For most Americans, Social Security represents the bedrock of their retirement strategy. Yet, despite its importance, the system remains a “black box” for many. Understanding how to estimate your future benefits is not merely an exercise in curiosity; it is a critical component of professional financial planning. Whether you are decades away from retirement or standing on the threshold, knowing how the Social Security Administration (SSA) calculates your checks allows you to make informed decisions about your savings, investments, and the timing of your departure from the workforce.

In this guide, we will deconstruct the mechanics of Social Security calculations, explore the tools available for estimation, and analyze the strategic variables that can significantly increase your lifetime payout.

Understanding the Foundation of Social Security Calculations

Before you can estimate your benefits, you must understand the underlying math the government uses. Unlike a private savings account, Social Security is a “defined benefit” system based on your career earnings history. The SSA does not simply look at your last paycheck; it looks at your entire professional life.

The Role of Work Credits and Eligibility

To qualify for Social Security retirement benefits, you must first earn enough “credits.” As of the current regulations, you need 40 credits to be eligible, which typically equates to 10 years of work. You can earn a maximum of four credits per year, and the income threshold to earn a credit is relatively low, ensuring that even part-time or seasonal workers can eventually qualify. However, qualifying is only the first step; the actual dollar amount you receive is determined by the volume of your contributions via payroll taxes (FICA).

Average Indexed Monthly Earnings (AIME)

The core of your benefit estimate lies in your Average Indexed Monthly Earnings (AIME). The SSA looks at your highest 35 years of earnings. If you worked for 40 years, they drop the lowest five. If you worked for only 25 years, the remaining 10 years are calculated as zeros, which can drastically lower your estimate.

To ensure fairness across decades, the SSA “indexes” your past earnings. This means they adjust your 1990 salary to account for inflation and general wage increases, bringing it into “today’s dollars” before averaging it. This indexing ensures that the purchasing power of your contributions is reflected in your eventual benefit.

Primary Insurance Amount (PIA) and Bend Points

Once your AIME is calculated, the SSA applies a formula to determine your Primary Insurance Amount (PIA). The PIA is the monthly sum you are entitled to if you retire exactly at your Full Retirement Age (FRA).

The formula is progressive, meaning it is designed to provide a higher “replacement rate” for lower-income earners than for high-income earners. The SSA uses “bend points”—specific dollar thresholds—to apply different percentages to your AIME. For example, you might receive 90% of the first few hundred dollars of your AIME, but only 15% of the earnings above a certain high-level threshold. Estimating these bend points is essential for high-earning professionals who may realize that Social Security will only replace a small fraction of their pre-retirement income.

Key Factors That Influence Your Monthly Payout

An estimate is not a guarantee. The number you see on a statement today assumes certain behaviors and external factors. To get an accurate picture of your financial future, you must account for the variables that the SSA formula uses to adjust your PIA.

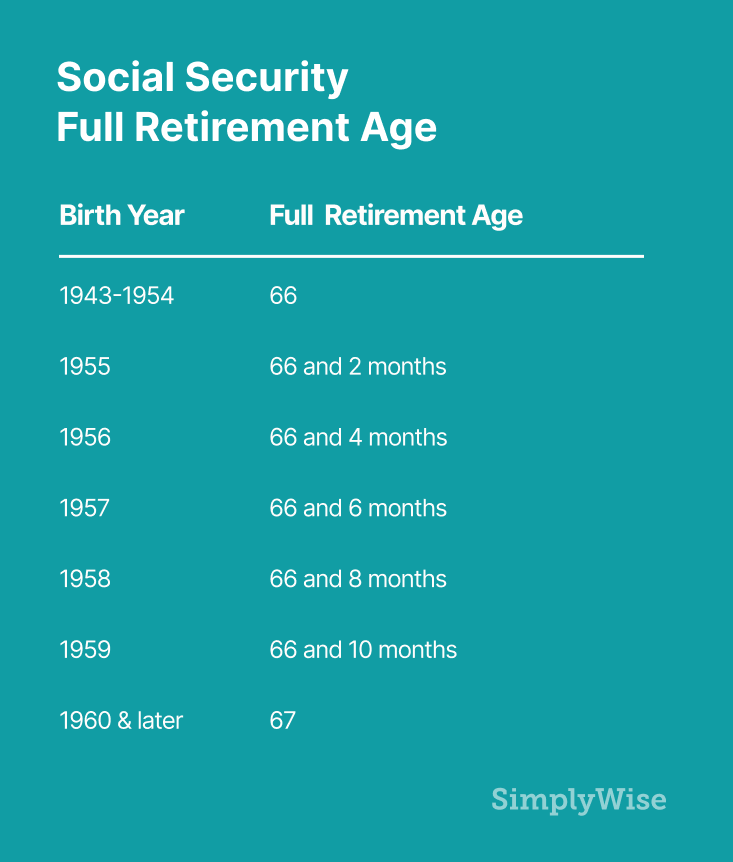

The Impact of Full Retirement Age (FRA)

Your Full Retirement Age is the most important milestone in your estimation process. For those born in 1960 or later, the FRA is 67. If you were born earlier, it may be 66 and a few months. Claiming benefits exactly at your FRA ensures you receive 100% of your calculated PIA. If you estimate your benefits based on an FRA of 67 but decide to retire at 64, your actual check will be significantly lower than the initial estimate.

Early vs. Delayed Claiming Strategies

The window for claiming Social Security opens at age 62 and stays open indefinitely, though the financial incentives stop increasing at age 70.

- Early Claiming: If you claim at 62, your benefit is permanently reduced by up to 30%. This is an actuarial reduction designed to account for the fact that you will receive checks for a longer period.

- Delayed Claiming: For every year you delay claiming past your FRA (up until age 70), your benefit increases by approximately 8% per year. This “Delayed Retirement Credit” is one of the most powerful tools in personal finance. A person with an FRA of 67 who waits until 70 to claim will receive 124% of their PIA for the rest of their life. When estimating, you must run “what-if” scenarios for ages 62, 67, and 70 to see the massive variance in potential income.

The Cost-of-Living Adjustment (COLA)

Social Security is one of the few retirement income sources that is inflation-protected. Every year, the SSA evaluates the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If inflation has risen, your benefit estimate will increase via a Cost-of-Living Adjustment (COLA). When performing long-term estimates, professionals often factor in a conservative annual COLA of 2-3% to understand how their purchasing power might hold up over a 30-year retirement.

Digital Tools and Methods to Estimate Your Benefits

Gone are the days of waiting for a paper statement to arrive in the mail once a year. The modern investor has several high-tech and high-touch methods to generate a precise estimate.

Using the “my Social Security” Account

The most accurate way to estimate your benefit is to go directly to the source. Creating a “my Social Security” account on the SSA.gov website allows you to view your actual earnings history. This is vital because if the SSA has an error in your record—such as a missing year of income from a decade ago—your estimate will be wrong. The portal provides a “Retirement Calculator” that pulls your real data and allows you to toggle your future salary and your expected retirement age to see real-time updates to your projected monthly check.

The SSA Quick Calculator vs. Detailed Calculator

For those who do not want to create an account or are helping a family member, the SSA offers two web-based tools:

- The Quick Calculator: This requires only your date of birth and current earnings. It provides a rough estimate based on average wage growth. It is helpful for a “ballpark” figure but lacks the nuance of an official statement.

- The Detailed Calculator: This is a downloadable software program used by financial planners. It allows for the input of complex variables, such as periods of self-employment, government work not covered by Social Security (Windfall Elimination Provision), and specific tax scenarios.

Third-Party Financial Planning Software

Many personal finance apps and professional wealth management platforms (such as RightCapital or eMoney) integrate Social Security estimation into a broader “financial plan.” These tools are superior for estimation because they don’t look at Social Security in a vacuum. They calculate how your Social Security income interacts with your 401(k) withdrawals, RMDs (Required Minimum Distributions), and brokerage accounts to provide a net-of-tax income projection.

Advanced Strategies for Maximizing Your Social Security Check

Estimating the number is only half the battle; the other half is optimizing it. In the realm of personal finance, there are nuances that can add hundreds of thousands of dollars to a household’s lifetime wealth.

Spousal and Survivor Benefit Considerations

If you are married, your estimation process is twice as complex. You are entitled to either your own benefit or 50% of your spouse’s benefit, whichever is higher. This is particularly important for households where one spouse was a high earner and the other stayed home or worked part-time. Additionally, survivor benefits allow a widowed spouse to “step into” the higher of the two checks. When estimating, couples should focus on maximizing the benefit of the higher-earning spouse (often by delaying until 70) to ensure the surviving spouse has the largest possible safety net.

Tax Implications of Social Security Income

Many people are surprised to learn that Social Security benefits can be taxable. If your “combined income” (adjusted gross income + tax-exempt interest + half of your Social Security benefits) exceeds $25,000 for individuals or $32,000 for couples, you will likely pay federal income tax on a portion of your benefits. When estimating your retirement budget, you must calculate the “net” benefit. If you are in a high tax bracket due to large IRA withdrawals, up to 85% of your Social Security check could be subject to taxation.

Integrating Social Security with Your Broader Portfolio

Finally, the estimate should serve as a guide for your investment allocation. In financial planning, Social Security is often viewed as a “government-backed inflation-protected annuity.” If you have a high estimated Social Security benefit, you might have a higher “risk capacity” in your investment portfolio, allowing you to hold more equities. Conversely, if your estimate shows a gap in your needed income, you may need to increase your current savings rate or consider a “bridge strategy,” where you spend down some personal assets to allow your Social Security benefit to grow via delayed claiming.

By taking the time to accurately estimate and analyze your Social Security benefits, you transform a vague future promise into a tangible financial asset. In the world of money management, clarity is power—and understanding your future Social Security check is the ultimate form of retirement clarity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.