Credit cards are an indispensable tool in modern finance, offering convenience, rewards, and security. However, with the constant flow of transactions, it’s not uncommon for errors or unauthorized activity to occur. Discovering an unfamiliar or incorrect charge on your statement can be unsettling, but understanding how to effectively dispute such a charge, particularly with a major issuer like Chase, is a crucial financial skill. This comprehensive guide will walk you through the process, empowering you to protect your finances and ensure fair billing practices.

Understanding Why Disputes Arise: Common Scenarios

Before delving into the “how,” it’s vital to recognize the various situations that typically necessitate a credit card dispute. Identifying the nature of the issue will guide your approach and strengthen your case.

Unauthorized Transactions: The Threat of Fraud

Perhaps the most alarming reason to dispute a charge is fraud. This category includes transactions you did not authorize, which often stem from:

- Stolen Physical Cards: If your card is lost or stolen and used by someone else.

- Compromised Card Numbers: When your card details are illegally obtained and used for online or in-person purchases without the physical card.

- Identity Theft: More severe cases where criminals open accounts or make charges under your identity.

In these instances, immediate action is paramount to limit your liability and protect your credit score. Federal law, specifically the Fair Credit Billing Act (FCBA) and the Electronic Fund Transfer Act (EFTA), offers significant protections against unauthorized charges, limiting your liability to as little as $0 if reported promptly.

Billing Errors: Mistakes Happen

Not all disputes involve malicious intent. Often, charges appear on your statement due to genuine administrative or technical errors. These can include:

- Incorrect Amounts: A charge for a different amount than what you agreed to pay.

- Duplicate Charges: Being billed twice for the same transaction.

- Charges for Returned Items: A charge appearing for an item you successfully returned and were supposed to be credited for.

- Incorrect Dates or Merchant Names: While less common, these can sometimes indicate a misposted transaction or an error that requires clarification.

- Failure to Post Payments/Credits: Your payment or a credit for a return wasn’t applied to your account.

These errors, while frustrating, are typically easier to resolve, especially if you have clear documentation of the correct transaction or return.

Goods or Services Not Received or As Described: Merchant Disputes

This category often involves a disagreement with a merchant regarding a purchase. Common scenarios include:

- Undelivered Purchases: You paid for an item or service but never received it.

- Defective or Damaged Goods: The product you received was faulty or damaged upon arrival, and the merchant refuses to rectify the situation.

- Services Not Performed: You paid for a service that was never rendered or was performed unsatisfactorily, contrary to what was promised.

- Misrepresentation: The product or service you received was significantly different from its description or what was advertised.

- Subscription Issues: Being charged for a subscription you cancelled or never authorized.

In these cases, the dispute usually arises after an attempt to resolve the issue directly with the merchant has failed. Documenting your communication and their refusal to cooperate is crucial for your dispute.

The Chase Credit Card Dispute Process: Step-by-Step

Disputing a charge with Chase is a structured process designed to investigate your claim thoroughly. Following the correct steps can significantly improve your chances of a swift and successful resolution.

Gather Your Documentation: Build a Strong Case

Before contacting Chase, compile all relevant information related to the disputed charge. This is the foundation of your claim.

- Credit Card Statement: Highlight the specific charge(s) you are disputing.

- Receipts or Invoices: Proof of purchase, showing the correct amount, date, and merchant.

- Communication with Merchant: Emails, chat logs, call summaries, or letters exchanged with the merchant regarding the issue.

- Evidence of Non-Delivery/Damage: Tracking numbers, photos of damaged goods, confirmation of failed delivery attempts.

- Cancellation Confirmation: If disputing a subscription, proof of cancellation.

- Any Other Supporting Information: Anything that validates your claim, such as screenshots of product descriptions or advertisements.

The more detailed and organized your documentation, the clearer your case will be for Chase’s investigators.

Contact Chase Promptly: Time is of the Essence

Federal law, specifically the FCBA, requires you to notify your creditor of a billing error within 60 days after the first bill containing the error was sent to you. While Chase may sometimes accept disputes beyond this window, acting quickly is always in your best interest.

You have several ways to contact Chase:

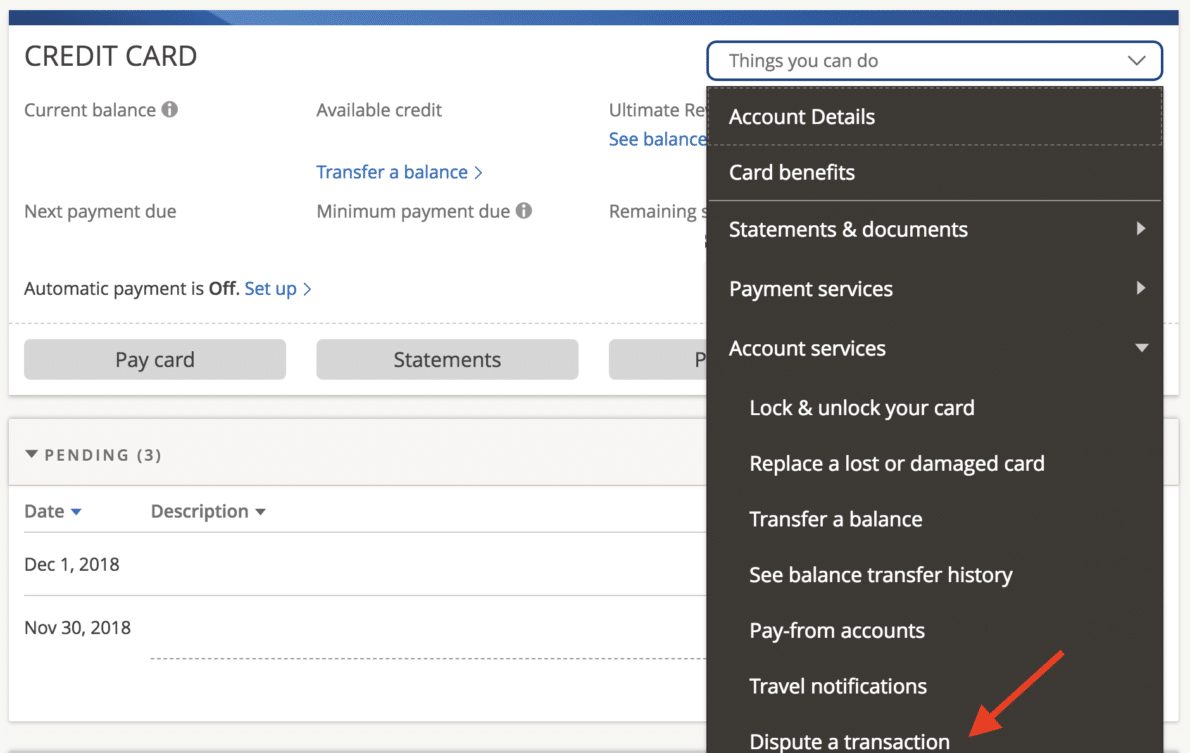

- Online: Log in to your Chase account. Many charges will have an option to “Dispute Charge” directly next to them on your transaction history. This is often the quickest and most convenient method.

- Phone: Call the customer service number on the back of your credit card. Be prepared to explain your situation clearly and provide all gathered documentation if requested. Make sure to note the date, time, and name of the representative you spoke with.

- Written Correspondence: While slower, a written letter allows you to detail your claim comprehensively and create a physical record. Send it via certified mail with a return receipt requested to Chase’s billing error address (found on your statement or website). This is often recommended for more complex disputes or if you want definitive proof of timely notification.

Clearly State Your Case: Precision Matters

Regardless of the method you choose, clearly articulate the following:

- Your account number.

- The specific charge(s) being disputed (date, amount, merchant name).

- The reason for the dispute (e.g., “unauthorized transaction,” “duplicate charge,” “goods not received”).

- Any steps you’ve already taken to resolve the issue with the merchant.

- A request for any temporary credits or reversals.

Be factual and concise. Avoid emotional language; stick to the objective details of the situation.

Follow Up and Respond: Maintain Engagement

Once you initiate a dispute, Chase will typically acknowledge your claim within 30 days. They will then conduct an investigation, which can take up to two billing cycles (approximately 90 days). During this period:

- Monitor Your Account: Keep an eye on your statement for any temporary credits applied to your account while the investigation is ongoing.

- Respond to Requests: Chase may request additional information or documentation. Respond promptly to these requests to avoid delays or the closure of your dispute.

- Keep Records: Maintain a log of all communications with Chase, including dates, times, and summaries of conversations.

Chase will inform you of their decision in writing. If they rule in your favor, the charge will be permanently removed. If they deny your claim, they must explain why and provide copies of any supporting documents they used in their decision.

Key Regulations and Your Rights as a Consumer

Understanding the legal framework that underpins credit card disputes can provide confidence and clarity during the process.

The Fair Credit Billing Act (FCBA): Your Shield

The FCBA is a federal law designed to protect consumers from unfair billing practices for open-end credit accounts, such as credit cards. It provides specific rights related to “billing errors,” which encompass more than just mathematical mistakes. Under the FCBA, a “billing error” includes:

- Unauthorized charges.

- Charges for goods or services you didn’t accept or that weren’t delivered as agreed.

- Math errors.

- Failure to properly credit payments or returns.

- Errors in account statements (e.g., wrong date, missing details).

Crucially, the FCBA dictates the timelines and procedures that creditors must follow when you dispute a charge.

Timelines and Deadlines: Act Decisively

As mentioned, you must send written notification of a billing error to your credit card company within 60 days after the first bill containing the error was mailed to you. Chase, like other issuers, adheres to this. For unauthorized charges (fraud), many card issuers have a “zero liability” policy, which often waives the 60-day rule for immediate reporting. However, for non-fraudulent billing errors, adhering to the 60-day window is critical.

Once you report an error, the credit card company must:

- Acknowledge your complaint in writing within 30 days.

- Investigate the error and resolve the dispute within two billing cycles (but no more than 90 days).

During the investigation, you are not required to pay the disputed amount (or any interest/finance charges on it), although you must pay the undisputed portions of your bill.

Temporary Credits and Investigations: What to Expect

When you initiate a dispute under the FCBA, especially for billing errors, Chase will often provide a temporary credit to your account for the disputed amount. This credit remains on your account while the investigation is underway. If Chase rules in your favor, the credit becomes permanent. If they find the charge to be valid, the temporary credit will be reversed, and you will be responsible for paying the original charge, potentially with accumulated interest if the payment due date passed.

The investigation process involves Chase contacting the merchant to gather their side of the story and any supporting documentation. This is why having your own robust documentation is so important – it provides a counter-narrative to any claims the merchant might make.

Maximizing Your Chances of a Successful Dispute

While the process is structured, there are strategies you can employ to strengthen your position and increase the likelihood of a favorable outcome.

Proactive Communication with the Merchant: Resolve Directly First

For non-fraudulent disputes (like “goods not received” or “billing errors”), it’s often advisable to attempt to resolve the issue directly with the merchant first. This demonstrates good faith and can sometimes lead to a quicker resolution without involving your credit card company.

- Contact Merchant Customer Service: Explain the problem clearly and request a refund or correction.

- Provide Documentation: Offer any relevant proof (receipts, photos, emails).

- Set a Deadline: If they promise a resolution, ask for a timeline.

- Document Everything: Keep a detailed record of these interactions, including dates, times, names of representatives, and what was discussed. If the merchant fails to resolve the issue, this documentation becomes powerful evidence for your dispute with Chase.

Chase often prefers that you attempt to resolve with the merchant first, especially for service-related disputes, before escalating to a formal chargeback.

Maintain Detailed Records: Your Personal Audit Trail

Beyond the initial documentation, maintaining a meticulous log throughout the dispute process is paramount. This includes:

- Date and Time of Calls: With whom you spoke at Chase or the merchant.

- Summary of Discussions: Key points, agreements, or disagreements.

- Reference Numbers: Any case or dispute numbers provided by Chase.

- Copies of All Correspondence: Emails, letters sent and received.

This comprehensive log serves as your personal audit trail, proving when and how you acted, which can be invaluable if there are any discrepancies or further issues down the line.

Understanding Different Types of Disputes: Fraud vs. Merchant Error

It’s crucial to understand that Chase treats fraud disputes differently from merchant-related billing errors.

- Fraud: For clear cases of unauthorized use, Chase’s fraud department is equipped to act swiftly, often immediately cancelling the card and issuing a new one, and then crediting your account. These disputes often have higher success rates due to strong consumer protection laws.

- Merchant Error/Service Disputes: These involve a more detailed investigation as Chase acts as an impartial arbiter, reviewing evidence from both you and the merchant. The outcome here heavily relies on the strength of your evidence and the clarity of the contractual agreement (what you were promised vs. what you received).

When you contact Chase, be clear about whether you believe the charge is fraudulent or a legitimate charge with a billing error/service issue, as this directs your case to the appropriate team and process.

Preventing Future Disputes and Protecting Your Finances

While knowing how to dispute a charge is essential, prevention is always better than cure. Adopting proactive financial habits can significantly reduce your chances of needing to dispute charges in the first place.

Monitor Your Statements Regularly: Early Detection is Key

Make it a habit to review your credit card statements, both online and paper, as soon as they become available. Don’t wait until the due date.

- Daily or Weekly Checks: A quick glance at your online activity can catch fraudulent charges within hours, allowing for immediate action.

- Reconcile Purchases: Compare your receipts with posted transactions to ensure accuracy.

- Look for Small or Odd Charges: Fraudsters often test stolen card numbers with small, inconspicuous charges before attempting larger purchases.

Early detection allows you to report issues within the critical 60-day window and often prevents larger financial losses.

Use Secure Payment Methods: Fortify Your Transactions

Embrace technology and practices that enhance the security of your transactions:

- Digital Wallets (Apple Pay, Google Pay): These services tokenize your card number, meaning the merchant never sees your actual card details, reducing the risk of compromise.

- One-Time Use Virtual Card Numbers: Some financial institutions (including Chase for certain cards/accounts via their “Shop Safe” feature in the past, or similar third-party services) offer virtual card numbers that can be used for single online transactions or expire after a short period, minimizing exposure.

- Secure Websites (HTTPS): Always ensure that websites where you make purchases use “https://” in their URL, indicating an encrypted connection.

- Strong, Unique Passwords: For all your online shopping accounts and banking portals.

Be Wary of Suspicious Transactions: Recognize Red Flags

Cultivate a healthy skepticism about unusual financial requests or situations:

- Unsolicited Emails/Calls: Be cautious of requests for personal or financial information from unknown sources.

- Too-Good-To-Be-True Offers: Scammers often lure victims with improbable deals.

- Public Wi-Fi: Avoid making sensitive transactions (like banking or shopping) on unsecured public Wi-Fi networks.

- Unfamiliar Merchants: Research unfamiliar online stores before making a purchase. Check reviews and look for contact information.

![]()

Understanding Chargeback Rights: A Last Resort

A credit card dispute, particularly for merchant-related issues, is effectively a “chargeback” request. While the FCBA protects you, understanding that merchants can also dispute your chargeback claim is important. If Chase rules against you after reviewing all evidence, you might have limited further recourse with the card issuer itself. In such scenarios, if you still believe you are right, you might need to consider small claims court or consumer protection agencies as further steps. However, by diligently following the steps outlined above, most legitimate disputes with Chase can be successfully resolved, safeguarding your financial well-being.

Navigating credit card disputes can seem daunting, but with the right knowledge and a methodical approach, you can effectively protect your financial interests. Chase, as a major financial institution, has established processes to handle these situations, and by understanding your rights and preparing thoroughly, you empower yourself to resolve any billing discrepancies with confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.