In the world of personal finance and business management, percentages are the fundamental language of progress. Whether you are calculating the return on a recent stock market investment, determining the impact of an interest rate hike on your mortgage, or simply trying to figure out how much of your monthly income is being swallowed by discretionary spending, understanding how to figure percentages out is a non-negotiable skill.

While many view math as a dry academic exercise, in the context of money, it is a tool for empowerment. Percentages allow us to compare apples to oranges, normalizing different financial values so we can make informed decisions. This guide will walk you through the essential methods of calculating percentages within the financial niche, moving from basic calculations to complex wealth-building applications.

The Fundamentals: Understanding Percentages in a Financial Context

To master your money, you must first master the basic “mechanics” of the percentage. At its core, a percentage represents a fraction of 100. In financial terms, this usually represents a portion of a whole—such as your tax bracket relative to your income or a dividend yield relative to a share price.

The Standard Percentage Formula

The most basic way to figure a percentage out is the “Part over Whole” method. To find what percentage a specific amount is of a larger total, you divide the part by the whole and then multiply by 100.

Formula: (Part / Whole) × 100 = Percentage

For example, if you save $500 out of a $4,000 monthly paycheck, the calculation is (500 / 4,000) = 0.125. Multiply that by 100, and you find that your savings rate is 12.5%. Understanding this simple division is the first step toward auditing your financial health.

Converting Decimals and Fractions

In the world of professional finance, you will often encounter percentages expressed as decimals. A 5% interest rate is often represented as 0.05 in financial modeling software. Moving between these formats is essential. To turn a percentage into a decimal, move the decimal point two places to the left (7.5% becomes 0.075). To turn a decimal into a percentage, move it two places to the right. This allows you to quickly calculate “percentage of” a number by simply multiplying (e.g., 0.07 multiplied by $1,000 gives you 7% of $1,000, which is $70).

The Power of Mental Math Shortcuts

When you are sitting in a boardroom or negotiating a deal, you may not always have a calculator handy. Learning mental shortcuts for common percentages can give you a significant edge.

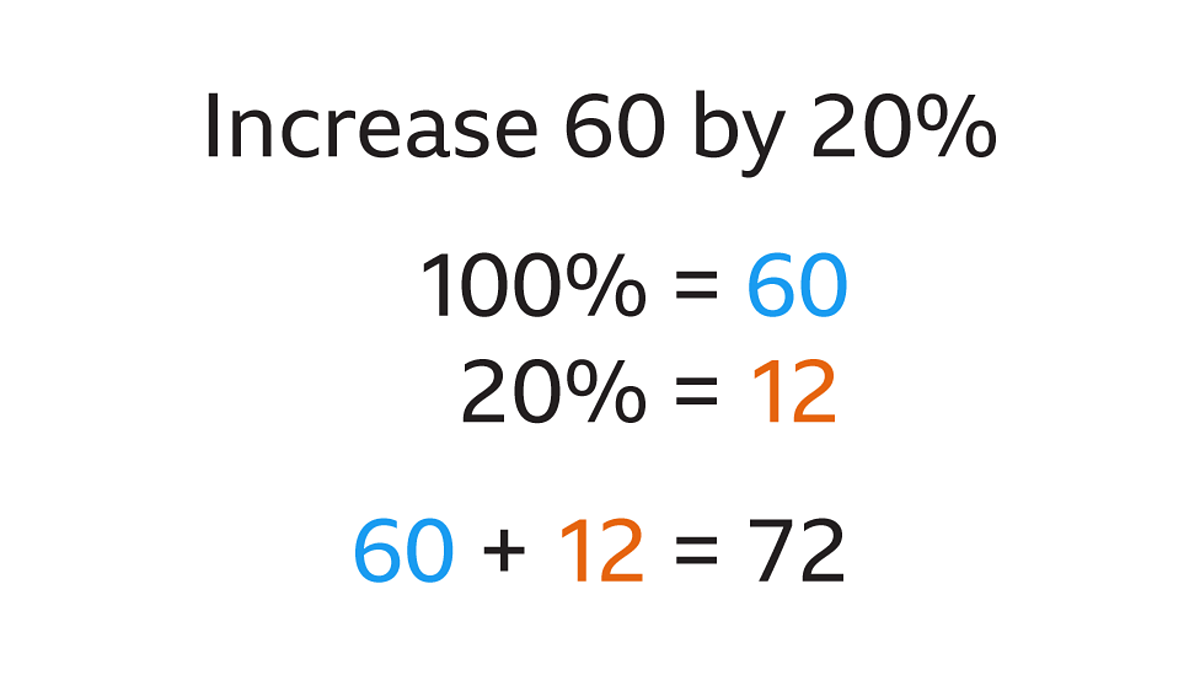

- To find 10%: Move the decimal point one place to the left ($450.00 becomes $45.00).

- To find 5%: Find 10% and cut it in half.

- To find 1%: Move the decimal point two places to the left ($450.00 becomes $4.50).

By combining these, you can calculate almost any figure. To find 16%, calculate 10%, then 5%, then 1%, and add them together.

Percentages in Personal Budgeting and Cash Flow Management

Once you understand the basic formulas, you can apply them to your daily financial life. Budgeting is essentially the art of managing percentages. Instead of looking at raw numbers, successful financial planners look at the “weight” of each expense category.

Applying the 50/30/20 Rule

One of the most popular personal finance frameworks is the 50/30/20 rule. This strategy suggests that you should allocate 50% of your after-tax income to “Needs,” 30% to “Wants,” and 20% to “Savings and Debt Repayment.” To figure out if you are adhering to this, you must calculate the percentage of your total income that each category consumes. If your rent is $2,000 and your income is $5,000, your housing alone is taking up 40% of your total budget, leaving only 10% for other “needs” like utilities and groceries.

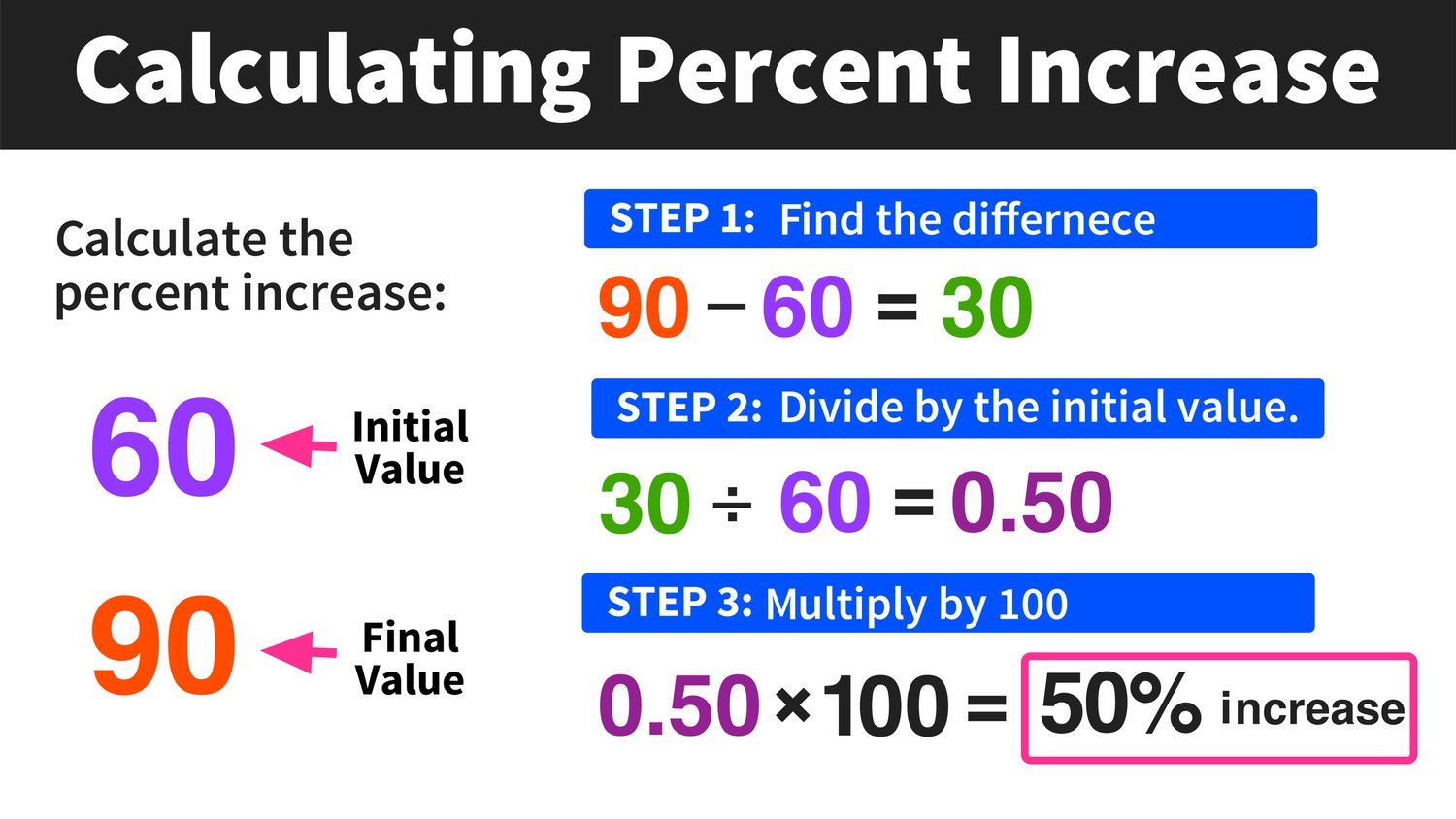

Calculating Percentage Change: Tracking Growth and Inflation

Understanding how to calculate percentage increase or decrease is vital for tracking your net worth or the rising cost of living.

Formula: [(New Value – Old Value) / Old Value] × 100

If your investment portfolio was worth $10,000 last year and is worth $11,500 today, the change is $1,500. Dividing $1,500 by the original $10,000 gives you 0.15, or a 15% increase. Conversely, if the price of eggs rises from $3.00 to $4.50, that is a 50% increase—a staggering figure that highlights why understanding percentages is crucial for gauging the impact of inflation on your purchasing power.

Debt-to-Income (DTI) Ratios

Lenders use percentages to determine your creditworthiness. Your Debt-to-Income ratio is the percentage of your gross monthly income that goes toward paying debts. To figure this out, add up all your monthly debt payments (credit cards, student loans, car loans, etc.) and divide by your gross monthly income. A DTI of 36% or less is generally considered healthy. If you find your DTI creeping toward 50%, the percentage tells you—louder than any raw dollar amount—that you are overleveraged.

Investment Mathematics: ROI, Yields, and Compound Interest

In the realm of investing, percentages are the primary metric for success. Raw profit doesn’t tell the whole story; a $1,000 profit on a $2,000 investment is incredible, while a $1,000 profit on a $1,000,000 investment is negligible.

Return on Investment (ROI)

ROI is the ultimate percentage for any investor. It measures the efficiency of an investment.

Formula: (Current Value – Cost Basis) / Cost Basis

If you buy a stock for $50 and sell it for $75, your gain is $25. $25 divided by the original $50 is 0.50, or a 50% ROI. In business finance, companies use this to decide which projects to fund. If Project A has a projected ROI of 12% and Project B has an ROI of 8%, the decision becomes mathematically clear.

Understanding Dividend Yields and Expense Ratios

When evaluating stocks or mutual funds, you’ll encounter two critical percentages: dividend yields and expense ratios.

- Dividend Yield: This is the annual dividend payment divided by the stock price. It tells you how much “cash flow” you are getting for every dollar invested.

- Expense Ratio: This represents the percentage of your investment that goes to the fund management company. A 1% expense ratio might sound small, but over 30 years, that 1% can consume nearly a third of your total potential gains. Figuring out these small percentages is the difference between retiring comfortably and retiring wealthy.

The Magic of Compound Interest

Compound interest is often called the “eighth wonder of the world” because it involves earning a percentage on top of a percentage. When your investment earns 7% in Year 1, that 7% is added to the principal. In Year 2, you earn 7% on the new, larger total.

To estimate how long it takes for your money to double at a specific percentage rate, use the Rule of 72. Divide 72 by your expected annual percentage return. If you earn 10% a year, your money will double in approximately 7.2 years (72 / 10 = 7.2).

Advanced Financial Applications: Taxes and Interest Rates

As you move into higher levels of financial planning, you must deal with the nuances of interest rates and tax brackets. These percentages are rarely straightforward and require a deeper level of analysis.

Marginal vs. Effective Tax Rates

In many tax systems, income is taxed in “brackets,” meaning different portions of your money are taxed at different percentages. Your marginal tax rate is the percentage of tax applied to your last dollar earned. However, your effective tax rate is the actual percentage of your total income that goes to the government.

To figure out your effective tax rate, divide your total tax bill by your total taxable income. Many people are surprised to find that while they are in a 24% marginal bracket, their effective rate might only be 15% or 18% due to deductions and lower-tier brackets.

The Impact of APR and APY

When borrowing or saving money, you will see two different percentage types: Annual Percentage Rate (APR) and Annual Percentage Yield (APY).

- APR: This is the annual rate charged for borrowing, expressed as a single percentage number that represents the actual yearly cost of funds over the term of a loan.

- APY: This takes into account the effect of compounding interest within the year.

When you are saving money, you want the highest APY. When you are borrowing money (like on a credit card), you need to look at the APR to understand how much that debt is truly costing you. Even a 1% difference in a mortgage APR can result in tens of thousands of dollars in interest over the life of a 30-year loan.

Profit Margins in Business Finance

For those running a side hustle or a full-time business, “Profit Margin” is the most important percentage to track.

- Gross Margin: (Total Revenue – Cost of Goods Sold) / Total Revenue. This tells you the percentage of revenue left after direct production costs.

- Net Margin: (Total Revenue – All Expenses) / Total Revenue. This is the “bottom line” percentage.

A company can have millions in revenue, but if its net margin is only 2%, it is in a much riskier position than a smaller company with a 25% net margin.

Conclusion: Data-Driven Financial Decisiveness

Learning how to figure percentages out is more than just a math lesson; it is a fundamental pillar of financial literacy. By moving away from raw numbers and focusing on percentages, you gain the ability to compare different financial products, track your progress toward goals with precision, and understand the true cost of debt.

Whether you are calculating your savings rate to ensure a stable future, analyzing the ROI of a potential investment, or auditing your business’s profit margins, the ability to manipulate and interpret percentages is what separates those who simply “spend money” from those who “manage wealth.” In the end, money is a game of numbers, and those who master the percentages are the ones who ultimately win.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.