” If your PayPal balance is zero, the card can automatically pull funds from a linked bank account to complete a transaction. This ensures that business operations are never interrupted due to timing issues with client payments. However, a savvy financial manager must monitor these transfers to avoid potential overdraft fees from the secondary bank.

International Commerce and Exchange Rates

For those working with international clients or vendors, the PayPal card provides a streamlined way to handle multiple currencies. While PayPal’s internal exchange rates include a spread, the convenience of spending directly from a Euro or GBP balance (if held in the account) can sometimes outweigh the complexity of traditional wire transfers.

Security Protocols and Financial Safety in the Digital Age

In the realm of personal finance, security is synonymous with asset protection. The PayPal card suite offers several layers of defense that are superior to many traditional “off-the-shelf” debit cards.

Real-Time Monitoring and Fraud Protection

Every transaction made with a PayPal card triggers an instant notification on your mobile device. From a financial security perspective, this allows for the immediate identification of unauthorized charges. If a card is lost or stolen, it can be “frozen” instantly within the app, preventing any capital loss without the need to wait on hold for a customer service representative.

The Advantage of Zero Liability

The Mastercard-branded PayPal cards come with “Zero Liability” protection. This means that as long as you exercise reasonable care in protecting your card and notify PayPal promptly of any unauthorized use, you are not held responsible for fraudulent charges. This level of protection is essential when using the card for online transactions, where the risk of data breaches is statistically higher.

Secure Integration with Digital Wallets

By adding your PayPal card to Apple Pay, Google Pay, or Samsung Pay, you add a layer of “tokenization” to your financial transactions. The merchant never sees your actual card number; instead, a one-time digital token is used. This reduces the risk of card-cloning at physical point-of-sale terminals, further safeguarding your primary financial accounts.

Conclusion: The PayPal Card as a Gateway to Financial Efficiency

Obtaining a PayPal card is a strategic decision that bridges the gap between digital earnings and physical spending. Whether you are seeking to optimize your credit rewards, manage a burgeoning side hustle, or simply find a more disciplined way to budget your monthly income, the PayPal card ecosystem offers a solution.

By understanding the nuances of each card type, meticulously following the application process, and leveraging the security and reward features available, you can transform a simple piece of plastic into a sophisticated engine for financial growth. In an era where “time is money,” the instant access and seamless integration provided by these tools represent the pinnacle of modern financial efficiency.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.