Navigating the world of loans can often feel like deciphering a complex financial puzzle, with the interest rate being one of its most critical pieces. Whether you’re considering a mortgage, a car loan, a personal loan, or even managing credit card debt, understanding how to calculate and interpret interest rates is fundamental to making sound financial decisions. It’s not merely a number; it’s the cost of borrowing money, directly impacting your monthly payments and the total amount you’ll repay over the loan’s lifetime. Far too many borrowers overlook the intricacies of interest rates, focusing solely on the principal amount or the monthly payment, thereby potentially committing to unfavorable terms.

This comprehensive guide will demystify loan interest rates, empowering you with the knowledge and tools to accurately figure out your loan’s true cost. We’ll delve into the foundational concepts, explore different types of interest, equip you with calculation methods both manual and digital, and highlight the external factors that influence the rates you’re offered. By the end of this article, you’ll not only know how to calculate interest but also understand why certain rates apply, enabling you to borrow more wisely and manage your finances more effectively.

Understanding the Fundamentals of Loan Interest

Before we dive into calculations, it’s crucial to establish a solid understanding of what an interest rate truly represents and the key terminology associated with it. This foundational knowledge is the bedrock upon which all subsequent calculations and financial decisions are built.

What is an Interest Rate?

At its core, an interest rate is the percentage charged by a lender to a borrower for the use of assets, typically expressed as an annual percentage of the principal outstanding. Essentially, it’s the price you pay for borrowing money and the compensation a lender receives for extending credit. This rate covers the lender’s risk, administrative costs, and their own cost of capital. A higher interest rate means a higher cost to borrow, leading to larger monthly payments and a greater total repayment over the loan term. Conversely, a lower interest rate reduces the cost of borrowing, making loans more affordable.

Why Calculating Interest Rates Matters

Understanding and calculating interest rates is paramount for several reasons. Firstly, it allows you to accurately assess the true cost of a loan, not just the principal amount. Without this understanding, you might underestimate the financial burden. Secondly, it enables you to compare different loan offers effectively. A seemingly attractive loan with a low monthly payment might hide a higher overall cost due to a longer term or hidden fees, which the interest rate calculation helps uncover. Thirdly, knowing how to figure interest helps in budgeting and financial planning, ensuring you can comfortably afford the repayments without jeopardizing your other financial goals. It empowers you to be a proactive participant in your financial journey, rather than a passive recipient of loan terms.

Key Terminology: Principal, Term, APR, and Fees

To accurately calculate and comprehend loan interest, a grasp of specific financial terms is essential:

- Principal: This is the initial amount of money borrowed or the outstanding balance of a loan, on which interest is calculated. As you make payments, a portion goes towards the principal, reducing the base on which future interest is charged.

- Term: The loan term is the agreed-upon duration over which the loan will be repaid. It can range from a few months for short-term personal loans to 15, 30, or even 40 years for mortgages. A longer term often means lower monthly payments but typically results in more interest paid over the life of the loan.

- Annual Percentage Rate (APR): The APR is a broader measure of the cost of borrowing money than the interest rate alone. It includes not only the nominal interest rate but also any additional fees or charges associated with the loan, such as origination fees, closing costs, or discount points. The APR is expressed as an annual percentage and is designed to provide a more comprehensive, standardized way to compare the true cost of different loans. It is often a better comparison tool than just the stated interest rate.

- Fees: Beyond the interest rate, many loans come with various fees. These can include application fees, origination fees (charged by the lender for processing the loan), late payment fees, prepayment penalties (charged if you pay off the loan early), and closing costs (for mortgages). These fees contribute to the overall cost of the loan and are often factored into the APR.

Types of Interest Rates and Their Impact

Not all interest rates are created equal. Different types of interest calculations and rate structures can significantly alter the total cost of your loan and the predictability of your payments. Understanding these distinctions is critical for choosing the right loan product.

Simple Interest

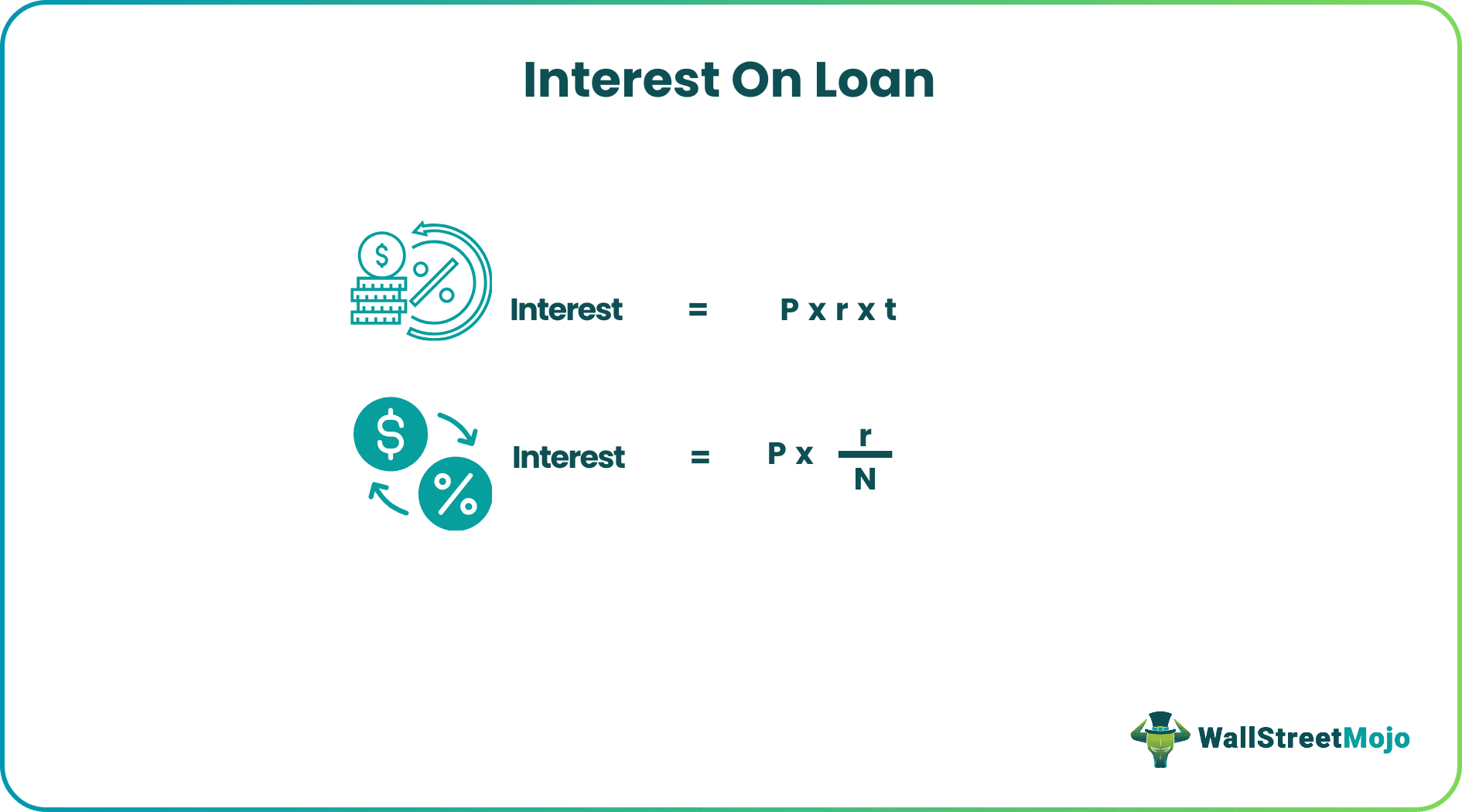

Simple interest is the most straightforward type of interest calculation. It is calculated only on the principal amount of the loan. This means the interest payment remains constant throughout the loan’s life, assuming no changes to the principal balance. Simple interest is often used for short-term loans, like some personal loans or car loans, or for specific financial instruments.

The formula for simple interest is:

Interest = Principal × Rate × Time

Where:

- Principal (P) is the initial amount borrowed.

- Rate (R) is the annual interest rate (expressed as a decimal).

- Time (T) is the loan term in years.

For example, if you borrow $10,000 at a 5% simple annual interest rate for 3 years, the interest would be: $10,000 × 0.05 × 3 = $1,500. Your total repayment would be $11,500.

Compound Interest

Compound interest is interest calculated on the initial principal and also on the accumulated interest from previous periods. This “interest on interest” effect can lead to significantly higher total repayments over time, especially for long-term loans. Most mortgages, student loans, and credit cards use compound interest. The frequency of compounding (daily, monthly, quarterly, annually) also plays a crucial role; the more frequently interest is compounded, the faster the balance grows.

While the calculation for compound interest over multiple periods can be complex, the key takeaway is that your interest burden increases as the accumulated interest is added to the principal. This is why paying down the principal quickly can save you substantial amounts in interest over the life of a compound interest loan.

Fixed vs. Variable Rates

Loan interest rates can also be categorized by their stability over time:

- Fixed-Rate Loans: With a fixed interest rate, the interest rate remains constant for the entire duration of the loan. This offers predictability in your monthly payments, making budgeting easier and shielding you from potential interest rate increases in the market. Mortgages are a common example where fixed rates are popular, offering long-term stability.

- Variable-Rate Loans (or Adjustable-Rate Loans): Variable rates, also known as adjustable-rate mortgages (ARMs) or floating rates, fluctuate based on an underlying benchmark interest rate (like the prime rate or LIBOR, though LIBOR is being phased out). This means your interest rate and monthly payments can go up or down over the loan term. While variable rates might start lower than fixed rates, they introduce an element of risk, as significant rate increases could make your payments unaffordable. They can be attractive in a declining interest rate environment but risky in a rising one.

Nominal vs. Effective Interest Rates

Understanding the difference between nominal and effective interest rates is critical for discerning the true cost of borrowing, especially when dealing with compound interest.

- Nominal Interest Rate: This is the stated or advertised annual interest rate without taking into account the effects of compounding. It’s often the rate lenders promote. For example, a loan might be advertised with a “10% nominal annual interest rate.”

- Effective Interest Rate (EIR) / Annual Equivalent Rate (AER): This is the true annual rate of interest paid on a loan, taking into account the effect of compounding over a given period. If a loan has a 10% nominal rate compounded monthly, the effective rate will be slightly higher than 10% because interest is being calculated on accrued interest throughout the year. The formula for the effective annual rate is:

EIR = (1 + (Nominal Rate / Number of Compounding Periods))^Number of Compounding Periods – 1

The EIR provides a more accurate comparison of different loan products, particularly when they have different compounding frequencies.

Manual Methods for Calculating Loan Interest

While modern financial tools can automate complex calculations, understanding the manual methods provides valuable insight into how interest accrues. These methods are particularly useful for simple interest loans or for estimating interest over shorter periods.

Simple Interest Calculation: The Foundation

As discussed, the calculation for simple interest is straightforward: Interest = Principal × Rate × Time. Let’s apply this to a practical scenario.

Suppose you take out a personal loan of $5,000 at a simple annual interest rate of 6% for 2 years.

- Principal (P) = $5,000

- Rate (R) = 0.06 (6% expressed as a decimal)

- Time (T) = 2 years

- Interest = $5,000 × 0.06 × 2 = $600

Your total repayment would be $5,000 (principal) + $600 (interest) = $5,600. To find your monthly payment, you would divide the total repayment by the total number of months: $5,600 / (2 years * 12 months/year) = $5,600 / 24 = $233.33 per month.

Estimating Monthly Payments and Total Interest

For loans with compound interest, manually calculating exact monthly payments can be more involved, often requiring financial calculators or formulas. However, you can make reasonable estimates for the total interest paid over time. A key concept here is amortization. An amortization schedule details each payment made over the life of a loan, showing how much goes towards interest and how much towards the principal. In the early stages of an amortized loan (like a mortgage), a larger portion of your monthly payment goes towards interest, and a smaller portion towards the principal. As the principal balance decreases, less interest accrues, and a greater portion of subsequent payments goes to reducing the principal.

A rough estimate for total interest on a long-term loan can be made by multiplying the estimated monthly payment by the total number of payments and then subtracting the original principal. For example, if a 30-year, $200,000 mortgage at 4% has a monthly payment of approximately $955, the total paid would be $955 * 360 months = $343,800. The total interest paid would be $343,800 – $200,000 = $143,800. This approximation doesn’t break down the exact interest paid per month but gives a solid estimate of the overall interest burden.

The Importance of Loan Amortization Schedules

While calculating each payment manually for a complex, compound interest loan is impractical, understanding the concept of an amortization schedule is crucial. An amortization schedule reveals:

- Payment Breakdown: For each payment, it shows the exact amount applied to interest and the amount applied to the principal.

- Principal Reduction: It illustrates how the outstanding principal balance decreases over time.

- Total Cost: It sums up the total interest paid over the life of the loan.

Lenders typically provide an amortization schedule with your loan documents. If not, numerous online calculators can generate one for you. Reviewing this schedule helps you visualize the true cost of your loan and understand the impact of additional payments towards the principal, which can significantly reduce total interest paid.

Leveraging Formulas and Tools for Accuracy

For most real-world loan scenarios, especially those involving compound interest and fixed monthly payments, relying on specific financial formulas or readily available digital tools is the most accurate and efficient approach.

Using the Loan Payment Formula

The standard loan payment formula, often referred to as the amortization formula, allows you to calculate the fixed monthly payment for a loan based on the principal, interest rate, and term. This formula is fundamental for anyone looking to understand their repayment obligations.

The formula for calculating a fixed monthly loan payment (PMT) is:

PMT = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- PMT = Monthly payment

- P = Principal loan amount

- i = Monthly interest rate (annual rate divided by 12, expressed as a decimal)

- n = Total number of payments (loan term in years multiplied by 12)

Let’s illustrate with an example: A $15,000 car loan at an annual interest rate of 4.5% over 5 years.

- P = $15,000

- i = 0.045 / 12 = 0.00375

- n = 5 years × 12 months/year = 60 months

Plugging these values into the formula:

PMT = 15000 [ 0.00375(1 + 0.00375)^60 ] / [ (1 + 0.00375)^60 – 1]

PMT ≈ $280.60

Once you have the monthly payment, you can easily figure the total amount paid ($280.60 × 60 = $16,836) and the total interest paid ($16,836 – $15,000 = $1,836). While this formula is precise, its manual calculation can be tedious.

Online Calculators and Spreadsheets

Fortunately, you don’t need to be a math whiz to apply these formulas. The internet is brimming with free, user-friendly loan calculators that automate these calculations. Websites of banks, credit unions, and financial education platforms typically offer robust loan calculators where you simply input the principal, interest rate, and term, and it instantly provides the monthly payment, total interest, and often an amortization schedule.

Spreadsheet software like Microsoft Excel or Google Sheets also provides powerful functions for loan calculations. The PMT function, for instance, can quickly calculate your monthly payment:

=PMT(rate, nper, pv, [fv], [type])

Where:

rate: The interest rate per period (e.g., annual rate / 12).nper: The total number of payments for the loan (e.g., years * 12).pv: The present value, or the total amount that a series of future payments is worth now; also known as the principal.

Using these tools not only saves time but also reduces the chance of calculation errors, allowing you to quickly compare multiple loan scenarios.

The Role of Annual Percentage Rate (APR) in Comparisons

While the formulas above help you figure out the nominal interest rate’s impact, remember the importance of APR for comprehensive loan comparison. As mentioned, the APR includes the nominal interest rate plus any additional fees, giving you a more accurate picture of the total cost of borrowing. When comparing loan offers from different lenders, always look at the APR rather than just the stated interest rate. A loan with a slightly lower nominal interest rate but higher fees might end up having a higher APR, meaning it’s ultimately more expensive. By focusing on APR, you ensure an apples-to-apples comparison, making an informed decision based on the true cost of credit.

Beyond the Calculation: Factors Influencing Your Rate

While understanding how to calculate interest is crucial, it’s equally important to know why you receive a particular interest rate. Numerous factors influence the rate a lender offers you, and being aware of these can help you secure more favorable terms.

Credit Score and History

Your credit score is arguably the most significant factor determining the interest rate you’ll be offered. Lenders use credit scores (like FICO or VantageScore) to assess your creditworthiness and the likelihood that you’ll repay your loan. A higher credit score (typically above 740) indicates a lower risk to lenders, which usually translates into lower interest rates. Conversely, a lower credit score suggests a higher risk, leading to higher interest rates to compensate the lender for that increased risk. Building and maintaining a strong credit history through timely payments and responsible credit utilization is paramount for accessing the best loan rates.

Loan Type and Lender

The type of loan you seek also plays a critical role. Secured loans, such as mortgages or auto loans, are backed by an asset (collateral) that the lender can seize if you default. Because the lender’s risk is lower, secured loans generally come with lower interest rates than unsecured loans, like personal loans or credit cards, which have no collateral.

Furthermore, the type of lender can influence rates. Traditional banks, credit unions, and online lenders each have different business models, overheads, and risk appetites, leading to varying rate offerings. Credit unions, for instance, being member-owned non-profits, often provide more competitive rates to their members.

Market Conditions and Economic Factors

Broader economic conditions significantly impact interest rates. The Federal Reserve’s monetary policy, specifically its target for the federal funds rate, directly influences borrowing costs across the economy. When the Fed raises rates, borrowing becomes more expensive for banks, and these costs are passed on to consumers. Conversely, rate cuts typically lead to lower loan interest rates. Inflation, economic growth, and the overall stability of financial markets also play a role. In periods of high inflation, lenders may charge higher rates to ensure the real value of their returns is preserved.

Negotiating Your Interest Rate

While many factors are outside your immediate control, there’s often room to negotiate your interest rate, especially for larger loans.

- Shop Around: Don’t accept the first offer. Apply to multiple lenders (within a short timeframe to minimize impact on your credit score) and compare their APRs. Use competing offers as leverage.

- Improve Your Credit Score: Before applying for a loan, take steps to improve your credit score. Pay down existing debt, correct any errors on your credit report, and avoid opening new credit accounts.

- Offer a Down Payment or Collateral: For unsecured loans, offering to secure it with an asset (if possible) could lower your rate. For secured loans, a larger down payment reduces the principal, thus reducing the lender’s risk and potentially lowering your rate.

- Shorten the Loan Term: While it means higher monthly payments, a shorter loan term often comes with a lower interest rate, as the lender’s money is tied up for a shorter period.

- Ask for Discounts: Some lenders offer discounts for existing customers, setting up auto-pay, or having a certain type of account with them. It never hurts to ask!

Conclusion

Understanding how to figure the interest rate on a loan is an essential skill in personal finance. It transforms what might seem like an abstract percentage into a tangible financial commitment, revealing the true cost of borrowing. From the basic principles of simple and compound interest to the nuances of APR and the influential factors like your credit score and market conditions, each piece of this puzzle contributes to a complete picture of your loan.

By diligently applying the formulas, leveraging online calculators, and critically evaluating the APR of different offers, you empower yourself to make informed decisions. Remember that a lower interest rate can save you thousands of dollars over the life of a loan, freeing up capital for other financial goals. Don’t be passive in your borrowing journey; be an active participant, armed with knowledge and the ability to calculate, compare, and ultimately choose the loan that best serves your financial well-being. The knowledge gained here is not just about numbers; it’s about financial freedom and control.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.