In the landscape of modern finance, where digital transactions often dominate, the cashier’s check retains a unique and critical role, particularly for significant financial dealings. When you need to ensure funds are guaranteed for a large purchase or an important transaction, a cashier’s check from a reputable institution like Chase Bank offers a level of security and assurance unmatched by a personal check. Understanding how to obtain one efficiently and effectively is a crucial skill for navigating various financial milestones, from real estate closings to purchasing a vehicle.

Understanding Cashier’s Checks: More Than Just a Personal Check

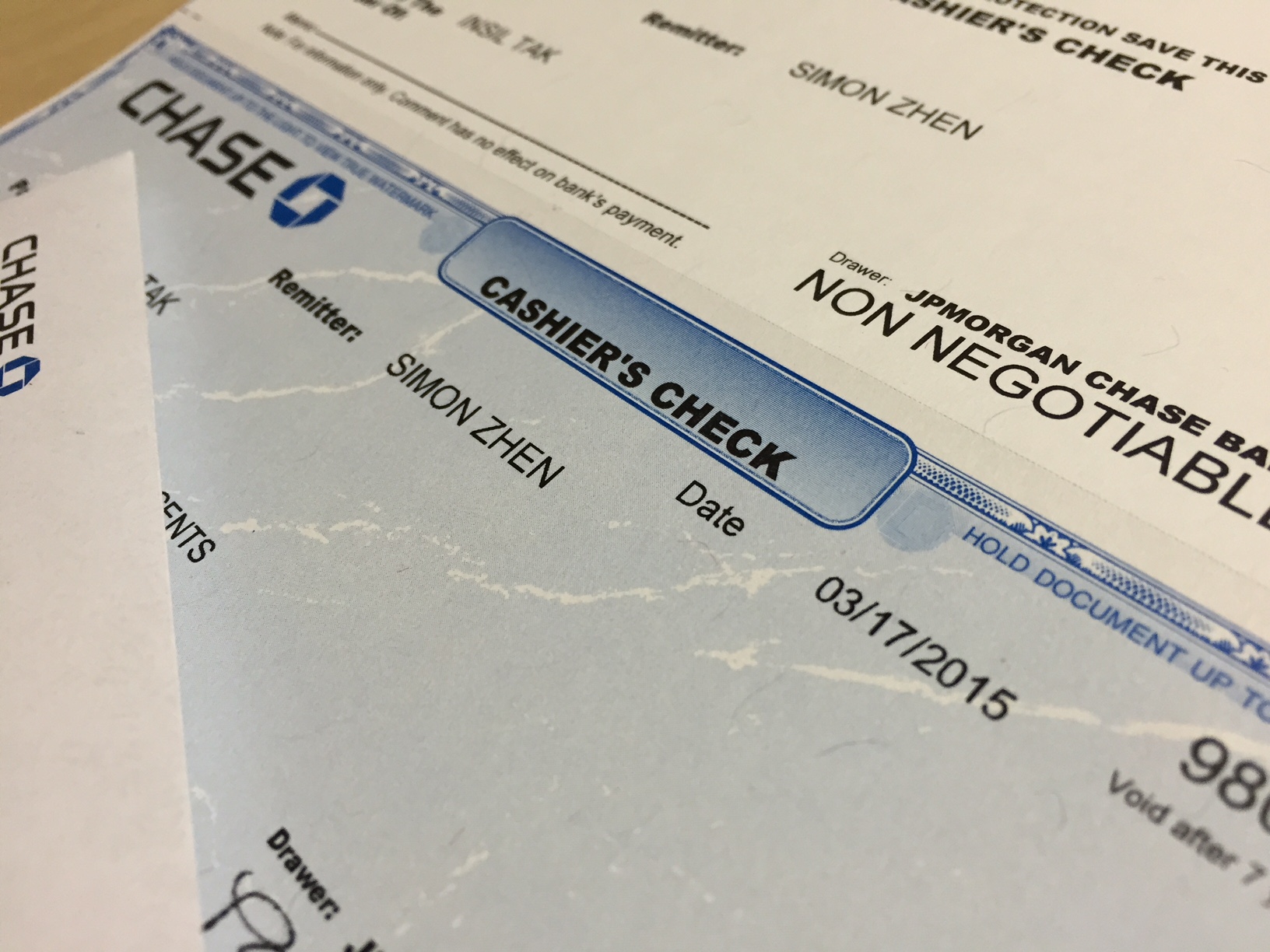

A cashier’s check is a payment instrument issued by a financial institution, like Chase Bank, drawn on its own funds rather than on the account holder’s personal funds. This fundamental difference is what imbues it with its superior security and reliability. Unlike a personal check, which can bounce if the issuer’s account lacks sufficient funds, a cashier’s check guarantees payment because the money is debited directly from your account (or an equivalent amount is provided) at the time of issuance and held by the bank.

Key Characteristics and Benefits

The primary benefit of a cashier’s check is its guaranteed funds status. When Chase Bank issues a cashier’s check, it immediately withdraws the specified amount from your account and holds it in the bank’s own reserves until the check is cashed or deposited by the payee. This process eliminates the risk of non-sufficient funds (NSF) for the recipient, making it a highly trusted form of payment.

Furthermore, cashier’s checks are generally considered more secure due to features such as watermarks, specific security printing, and the requirement of a bank representative’s signature. This makes them difficult to counterfeit compared to standard checks. They also provide a clear audit trail, as the bank maintains records of all cashier’s checks issued, including the payee, amount, and date. This documentation can be invaluable for dispute resolution or tax purposes.

When You Might Need One

Cashier’s checks are typically requested for transactions where a high degree of financial trust and guaranteed funds are paramount. Common scenarios include:

- Real Estate Transactions: Buying a home or land often requires a cashier’s check for down payments, earnest money deposits, or closing costs. Sellers and escrow agents demand this assurance.

- Vehicle Purchases: When buying a car, boat, or RV from a private seller or even a dealership, a cashier’s check is a common requirement to secure the sale.

- Large Rent or Security Deposits: Some landlords or property management companies, especially for high-value properties, may request a cashier’s check for the initial rent and security deposit.

- Legal Settlements: Payments related to legal judgments, settlements, or court fees often necessitate guaranteed funds.

- International Transactions: While wire transfers are also common, for certain international payments where a physical check is preferred, a cashier’s check can offer enhanced security.

- High-Value Purchases from Individuals: When buying expensive items like antiques, collectibles, or equipment from an individual, a cashier’s check protects both buyer and seller.

In each of these instances, the cashier’s check mitigates risk for the recipient, ensuring they receive the agreed-upon funds without delay or complication.

Prerequisites for Obtaining a Cashier’s Check at Chase

Before you head to a Chase Bank branch, understanding the prerequisites can streamline the process and prevent unnecessary trips. Proper preparation ensures you have all the necessary information and funds readily available.

Account Requirements

To obtain a cashier’s check from Chase Bank, you generally need to be an account holder with sufficient funds to cover the check’s amount and any associated fees. Chase will typically draw the funds directly from your checking or savings account. If you do not have an account with Chase, obtaining a cashier’s check from them may be challenging or impossible, as they primarily serve their existing customers for this service to ensure proper identity verification and fund availability. In some rare cases, non-account holders might be able to purchase a money order or a similar instrument, but a true cashier’s check is usually exclusive to account holders.

Necessary Documentation and Information

When you visit a Chase branch to request a cashier’s check, be prepared with the following:

- Valid Photo Identification: This is non-negotiable. Acceptable forms include a government-issued ID such as a driver’s license, state ID card, or passport. This verifies your identity as the account holder.

- Chase Debit Card or Account Number: While your ID helps, having your debit card or knowing your account number expedites the process of accessing your account.

- The Exact Amount of the Check: Know the precise dollar amount required for the cashier’s check.

- The Full Name of the Payee: This is the individual or entity to whom the check will be made out. Ensure the name is spelled correctly and completely.

- Any Memo Information: If there’s a specific purpose for the check (e.g., “Down Payment for 123 Main St.”), having this ready can be helpful for the bank representative to include it in the memo line.

It’s advisable to write down all this information beforehand to ensure accuracy and speed when you’re at the teller window.

Funding the Check

The amount of the cashier’s check, plus any service fees, will be debited directly from your Chase checking or savings account. Ensure that the account you intend to use has sufficient funds to cover the total amount. If you are close to your account balance, it’s wise to verify your balance through the Chase mobile app, online banking, or an ATM before visiting the branch. Attempting to get a cashier’s check without adequate funds will result in delays or an inability to complete the transaction. In some cases, for very large amounts, the bank might require the funds to have been cleared in your account for a certain period to prevent fraud.

Step-by-Step Guide to Getting Your Check

Obtaining a cashier’s check from Chase Bank is a relatively straightforward process, primarily conducted in-person.

In-Person at a Chase Branch

- Locate Your Nearest Chase Branch: Use the Chase mobile app or website to find a branch location convenient for you. It’s often beneficial to choose a branch where you typically conduct your banking if you’re not visiting your primary branch.

- Gather Your Essentials: Ensure you have your valid photo ID, debit card or account number, the exact check amount, and the payee’s full name.

- Approach a Teller or Customer Service Representative: When you enter the branch, you can typically approach any available teller. Inform them that you wish to obtain a cashier’s check.

- Provide Required Information: The teller will ask for your identification and account information. They will then confirm the amount of the check and the payee’s name. Double-check the payee’s name for accuracy before the check is printed.

- Confirm the Debit and Fees: The teller will inform you of the total amount to be debited from your account, which includes the check amount and any associated service fee. Confirm this before proceeding.

- Review and Receive the Check: Once the cashier’s check is printed, the teller will present it to you. Carefully review all details: the amount, the payee’s name, the date, and the bank’s signature. Ensure everything is correct before you leave the counter. The teller will usually provide you with a receipt; keep this for your records as proof of purchase.

Potential Online or Phone Inquiry

While you cannot issue a cashier’s check online or over the phone for security reasons, you can certainly use Chase’s online banking platform or contact their customer service line to:

- Check Account Balances: Verify you have enough funds.

- Confirm Branch Hours and Locations: Plan your visit.

- Inquire About Fees: Get up-to-date information on any service charges.

- Understand Bank Policies: Clarify any specific requirements or limits regarding cashier’s checks.

These resources can help you prepare for your in-person visit, but the actual issuance of the cashier’s check will always require a physical visit to a Chase branch.

Fees, Limits, and Important Considerations

Understanding the costs and potential restrictions associated with cashier’s checks is vital for effective financial planning.

Associated Costs

Chase Bank, like most financial institutions, typically charges a service fee for issuing a cashier’s check. This fee is usually a flat rate, often in the range of $5 to $10, though it can vary based on your account type and relationship with the bank. For example, certain premium checking accounts or private client relationships might waive these fees. Always inquire about the current fee structure when you request the check or check Chase’s current fee schedule online. The fee will be debited from your account along with the check amount.

Daily Limits and Large Transactions

While cashier’s checks offer guaranteed funds, there might be internal limits set by Chase Bank regarding the maximum amount that can be issued in a single check or within a day. For exceptionally large transactions (e.g., several hundred thousand dollars or more), it’s highly recommended to call your specific Chase branch in advance. Inform them of the large amount you intend to request. This pre-notification allows the branch to ensure they have the necessary personnel, forms, and procedures in place, and can also confirm specific security protocols or require additional verification for such large sums. They may also advise on alternative methods like wire transfers if the amount exceeds their comfort level for a single cashier’s check.

Verifying a Cashier’s Check

If you are on the receiving end of a cashier’s check, especially for a significant amount, it’s prudent to verify its authenticity. The most reliable method is to contact the issuing bank directly. Do not rely on contact information provided on the check itself, as this could be fraudulent. Instead, independently look up the bank’s official phone number or visit a branch. When calling, provide the check number, payee name, and amount. A legitimate bank will be able to confirm the check’s issuance. This step is critical to protect against common scams involving fake cashier’s checks.

What If It’s Lost or Stolen?

Losing a cashier’s check can be a stressful situation, but steps can be taken. Immediately contact Chase Bank to report the loss or theft. Because cashier’s checks represent guaranteed funds, the bank will typically require you to complete a Declaration of Lost, Stolen, or Destroyed Instrument form, which often includes an indemnity agreement. This agreement essentially holds the bank harmless if the original check is later cashed by someone else. Due to the nature of guaranteed funds, the bank may place a waiting period (often 90 days or more) before reissuing the funds, to allow time for the original check to surface or expire. This waiting period protects the bank from having to pay out twice if the original check is eventually presented.

Alternative Secure Payment Methods

While cashier’s checks are excellent for many situations, other secure payment methods offered by Chase Bank might be more suitable depending on your specific needs.

Wire Transfers

For immediate and often international high-value transactions, a wire transfer is a robust alternative. Wire transfers directly move funds electronically from one bank account to another. They are irreversible once initiated and provide instant access to funds for the recipient (domestically). Chase offers both domestic and international wire transfer services, typically for a higher fee than a cashier’s check. They are ideal for time-sensitive payments where physical checks are impractical.

Certified Checks

A certified check is similar to a cashier’s check but differs slightly. With a certified check, the bank verifies that sufficient funds are in the account holder’s personal account and then “certifies” the check, guaranteeing the payment. The funds remain in the account holder’s account until the check clears, but they are frozen by the bank, making them unavailable for other use. Certified checks are still drawn on the account holder’s funds, not the bank’s, offering a slightly different risk profile than a cashier’s check. Chase can issue certified checks, often for a similar fee to cashier’s checks.

Money Orders

For smaller sums, typically up to $1,000, money orders are a cost-effective and secure alternative. Money orders are prepaid and issued by post offices, convenience stores, and some banks. They are essentially a guaranteed form of payment, much like a cashier’s check but for lower amounts. Chase Bank offers money orders to account holders, and they can be a convenient option for sending small, secure payments without using a personal check or cash.

Each of these financial tools serves a specific purpose in the secure transfer of funds, and choosing the right one depends on the amount, urgency, and recipient’s requirements for your particular transaction. When in doubt, consulting with a Chase Bank representative can help you determine the best option.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.