In the world of finance, percentages are more than just mathematical expressions; they are the fundamental language of value, growth, and risk. Whether you are a retail investor tracking the performance of your portfolio, a small business owner analyzing profit margins, or an individual trying to optimize a monthly budget, understanding how to find the percent of something is an essential skill.

Percentages allow us to standardize information, making it possible to compare disparate financial figures on a level playing field. Without the ability to calculate and interpret percentages, making informed decisions about interest rates, tax implications, or investment returns becomes a matter of guesswork rather than strategy. This guide explores the critical applications of percentage calculations within the “Money” niche, providing you with the tools to navigate your financial journey with precision.

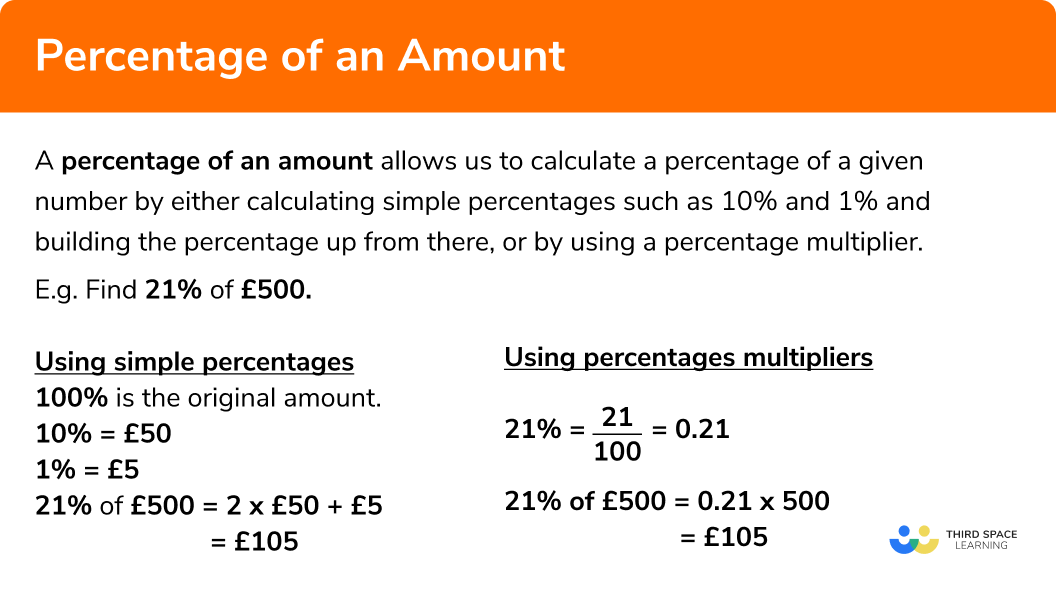

1. The Core Formula: Understanding the “Part of the Whole”

At its most basic level, finding a percentage is the process of determining how one number relates to another based on a scale of 100. The word “percent” literally stems from the Latin per centum, meaning “by the hundred.” In a financial context, this allows us to understand what portion of our total resources is being allocated to a specific area.

The Basic Percentage Calculation

To find the percentage of a specific amount, the formula is straightforward:

(Part / Whole) × 100 = Percentage

For example, if you decide to save $500 out of a $4,000 monthly salary, you are calculating what “percent” of your income is being diverted to savings. Dividing 500 by 4,000 gives you 0.125. Multiplying by 100 results in 12.5%. This simple calculation is the bedrock of personal budgeting, allowing you to see exactly where your money goes relative to your total earnings.

Finding the Value from a Percentage

Often in finance, you are given the percentage and need to find the actual dollar amount. This is common when calculating sales tax, tips, or investment fees. The formula is:

(Percentage / 100) × Total Value = Amount

If an investment platform charges a 0.75% annual management fee on a $50,000 portfolio, you would divide 0.75 by 100 (0.0075) and multiply it by 50,000. The result, $375, represents the tangible cost of that service. Mastering this reverse calculation ensures you are never surprised by the “small print” in financial contracts.

2. Percentage Change: Measuring Financial Growth and Inflation

In the realm of investing and economic health, static numbers rarely tell the whole story. What matters most is the direction and velocity of change. To understand how much an asset has grown or how much purchasing power you have lost to inflation, you must be able to calculate percentage increase and decrease.

Calculating Investment Returns

The most common use of percentage change is calculating the Return on Investment (ROI). The formula is:

[(Current Value – Original Value) / Original Value] × 100 = Percentage Change

If you purchased a stock for $150 and it is now worth $180, the increase is $30. Dividing $30 by the original $150 gives you 0.2, or a 20% gain. This calculation is vital because it allows you to compare the performance of a $150 stock to a $1,000 stock. A $30 gain on a $150 investment is far more impressive than a $30 gain on a $1,000 investment, and the percentage calculation is what reveals that truth.

Understanding the Impact of Inflation

Inflation is the percentage at which the general level of prices for goods and services rises, subsequently eroding purchasing power. If the annual inflation rate is 4%, a basket of goods that cost $100 last year will cost $104 this year. For an individual, understanding this percentage is crucial for salary negotiations and retirement planning. If your annual raise is 3% but inflation is 4%, you have effectively received a 1% pay cut in terms of “real” purchasing power. Being able to calculate these shifts allows you to adjust your financial strategy to stay ahead of the curve.

3. Percentages in Debt and Credit Management

For most people, debt is the most significant hurdle to wealth accumulation. Interest rates, expressed as percentages, determine the cost of borrowing money. Understanding how these percentages compound can mean the difference between financial freedom and a cycle of perpetual debt.

Deciphering APR and Interest Costs

The Annual Percentage Rate (APR) represents the yearly cost of funds over the term of a loan. However, many credit cards calculate interest daily based on your average daily balance. To find the daily periodic rate, you divide the APR by 365.

If you carry a $2,000 balance on a card with a 24% APR, your daily interest rate is approximately 0.0657%. While that seems negligible, calculating the monthly impact (0.0657% × 30 days = ~1.97%) shows that you are paying nearly $40 a month just in interest. Understanding how to break down these percentages helps you prioritize which debts to pay off first—generally those with the highest percentage rates.

The Credit Utilization Ratio

In the world of personal finance and credit scoring, the “Credit Utilization Ratio” is a critical percentage. It is calculated by dividing your total used credit by your total available credit limit. Financial experts generally recommend keeping this percentage below 30%. If you have a total credit limit of $10,000 and your balances total $3,000, your utilization is exactly 30%. Knowing how to monitor this percentage allows you to manage your credit score proactively, which in turn helps you qualify for lower interest rate percentages on future loans like mortgages.

4. Strategic Business Finance: Margins and Markups

For entrepreneurs and business professionals, percentages are the primary indicators of health and sustainability. Two of the most misunderstood yet vital calculations involve gross profit margins and markups. While they use the same basic inputs, they tell very different stories about a business’s pricing strategy.

Calculating Profit Margins

A profit margin tells you what percentage of your total sales revenue is kept as profit after expenses. The formula is:

[(Revenue – Cost of Goods Sold) / Revenue] × 100 = Profit Margin

If a business sells a product for $100 and it costs $70 to produce, the profit is $30. The profit margin is 30%. This percentage is essential for understanding efficiency. A company with high revenue but a 2% profit margin is much more vulnerable to market fluctuations than a smaller company with a 25% margin.

Markup vs. Margin

Markup is often confused with margin, but it relates the profit to the cost rather than the selling price. The formula for markup is:

[(Selling Price – Cost) / Cost] × 100 = Markup

Using the same example (Cost $70, Price $100), the markup is ($30 / $70) × 100 = 42.8%. Business owners must understand this distinction to set prices correctly. If you want to achieve a 20% profit margin, you cannot simply mark up your items by 20%; you must calculate the percentage based on the final intended sale price. Mastering these nuances ensures that a business remains solvent and profitable.

5. Portfolio Allocation and Risk Assessment

In wealth management, “how much” you own of a certain asset class is always expressed as a percentage. Diversification is the practice of spreading your investments across various categories to reduce risk, and it is entirely managed through percentage-based targets.

The Power of Asset Allocation

A classic “60/40” portfolio consists of 60% stocks and 40% bonds. As the market fluctuates, these percentages will shift. If stocks perform exceptionally well, they might grow to represent 70% of your portfolio. This increases your risk profile. To return to your original strategy, you must “rebalance”—calculating what dollar amount needs to be moved from stocks to bonds to return to the 60/40 percentage split. This disciplined approach to percentages removes emotion from investing and forces you to “buy low and sell high.”

Dividend Yields and Effective Yields

For income-focused investors, the “Dividend Yield” is a key percentage. It represents the annual dividend payment divided by the stock’s current price. If a stock costs $50 and pays $2 in annual dividends, its yield is 4%.

However, savvy investors also look at “Yield on Cost”—the dividend percentage relative to the price they originally paid. If you bought that same stock years ago at $25, and it still pays a $2 dividend, your effective yield is 8%. Calculating these percentages allows investors to see the true power of long-term holding and compounding growth, providing a much clearer picture of income potential than raw dollar amounts ever could.

Conclusion: The Quantitative Edge

Learning how to find the percent of something is not merely an academic exercise; it is a fundamental pillar of financial literacy. Percentages provide the context necessary to evaluate the true cost of debt, the real growth of investments, and the efficiency of business operations. By mastering these calculations, you move away from a reactive financial life and toward a proactive, strategic approach to wealth management. In the economy of the 21st century, those who understand the math of money are the ones best positioned to grow it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.