Navigating the complexities of the U.S. tax system can often leave individuals uncertain about their financial obligations. Discovering that you owe money to the Internal Revenue Service (IRS) can be daunting, but it’s crucial to identify this status early to manage potential penalties and interest. This guide will walk you through the official channels and best practices for determining if you have an outstanding balance with the IRS, understand why you might, and outline the steps to take once you know.

Common Scenarios Leading to IRS Debt

Before delving into how to check your status, it’s helpful to understand the frequent reasons taxpayers find themselves owing the IRS. Recognizing these scenarios can also help in preventing future tax liabilities.

Insufficient Withholding or Estimated Tax Payments

This is perhaps the most common reason. If you’re an employee, your employer withholds a portion of your paycheck for taxes based on the Form W-4 you submit. If you’ve claimed too many allowances or failed to update your W-4 after a significant life event (like marriage, children, or a second job), too little tax might be withheld. For self-employed individuals, freelancers, or those with significant investment income, estimated tax payments are required throughout the year. Failure to make these, or paying too little, can result in a balance due at tax time.

Untaxed Income

Many forms of income are taxable but may not have taxes withheld at the source. This includes income from the gig economy, rental income, capital gains from investments, or even certain lottery winnings. If you receive income that isn’t subject to automatic withholding, it’s your responsibility to set aside funds for taxes or make estimated payments.

Tax Return Errors or Oversight

Simple mathematical errors, misinterpreting tax laws, or overlooking certain income streams when preparing your tax return can lead to an incorrect calculation of your tax liability. Even minor errors can result in an underpayment that the IRS will identify.

Late or Unfiled Returns

The IRS imposes penalties for both failure to file on time and failure to pay on time. If you file your return late, or worse, don’t file at all, the penalties and interest can quickly accumulate, adding significantly to your original tax debt. An extension to file does not grant an extension to pay.

Audit Adjustments

In some cases, the IRS may audit your tax return. If the audit results in an adjustment to your income, deductions, or credits, it could lead to an increased tax liability and a demand for payment.

Official Methods to Confirm Your IRS Debt Status

The IRS provides several reliable avenues for taxpayers to check their account status and confirm any outstanding balances. Utilizing these official channels ensures accuracy and security.

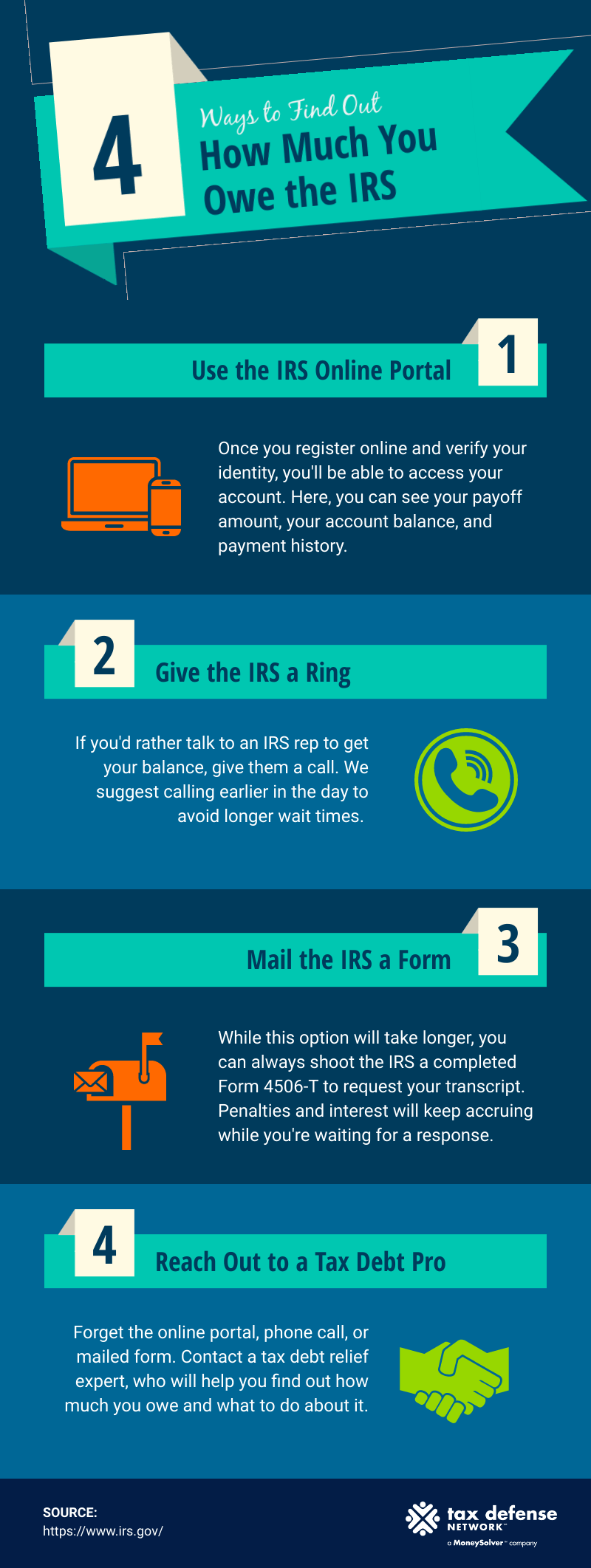

Checking Your IRS Online Account

The IRS online account is arguably the most convenient and comprehensive way to access your tax information.

- How to Access: Visit IRS.gov and search for “IRS Online Account.” You’ll need to create an account if you don’t have one, which involves a robust identity verification process (often requiring a government-issued ID and a selfie, or answering detailed financial questions).

- What You’ll Find: Once logged in, you can view your tax return information for the current year and previous years, payment history, account balance (including any amount owed, interest, and penalties), and certain tax transcripts. This dashboard provides a clear summary of your financial standing with the IRS.

Requesting a Tax Transcript

A tax transcript is a summary of your tax return information or account activity. While it doesn’t always show the current amount due, it provides detailed information that can help you understand your tax history.

- Types of Transcripts:

- Account Transcript: Shows most line items from your original return and any adjustments made by you or the IRS. It also shows payments, penalties, and interest, giving a good overview of your balance due for a specific tax year.

- Record of Account Transcript: Combines the information from the line-by-line tax return transcript and the account transcript.

- How to Request: You can request transcripts online via the “Get Transcript Online” tool on IRS.gov (for immediate access), by mail using Form 4506-T or Form 4506T-EZ, or by phone.

Reviewing IRS Notices and Letters

The IRS primarily communicates balances due through mail. If you owe money, you will almost certainly receive an official notice or letter.

- Common Notices:

- CP14 (Balance Due): This is one of the most common notices, informing you of a balance due on your tax return.

- CP504 (Notice of Intent to Levy): This indicates that you have an unpaid balance, and the IRS intends to levy (seize) your assets if you don’t pay.

- LT11 / Letter 1058 (Final Notice of Intent to Levy and Notice of Your Right to a Hearing): This is a serious notice, generally sent after previous attempts to collect, informing you of the IRS’s intent to levy and your right to appeal.

- What to Look For: Always open and carefully read any mail from the IRS. These notices clearly state the amount owed, the tax year it pertains to, and the reason for the debt, along with deadlines for payment or response.

Contacting the IRS Directly

If you’ve exhausted other methods or prefer direct communication, you can call the IRS.

- Phone Number: The main IRS phone number for individuals is 1-800-829-1040. For businesses, it’s 1-800-829-4933.

- What to Have Ready: Before calling, gather all relevant tax documents, including your Social Security number, date of birth, previous tax returns, and any IRS notices you’ve received. Be prepared for potentially long wait times, especially during tax season.

Deciphering IRS Communications

Receiving an IRS notice can be unsettling, but understanding its components is the first step towards resolving any debt.

Understanding Balance Due Notices

An IRS notice detailing a balance due will break down the amount owed into several categories:

- Original Tax Due: The primary amount of tax the IRS believes you owe.

- Penalties: These can include failure-to-file penalties, failure-to-pay penalties, or accuracy-related penalties. They are typically calculated as a percentage of the unpaid tax.

- Interest: Interest accrues on any unpaid tax and penalties from the original due date of the return until the date of payment. The interest rate is set by the IRS and can change quarterly.

Importance of Response Deadlines

IRS notices almost always include a deadline for response or payment. Ignoring these deadlines can lead to additional penalties, increased interest, and more aggressive collection actions. If you disagree with the notice, you often have a specific window to appeal or provide additional information.

What if You Disagree?

If you believe the IRS has made an error, do not ignore the notice. Gather all supporting documentation that proves your position and respond to the IRS by the specified deadline. This might involve sending a letter of explanation, amended tax returns (Form 1040-X), or disputing the assessment. Consulting a tax professional is highly recommended in such situations.

Navigating Your Options When You Owe

Discovering you owe the IRS money can be stressful, but the agency offers several payment and resolution options. Choosing the right one depends on your financial situation.

Paying in Full

If you have the means, paying your tax debt in full is the best option. It stops the accrual of interest and penalties immediately and prevents any further collection actions.

- How to Pay: The IRS offers several payment methods, including IRS Direct Pay (from your checking or savings account), debit/credit card (through third-party processors, which may charge a fee), Electronic Federal Tax Payment System (EFTPS), electronic funds withdrawal when e-filing, or by check or money order via mail.

Short-Term Payment Plan

If you can pay your full tax liability within 180 days, you might be eligible for a short-term payment plan. While this option allows more time, interest and penalties continue to accrue until the debt is paid off. You can often request this online.

Installment Agreement

If you can’t pay your full tax debt within 180 days, an installment agreement allows you to make monthly payments for up to 72 months.

- Eligibility: Generally, you can set up an installment agreement if you owe a combined total of under $50,000 (tax, penalties, and interest) for individuals or under $25,000 for businesses.

- Important Note: Interest and penalties continue to accrue, though the failure-to-pay penalty rate may be reduced. Filing an installment agreement request can often be done online using the IRS Online Payment Agreement application.

Offer in Compromise (OIC)

An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This is an option for taxpayers who are experiencing significant financial difficulty and cannot pay their full tax debt.

- Eligibility: The IRS generally approves an OIC when your ability to pay is limited. They consider your ability to pay, income, expenses, and asset equity. The OIC process is complex and requires detailed financial disclosures.

- When to Consider: This is typically a last resort for those facing severe hardship, as the acceptance rate is relatively low.

Currently Not Collectible (CNC) Status

If the IRS determines that you are unable to pay your tax debt due to financial hardship, they may place your account in “Currently Not Collectible” status. This means the IRS will temporarily stop collection efforts.

- Important Note: This is not a forgiveness of debt. Interest and penalties continue to accrue, and the IRS can review your financial situation periodically. If your financial situation improves, the IRS can resume collection activities.

Professional Tax Help

If your tax situation is complex, you owe a significant amount, or you’re unsure about the best course of action, consult a qualified tax professional. Enrolled Agents (EAs), Certified Public Accountants (CPAs), and tax attorneys specialize in tax law and can help you understand your options, negotiate with the IRS, and ensure you comply with regulations.

Proactive Strategies to Avoid Future Tax Debt

The best way to deal with IRS debt is to avoid it altogether. Implementing proactive financial strategies can significantly reduce your risk of owing money in future tax seasons.

Adjusting Your Withholding (Form W-4)

Regularly review your W-4 form, especially after significant life changes like marriage, divorce, birth of a child, or starting a new job. Use the IRS Tax Withholding Estimator tool available on IRS.gov. This tool helps you accurately determine the amount of tax to withhold from your pay, aiming for a tax liability close to zero or a small refund.

Making Estimated Tax Payments

If you’re self-employed, a gig worker, or have substantial income not subject to withholding (e.g., investments, rental income), make quarterly estimated tax payments using Form 1040-ES. This ensures you pay taxes as you earn income, avoiding a large tax bill and potential penalties at year-end.

Keeping Meticulous Records

Maintain organized records of all income, expenses, deductions, and credits. This includes bank statements, receipts, invoices, and any tax-related documents. Good record-keeping simplifies tax preparation and provides necessary documentation if the IRS has questions or conducts an audit.

Filing on Time, Even if You Can’t Pay

Even if you cannot afford to pay your entire tax bill, always file your tax return or an extension by the due date. This avoids the failure-to-file penalty, which is typically much larger than the failure-to-pay penalty. You can then address payment options with the IRS.

Regular Financial Health Checks

Make it a practice to review your income, expenses, and tax situation throughout the year, not just at tax time. A mid-year check-up can reveal potential tax liabilities, allowing you to make adjustments to withholding or estimated payments before it’s too late.

By understanding how to check your IRS account, recognizing common reasons for debt, and proactively managing your finances, you can navigate your tax obligations with greater confidence and avoid unwelcome surprises.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.