In the realm of finance, percentages are more than just numbers on a page; they are the fundamental language of growth, risk, and value. Whether you are a small business owner calculating profit margins, an investor tracking portfolio performance, or a consumer trying to understand the impact of inflation on your purchasing power, knowing how to accurately add percentages is an essential skill.

While the concept might seem elementary at first glance, adding percentages in a financial context is rarely as simple as adding two integers. Depending on whether you are dealing with sales tax, cumulative investment returns, or year-over-year growth, the methodology changes significantly. This guide explores the professional nuances of percentage addition, ensuring you have the mathematical precision required to manage your money effectively.

Understanding the Fundamentals: Why Percentages Matter in Your Financial Life

Before diving into complex formulas, it is crucial to establish a baseline for how percentages function within a financial framework. A percentage represents a fraction of 100, acting as a relative measure rather than an absolute one. In money management, this relativity is what allows us to compare a small-cap stock’s growth to a large-cap dividend, even when the dollar amounts differ vastly.

The Difference Between Absolute Values and Relative Growth

The most common mistake in financial calculations is treating percentage points as absolute values. For instance, if your savings account interest rate rises from 1% to 2%, it has increased by one percentage point, but it has actually grown by 100% in terms of its relative value.

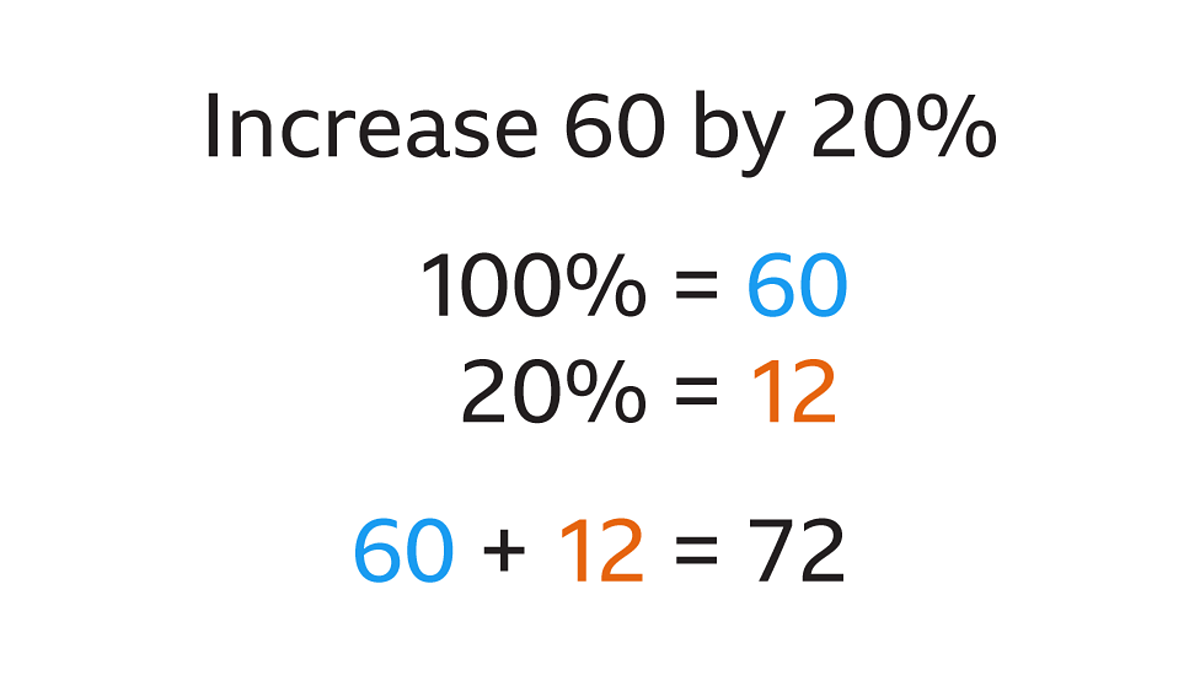

When we talk about “adding” a percentage to a financial figure, we are usually performing an “increase” operation. If a consultant tells you they are adding a 15% service fee to a $1,000 invoice, they aren’t adding the number 15; they are adding 15% of the base value. Understanding this distinction is the first step toward financial literacy. It prevents errors in budgeting and ensures that when you see a “5% increase” in expenses, you can immediately translate that into the actual impact on your cash flow.

Decimal Conversions: The First Step to Accuracy

To perform any professional-grade financial calculation, you must first convert percentages into decimals. This reduces the risk of “zero-tracking” errors and makes it easier to use digital tools like Excel or financial calculators.

To convert a percentage to a decimal, you simply divide by 100 or move the decimal point two places to the left. For example:

- 5% becomes 0.05

- 25.5% becomes 0.255

- 110% becomes 1.10

In the context of “adding” a percentage to a base amount, the most efficient way to think about it is using the “1 + r” method, where “r” is the decimal form of the percentage. If you are adding a 7% tax to a purchase, you are essentially multiplying the base by 1.07. This streamlined approach is the standard in business finance because it combines the addition and the calculation into a single, elegant step.

Adding Percentages to Principal: Calculating Sales Tax, Tips, and Fees

In daily personal finance, the most frequent application of adding percentages occurs at the point of sale. Whether it’s adding a gratuity at a restaurant or calculating the total cost of an item including VAT or sales tax, these calculations affect your daily liquidity.

The Multiplier Method for Instant Calculations

The most professional way to add a percentage to a base amount is the multiplier method. This is particularly useful for business owners who need to provide instant quotes or for individuals managing a strict budget.

The formula is: Total = Principal × (1 + Percentage as a Decimal)

Consider a business purchasing $5,000 worth of equipment with an 8.5% sales tax. Instead of calculating 8.5% of $5,000 ($425) and then adding it back to the original amount, you simply multiply $5,000 by 1.085. The result, $5,425, is achieved in one step. This method is less prone to “copy-paste” errors in spreadsheets and provides a clearer picture of the total capital outflow required for an acquisition.

Managing Cumulative Percentage Increases in Consumer Spending

Sometimes, you aren’t just adding one percentage; you are adding multiple layers of percentages. A common scenario in high-end services or international business is the application of a service charge followed by a government tax.

It is vital to know if these percentages are “additive” or “compounded.” If they are additive, you add the percentages together first (e.g., 10% service + 5% tax = 15% total). If they are compounded (tax applied on top of the service charge), the math changes. Professional financial planning always assumes the most conservative (higher) cost, meaning you should be prepared for the compounding effect where the second percentage is calculated based on the new, higher subtotal.

The Power of Compounding: Adding Interest Percentages Over Time

When we move from spending money to growing it, “adding” percentages takes on a whole new meaning. In investing, we often talk about annual returns. However, adding a 10% return in Year 1 and a 10% return in Year 2 does not result in a total 20% gain. It results in a 21% gain. This is the magic—and the math—of compounding.

Simple vs. Compound Interest: A Mathematical Distinction

Simple interest is calculated only on the principal amount. If you have $10,000 at 5% simple interest, you “add” $500 every year. The percentage added remains static because the base does not change.

Compound interest, however, is the standard for modern investing and high-yield savings. Here, the percentage is added to the principal plus any previously earned interest. The formula for adding these percentages over time is:

A = P(1 + r/n)^nt

Where:

- A is the final amount.

- P is the principal.

- r is the annual interest rate.

- n is the number of times interest is compounded per year.

- t is the number of years.

In this context, “adding” a percentage is a recursive process. For a financial professional, understanding that adding 5% annually for 10 years is vastly different from adding 50% once is the key to long-term wealth projection.

Using the Rule of 72 to Forecast Growth

A useful mental shortcut for adding percentages over time is the “Rule of 72.” This is a quick way to estimate how long it will take for an investment to double given a fixed annual percentage increase. You simply divide 72 by the annual interest rate.

For example, if you are adding a 6% return to your portfolio annually, it will take approximately 12 years (72 / 6) for your money to double. This tool is invaluable for retirement planning and side-hustle projections, allowing you to see the “additive” power of consistent percentage growth without needing a complex calculator.

Business Finance: Adding Percentages to Margins and Markups

For entrepreneurs and business finance managers, adding percentages is a daily task that dictates the health of the company’s bottom line. However, there is a dangerous pitfall here: the confusion between markup and margin.

Profit Margin vs. Markup: Avoiding the Common Pitfall

Adding a percentage to your cost to determine a sales price is called a markup. If an item costs you $100 and you want to add a 25% markup, the price is $125.

However, if your goal is to have a 25% profit margin, adding 25% to the cost will leave you short. Margin is calculated as a percentage of the selling price, not the cost. To achieve a 25% margin on a $100 item, the formula is:

Cost / (1 – Desired Margin)

$100 / 0.75 = $133.33.

As you can see, “adding” a 25% margin requires a much higher price increase than a 25% markup. Professionals in business finance must be precise with this terminology, as a mistake here can lead to underpricing services and eroding the business’s sustainability.

Factoring in Inflation and Cost of Goods Sold (COGS)

When adding percentages to your pricing strategy, you must also account for external “additions” like inflation. If inflation is at 4% and your shipping costs have increased by 10%, you cannot simply add 14% to your prices and expect to maintain the same profit levels.

Each component of your cost structure must be weighted. Adding percentages in a business environment often requires a “Weighted Average” approach. If 60% of your costs stayed the same and 40% increased by 10%, your total cost base has only increased by 4% (0.40 × 0.10). Mastery of these additive properties allows for strategic price adjustments that remain competitive while protecting margins.

Advanced Financial Tools for Percentage Calculation

In the modern digital age, we rarely do these calculations by hand on the back of an envelope. Professional financial management relies on tools that handle the “adding” of percentages with 100% accuracy.

Utilizing Financial Calculators and Spreadsheet Functions

Excel and Google Sheets are the gold standard for financial percentage calculations. To add a column of percentage increases, professionals use specific functions:

- The PRODUCT Function: Used for calculating cumulative growth (e.g., adding several years of different percentage returns).

- Absolute Cell Referencing: Essential when adding a fixed percentage (like a tax rate) to a long list of different prices.

For example, if you have a list of prices in Column A and want to add a 15% markup in Column B, your formula would be =A1*1.15. This ensures that the percentage addition is applied uniformly across your entire inventory or budget.

Analyzing Portfolio Diversification and Percentage Allocation

Finally, adding percentages is critical in the context of portfolio “weighting.” In an investment portfolio, the percentages of all your assets must add up to exactly 100%. When one asset grows by 20% and another shrinks by 10%, your total “pie” has shifted.

“Adding” percentages here refers to rebalancing—the process of selling a portion of an asset that has grown too large and adding to an asset that has become a smaller percentage of your total wealth. This ensures that your risk exposure remains aligned with your financial goals. By viewing percentage addition as a tool for balance rather than just growth, you create a more resilient financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.