Inflation, a ubiquitous economic phenomenon, impacts nearly every facet of our financial lives. From the grocery store prices to the cost of a new car, its insidious creep can erode purchasing power and alter long-term financial planning. Understanding how to “figure out” the inflation rate isn’t just an academic exercise; it’s a crucial skill for informed personal finance management, savvy investing, and effective business decision-making. While the official figures are calculated by governmental bodies, grasping the underlying methodology and being able to interpret the data empowers individuals and businesses to navigate an inflationary environment with greater confidence. This article delves into the core concepts, methodologies, and practical applications of understanding and calculating inflation rates.

Understanding the Fundamentals of Inflation

At its core, inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. It’s not about the price increase of a single item, but rather a broad-based increase across a basket of goods and services representative of consumer spending. This distinction is critical because individual price fluctuations are normal and can be driven by myriad factors, from seasonal demand to supply chain disruptions for specific products. Inflation, however, signifies a sustained, economy-wide trend.

Defining Inflation and Its Causes

Inflation is typically measured as a percentage change in a price index over a specific period, usually a year. For instance, if the inflation rate is 3%, it means that, on average, prices for the goods and services included in the index have risen by 3% compared to the previous year.

The causes of inflation are complex and can be broadly categorized into two main types:

- Demand-Pull Inflation: This occurs when there is too much money chasing too few goods. When aggregate demand in the economy outpaces aggregate supply, businesses can raise prices because consumers are willing and able to pay more. This can be fueled by factors such as increased government spending, a booming economy with low unemployment leading to higher wages and consumer confidence, or a sudden increase in the money supply.

- Cost-Push Inflation: This arises when the cost of producing goods and services increases, forcing businesses to pass those higher costs onto consumers through higher prices. Common drivers of cost-push inflation include rising raw material costs (like oil or metals), increased labor costs due to wage hikes or labor shortages, and supply chain disruptions that make it more expensive to transport goods.

Other factors can contribute to inflation, including built-in inflation, which is driven by expectations of future inflation. If workers expect prices to rise, they will demand higher wages, which in turn increases business costs, leading to further price increases in a self-fulfilling prophecy.

Differentiating Inflation from Other Economic Concepts

It’s important to distinguish inflation from related economic concepts to avoid confusion.

- Deflation: The opposite of inflation, deflation is a sustained decrease in the general price level. While lower prices might sound appealing, deflation can be economically damaging, leading to decreased consumer spending as people anticipate further price drops, reduced business profits, and a potential debt spiral.

- Stagflation: This is a more problematic scenario where an economy experiences high inflation coupled with high unemployment and stagnant economic growth. It’s a difficult situation for policymakers to address, as typical solutions for inflation (like raising interest rates) can worsen unemployment.

- Disinflation: This refers to a slowdown in the rate of inflation. For example, if inflation was 5% last year and is 3% this year, the rate has disinflated. This is generally seen as a positive development as it signifies that price increases are moderating.

Understanding these distinctions provides a more nuanced view of the economic landscape and the specific challenges or opportunities presented by different price trends.

The Mechanics of Inflation Measurement: Price Indexes

The backbone of measuring inflation lies in the creation and maintenance of comprehensive price indexes. These indexes are designed to track the average change over time in the prices paid by consumers for a representative “basket” of goods and services.

The Consumer Price Index (CPI) Explained

The most widely cited measure of inflation for consumers is the Consumer Price Index (CPI). In the United States, the Bureau of Labor Statistics (BLS) is responsible for calculating and publishing the CPI. The process involves several key steps:

-

Defining the Basket: The BLS conducts detailed surveys to determine what goods and services households typically purchase. This basket is broad, encompassing categories like food and beverages, housing, apparel, transportation, medical care, recreation, education, and communication. The relative importance of each category is determined by its share in average household spending. For instance, housing typically represents a larger portion of consumer spending than apparel.

-

Collecting Prices: The BLS collects prices for thousands of specific items across the United States on a monthly basis. This involves sending agents to retail stores, service providers, and rental units to record the prices of identical or comparable items over time. Online price collection has also become an increasingly important part of the process.

-

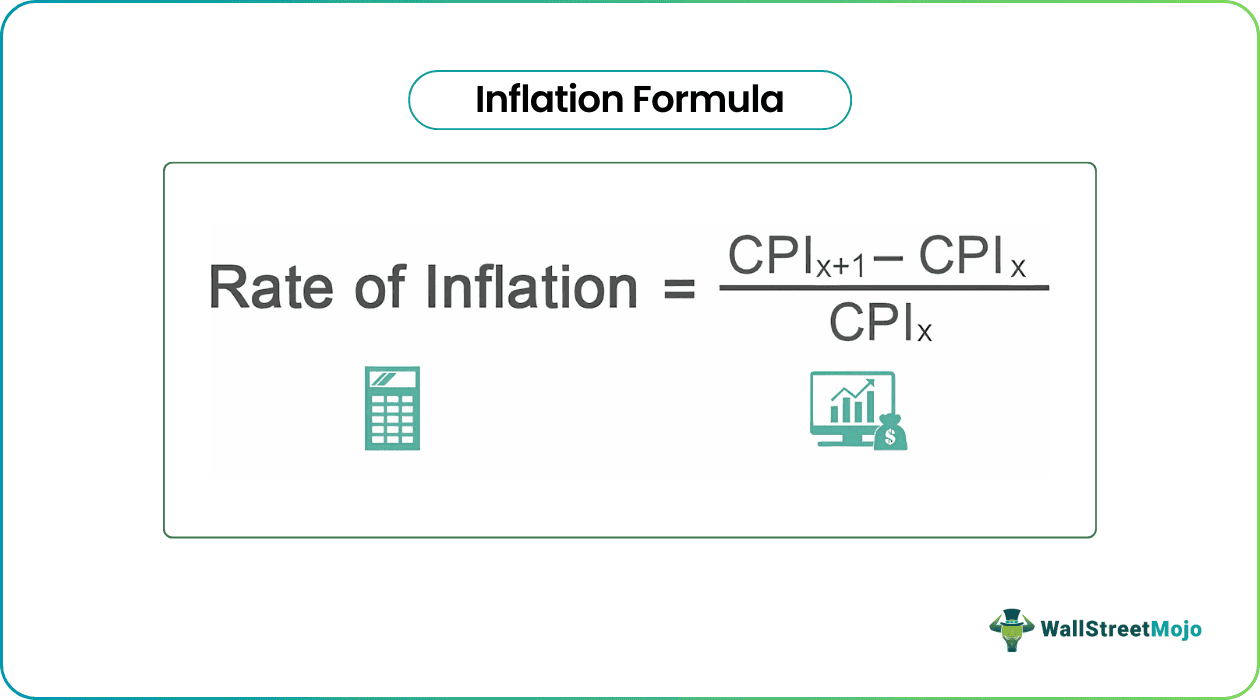

Calculating the Index: The collected prices are used to calculate an index. The index is set to 100 in a base period. As prices change, the index value fluctuates. The formula for the CPI for a given period is:

CPI = (Cost of Market Basket in Current Period / Cost of Market Basket in Base Period) * 100

For example, if the cost of the basket was $200 in the base period and $210 in the current period, the CPI would be (210 / 200) * 100 = 105.

-

Calculating the Inflation Rate: The inflation rate is then derived from the percentage change in the CPI between two periods:

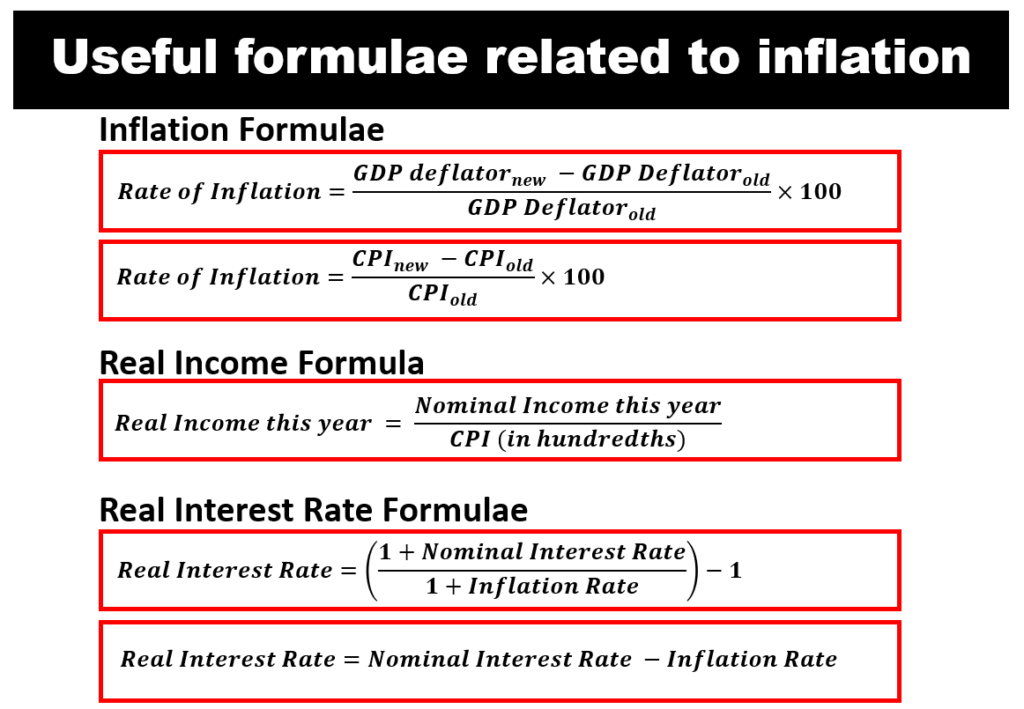

Inflation Rate = ((CPI in Current Period – CPI in Previous Period) / CPI in Previous Period) * 100

For example, if the CPI was 275 in January and 277 in February, the monthly inflation rate would be ((277 – 275) / 275) * 100 = approximately 0.73%. Annual inflation rates are calculated using CPI figures from the same month in consecutive years.

Other Important Price Indexes

While the CPI is the most common, other price indexes provide different perspectives on inflation:

- Producer Price Index (PPI): The PPI measures the average change over time in the selling prices received by domestic producers for their output. It tracks prices at the wholesale level and can sometimes be a leading indicator of future CPI changes, as rising production costs often eventually get passed on to consumers. The PPI can be broken down by industry or by stage of processing (crude goods, intermediate goods, finished goods).

- Personal Consumption Expenditures (PCE) Price Index: This index, released by the Bureau of Economic Analysis (BEA), is another key measure of inflation. It’s considered by many economists to be a broader measure than the CPI because it includes spending by all individuals and is weighted differently, reflecting actual consumption patterns and substitutions consumers make. The Federal Reserve often uses the PCE price index as its preferred inflation gauge.

- GDP Deflator: This is a measure of the price level of all new, domestically produced, final goods and services in an economy. It’s calculated by dividing nominal GDP by real GDP and multiplying by 100. The GDP deflator is a very broad measure, encompassing all components of GDP, not just consumer spending.

Each of these indexes offers a unique lens through which to view price changes, and understanding their differences can provide a more comprehensive economic picture.

Applying Inflation Rate Calculations to Personal Finance

The ability to “figure out” inflation rate isn’t just about understanding economic reports; it’s about applying that knowledge to make smarter financial decisions in your everyday life. Inflation directly impacts your purchasing power, the real return on your investments, and the future value of your savings.

Assessing the Impact on Purchasing Power

Inflation erodes the value of your money over time. This means that the same amount of money will buy fewer goods and services in the future than it does today. For instance, if inflation is 5% per year, then a $100 bill today will only be able to purchase what $95.24 could buy last year (approximately).

To calculate the impact of inflation on your purchasing power, you can use the following formula:

Real Value of Money = Nominal Amount / (1 + Inflation Rate)^Number of Years

Let’s say you have $10,000 saved. If the inflation rate is 3% per year, after 5 years, the purchasing power of that $10,000 will be:

Real Value = $10,000 / (1 + 0.03)^5 = $10,000 / 1.15927… = $8,626.09

This demonstrates that while you still have $10,000, its ability to buy goods and services has decreased by over $1,300 due to inflation. This highlights the importance of earning a return on your savings that outpaces inflation.

Making Informed Investment Decisions

Inflation is a critical factor to consider when making investment decisions. The nominal return on an investment is the percentage gain you see on paper. However, it’s the real return – the nominal return adjusted for inflation – that truly reflects the increase in your purchasing power.

To calculate the real rate of return on an investment, you can use the Fisher Equation (though a simpler approximation is often used for lower inflation rates):

Real Rate of Return ≈ Nominal Rate of Return – Inflation Rate

For example, if your investment yields a nominal return of 7% and the inflation rate is 3%, your real rate of return is approximately 4%. This means your purchasing power has increased by 4%.

If, however, your investment yields 2% and inflation is 3%, your nominal return is positive, but your real rate of return is -1%. In this scenario, even though your investment grew by 2%, the purchasing power of your money has decreased by 1%. This is why investments like cash in a low-interest savings account can lose value in real terms during periods of high inflation.

When choosing investments, it’s essential to consider assets that have historically provided returns exceeding inflation over the long term. These can include equities, real estate, and certain inflation-protected securities. Understanding the expected inflation rate helps in setting realistic return expectations and selecting appropriate investment vehicles.

Budgeting and Financial Planning for the Future

Inflation makes long-term financial planning more challenging. Retirement planning, for instance, requires estimating future expenses, which will inevitably be higher due to inflation. If you estimate needing $50,000 per year in retirement, and inflation averages 3% over 30 years until you retire, you’ll actually need significantly more to maintain the same lifestyle.

A simple way to project future costs is to use the inflation rate as a growth factor:

Future Cost = Present Cost * (1 + Inflation Rate)^Number of Years

Using the retirement example:

Future Annual Retirement Need = $50,000 * (1 + 0.03)^30 = $50,000 * 2.427… = $121,351.78

This starkly illustrates the power of compounding inflation. When creating budgets, it’s wise to incorporate a buffer for potential inflation. For short-term goals, the impact might be minor, but for long-term aspirations like buying a home or funding education, accounting for inflation is paramount. Regularly reviewing and adjusting financial plans to reflect current inflation trends ensures that your savings goals remain achievable.

Beyond Official Figures: Practical Approaches to Gauging Inflation

While official inflation statistics are essential for broad economic understanding, there are practical ways individuals can gain a more personal sense of inflation and its impact on their lives. This involves paying attention to specific price changes and understanding how these might be influenced by broader economic forces.

Tracking Personal Price Changes

The most intuitive way to “figure out” inflation is to observe the prices of goods and services you regularly purchase.

- Grocery Bills: Keep a mental note or even a record of the prices of staple items like milk, bread, eggs, and produce. A noticeable increase in your weekly grocery bill, even if your purchasing habits haven’t changed, is a direct indication of inflation at play.

- Energy Costs: Monitor your utility bills, including electricity, gas, and fuel for your vehicle. Fluctuations in these costs are often sensitive to global commodity prices and can be a significant contributor to overall inflation.

- Major Purchases: When considering larger expenditures like appliances, electronics, or vehicles, compare current prices to what you might have paid a year or two ago. While sales and discounts can influence these prices, a consistent upward trend across many such items suggests broader inflationary pressures.

By actively tracking these personal price changes, you can develop an intuitive understanding of how inflation is affecting your household budget. This personal awareness can then be cross-referenced with official inflation data to see if your observations align with the broader economic picture.

Interpreting Economic Indicators and News

Staying informed about economic news and indicators is crucial for understanding the context behind price changes.

- Official Reports: Regularly check the releases from statistical agencies like the Bureau of Labor Statistics (BLS) for CPI data and the Bureau of Economic Analysis (BEA) for PCE data. Look for trends over several months and years, rather than focusing on single-month figures, which can be volatile.

- Central Bank Statements: Pay attention to the statements and decisions of central banks, such as the Federal Reserve. Their actions, particularly interest rate adjustments, are often responses to inflation concerns and can signal their outlook on future price trends.

- Analyst Commentary: Read analyses from reputable financial news outlets and economists. They often provide context and interpretations of inflation data, helping to explain the underlying causes and potential future implications.

By understanding how to interpret these economic indicators and news reports, you can move beyond simply observing price changes to comprehending the forces driving them and their potential future direction. This informed perspective is invaluable for making strategic financial decisions.

The Role of Personal Finance Tools and Calculators

Fortunately, many digital tools and calculators can assist in understanding and projecting the impact of inflation.

- Inflation Calculators: Numerous websites offer free inflation calculators. You input an amount, a starting year, and an ending year, and the calculator will show you how much that amount would be worth in the ending year, adjusted for inflation. Conversely, you can see how much money you would need in the future to have the same purchasing power as a certain amount today.

- Investment Calculators: Many investment platforms and financial planning websites provide calculators that incorporate inflation into return calculations. These tools help you estimate the real growth of your investments, considering both nominal returns and projected inflation rates.

- Budgeting Apps: Advanced budgeting apps can help you track your spending patterns and identify areas where you might be experiencing the effects of inflation most acutely. Some even allow you to set inflation-adjusted savings goals.

Leveraging these readily available financial tools can demystify inflation calculations and provide tangible insights into how it affects your personal financial situation. They transform abstract economic concepts into actionable data, empowering you to make more informed decisions about saving, spending, and investing.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.