The journey to financial prosperity is paved with many principles, but few are as powerful and foundational as compound interest. Often referred to as the “eighth wonder of the world” by Albert Einstein, compound interest is the engine that drives wealth accumulation over time. Understanding how to compute it isn’t just an academic exercise; it’s a critical skill for anyone looking to make informed decisions about their savings, investments, and long-term financial planning. This comprehensive guide will demystify compound interest, walk you through its computation, and reveal strategies to harness its incredible potential for your financial future.

Understanding the Power of Compound Interest

At its core, compound interest is the interest you earn on interest. It’s a concept that distinguishes itself sharply from simple interest, which is calculated only on the initial principal amount. The magic of compounding lies in its snowball effect: your earnings begin to generate their own earnings, leading to exponential growth that accelerates over time.

What is Compound Interest?

Imagine you deposit money into a savings account or make an investment. With simple interest, the interest you earn each period (e.g., annually) is always based solely on your original deposit. So, if you invest $1,000 at a 5% simple interest rate, you’d earn $50 every year, and your principal would remain $1,000. After ten years, you’d have your original $1,000 plus $500 in interest ($50 x 10).

Compound interest, however, works differently. In the first period, you still earn interest on your principal. But in subsequent periods, you earn interest not only on your initial principal but also on the accumulated interest from previous periods. Using the same example:

- Year 1: $1,000 principal + $50 interest (5% of $1,000) = $1,050

- Year 2: You now earn 5% interest on $1,050, which is $52.50. Your total becomes $1,102.50.

- Year 3: You earn 5% interest on $1,102.50, which is $55.13. Your total becomes $1,157.63.

This seemingly small difference quickly compounds into significant amounts over longer periods, making it a cornerstone of effective wealth building.

The Core Principle: Earning Interest on Interest

The fundamental idea is that money not only makes money, but that money then makes more money. This cyclical growth is why compound interest is so powerful. It rewards patience and consistency, transforming modest initial investments and regular contributions into substantial sums over decades. The longer your money has to grow, and the more frequently it compounds, the more pronounced this effect becomes.

Why Compound Interest is a Game-Changer for Wealth Building

For individuals striving for financial independence, compound interest is not merely a financial concept; it’s a strategic ally. It allows your money to work harder for you, reducing the burden on your active income for wealth creation. Whether you’re saving for retirement, a child’s education, a down payment on a home, or simply aiming to build a robust emergency fund, understanding and applying compound interest principles can dramatically accelerate your progress. It shifts the focus from purely adding new money to also leveraging the growth of existing money, creating a virtuous cycle of accumulation.

The Formula for Compound Interest Explained

While the concept of compound interest is intuitive, precise calculation requires a specific mathematical formula. This formula allows you to project the future value of an investment or savings account given certain parameters.

Deconstructing the Compound Interest Formula

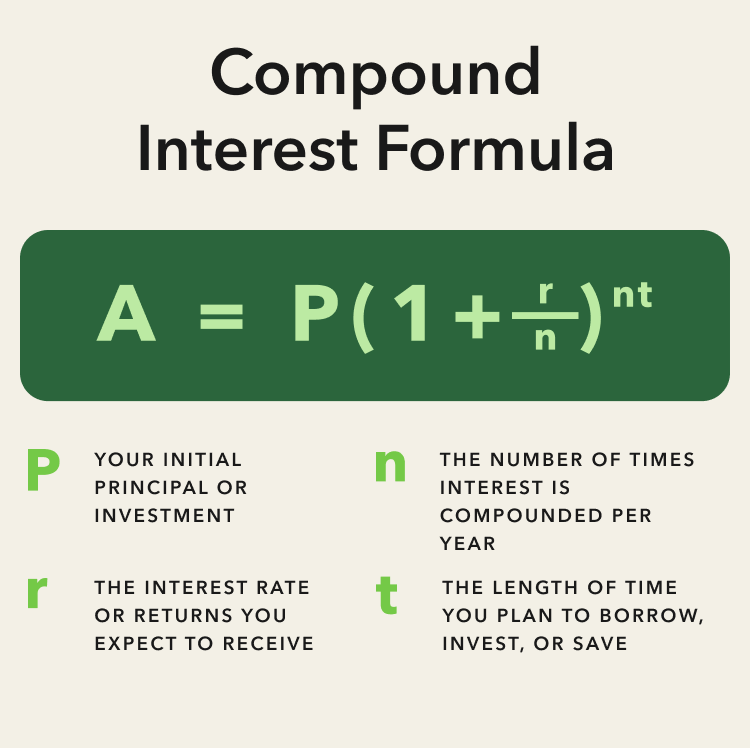

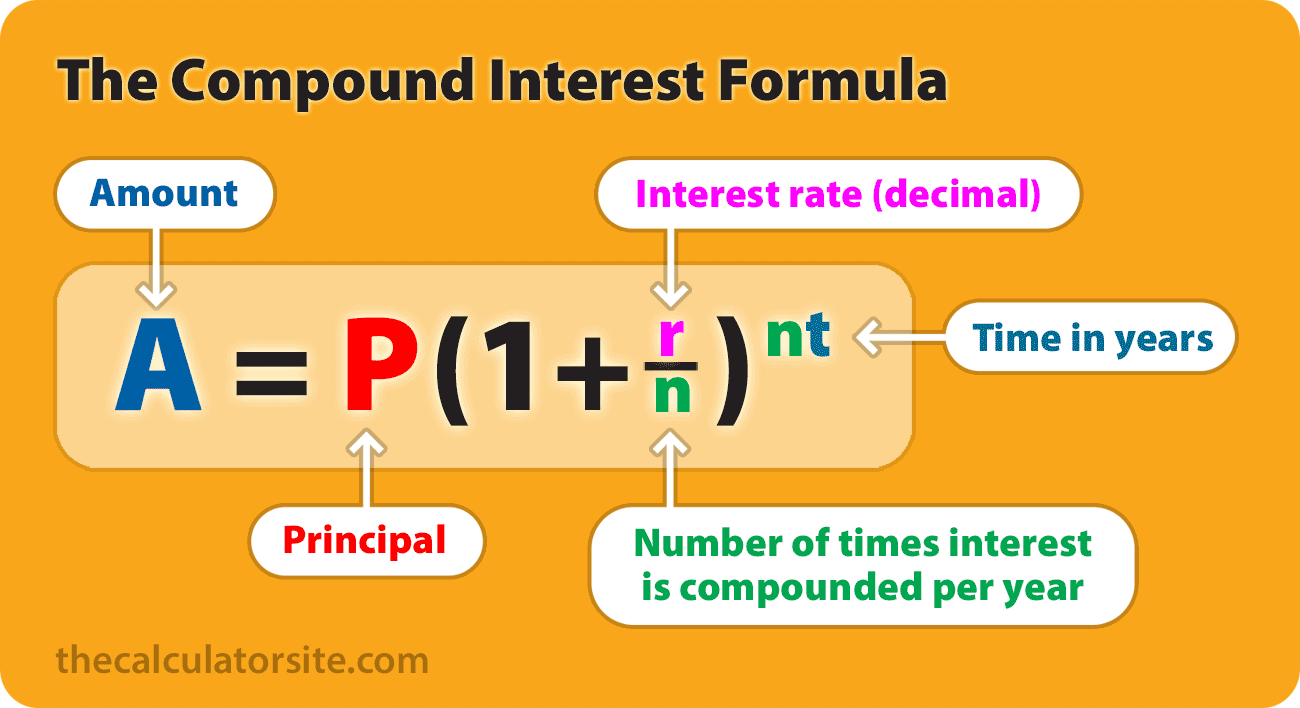

The standard formula for calculating compound interest is:

A = P (1 + r/n)^(nt)

Let’s break down each component:

- A = Future Value of the Investment/Loan, including interest. This is the total amount you will have at the end of the investment period.

- P = Principal Investment Amount (the initial deposit or loan amount). This is the starting sum of money.

- r = Annual Interest Rate (as a decimal). It’s crucial to convert the percentage rate into a decimal. For example, if the rate is 5%, you use 0.05.

- n = Number of times that interest is compounded per year. This can vary significantly:

- Annually: n = 1

- Semi-annually: n = 2

- Quarterly: n = 4

- Monthly: n = 12

- Daily: n = 365

- t = Number of years the money is invested or borrowed for.

Understanding how each variable influences the outcome is key to manipulating the formula for various financial scenarios.

Step-by-Step Calculation Example

Let’s illustrate the formula with a practical example.

Scenario 1: Annual Compounding

Suppose you invest $10,000 at an annual interest rate of 7% for 10 years, compounded annually.

- P = $10,000

- r = 0.07 (7% as a decimal)

- n = 1 (compounded annually)

- t = 10 years

Plug these values into the formula:

A = 10,000 * (1 + 0.07/1)^(1*10)

A = 10,000 * (1 + 0.07)^10

A = 10,000 * (1.07)^10

A = 10,000 * 1.96715135729

A = $19,671.51

After 10 years, your $10,000 investment would grow to $19,671.51. The interest earned is $9,671.51 ($19,671.51 – $10,000).

Scenario 2: Quarterly Compounding

Now, let’s consider the same investment, but this time, the interest is compounded quarterly.

- P = $10,000

- r = 0.07

- n = 4 (compounded quarterly)

- t = 10 years

Plug these values into the formula:

A = 10,000 * (1 + 0.07/4)^(4*10)

A = 10,000 * (1 + 0.0175)^40

A = 10,000 * (1.0175)^40

A = 10,000 * 1.99049755494

A = $19,904.98

By compounding quarterly instead of annually, your investment grows an additional $233.47 ($19,904.98 – $19,671.51) over 10 years. This demonstrates the impact of compounding frequency. The more frequently interest is compounded, the slightly higher the final amount, given the same annual rate.

Practical Applications and Tools for Computing Compound Interest

While understanding the formula is essential, in day-to-day financial planning, you don’t always need to manually crunch the numbers. A variety of tools can help you quickly compute and visualize compound interest.

Leveraging Online Calculators and Spreadsheets

For most people, online compound interest calculators are the most convenient way to estimate future growth. Websites like Investor.gov, Bankrate, or various financial planning sites offer user-friendly tools where you simply input your principal, interest rate, compounding frequency, and time horizon. These calculators instantly display the future value and total interest earned.

Spreadsheets like Microsoft Excel or Google Sheets also provide powerful capabilities. You can set up your own compound interest calculator using the FV (Future Value) function, or simply by writing out the formula using cell references. This method offers flexibility for sensitivity analysis, allowing you to easily adjust variables and see their impact. For example, FV(rate, nper, pmt, [pv], [type]) can be used, where rate is r/n, nper is n*t, pmt is for regular payments (which we aren’t using in the basic formula), and pv is your principal P (entered as a negative value since it’s an outflow).

Estimating Future Growth for Various Investments

Compound interest isn’t just for simple savings accounts. It applies to a wide range of financial instruments:

- Savings Accounts & GICs: These usually have fixed rates and compounding frequencies, making calculations straightforward.

- Stocks & Mutual Funds: While returns are not guaranteed and fluctuate, compound growth is the underlying principle. When you reinvest dividends or capital gains, you are essentially compounding your returns.

- Retirement Funds (401ks, IRAs): These vehicles are perhaps the best examples of long-term compound growth. Contributions over decades, coupled with investment returns, build substantial nest eggs.

- Real Estate: While not direct “interest,” reinvesting rental income or capital gains from property sales also leads to a compounding effect on wealth.

Using compound interest calculations helps in setting realistic financial goals and tracking progress towards them. It allows you to model different scenarios—what if I save more? What if I achieve a higher return? How much do I need to save for retirement at age 65?

The Importance of Regular Contributions

While the core formula focuses on an initial principal, in reality, many people build wealth through regular, consistent contributions (e.g., monthly savings). This introduces another layer of compounding known as dollar-cost averaging, where you invest a fixed amount at regular intervals, regardless of market fluctuations. Each new contribution starts compounding, and previous contributions continue to grow. While the formula A = P(1 + r/n)^(nt) calculates the future value of a single lump sum, for regular contributions, a more complex “future value of an annuity” formula is used, or simply building a spreadsheet model that adds each new contribution and compounds it. This combination of an initial lump sum growing and new contributions continuously being added and growing is how most people effectively maximize their compounding returns over their working lives.

Factors Influencing Compound Interest Growth

Several key factors critically influence the ultimate growth achieved through compound interest. Understanding these levers empowers you to make strategic financial decisions.

The Impact of Interest Rate

The interest rate (r) is arguably the most straightforward factor. A higher interest rate means your money grows faster. A 7% annual return will yield significantly more over time than a 3% return, even with the same principal and time frame. For instance, over 30 years, $10,000 at 3% compounded annually grows to approximately $24,273, while at 7%, it grows to about $76,123 – a difference of over $50,000. This highlights the importance of seeking out competitive interest rates for savings or prudent, growth-oriented investments, always balanced with risk tolerance.

The Significance of Time

Time (t) is the silent powerhouse behind compound interest. The longer your money has to grow, the more pronounced the compounding effect becomes. This is due to the exponential nature of the formula. The interest earned in earlier years starts earning interest itself, leading to an accelerating growth curve. This phenomenon is often referred to as the “time value of money” – a dollar today is worth more than a dollar tomorrow because of its potential to earn interest. This factor underscores the immense benefit of starting to save and invest as early as possible. A 25-year-old who invests $5,000 annually for 10 years (total $50,000) might end up with more money by age 65 than a 35-year-old who invests $5,000 annually for 30 years (total $150,000), purely because the younger investor’s money had more time to compound.

The Role of Compounding Frequency

As demonstrated in our earlier examples, the number of times interest is compounded per year (n) also affects the final amount. More frequent compounding (e.g., monthly vs. annually) leads to slightly higher returns because interest is added to the principal more often, allowing subsequent interest calculations to be based on a larger sum. While the difference between daily and monthly compounding might be minimal over a short period, it adds up over decades. When evaluating financial products, always look for those with higher compounding frequencies, all other factors being equal.

Initial Principal and Regular Contributions

The starting principal (P) and any subsequent regular contributions play a vital role. A larger initial investment naturally provides a larger base for interest to compound upon. Similarly, consistent additions to your principal (e.g., monthly savings deposits into an investment account) continuously inject new money into the compounding engine, further accelerating growth. Combining a solid initial principal with diligent, regular contributions is the most effective strategy for harnessing compound interest. Even small regular contributions, consistently made, can grow into substantial sums over extended periods thanks to the power of compounding.

Strategies to Maximize the Benefits of Compound Interest

Understanding how compound interest works is the first step; actively applying strategies to maximize its benefits is where true wealth building begins.

Start Early, Invest Often

This is perhaps the most critical piece of advice for leveraging compound interest. The “time” variable in the formula is your most valuable asset. The earlier you begin saving and investing, even small amounts, the more time your money has to compound and grow exponentially. Delaying even a few years can result in a significant difference in your long-term wealth, often requiring you to invest substantially more later to catch up. Automate your savings to ensure consistency and minimize the temptation to spend.

Reinvest Earnings Consistently

To truly unleash the power of compounding, you must resist the urge to withdraw your interest or dividends. Reinvesting these earnings means they get added back to your principal, and in turn, start earning interest themselves. Many investment platforms and mutual funds offer automatic dividend reinvestment programs, simplifying this process. This continuous cycle of reinvestment fuels the exponential growth, allowing your portfolio to expand at an accelerating pace.

Consider High-Interest-Bearing Accounts or Investments

While savings accounts offer stability, their interest rates might be low. To maximize compounding, explore investment avenues that offer potentially higher returns, aligning with your risk tolerance. This could include high-yield savings accounts, Certificates of Deposit (CDs) for shorter terms, or a diversified portfolio of stocks, bonds, and mutual funds for long-term growth. Educate yourself on the risks associated with different investment types, but don’t shy away from options that offer better growth potential than traditional low-interest savings.

Understand and Minimize Fees

Fees, whether they are investment management fees, trading commissions, or account maintenance fees, can significantly erode your returns and diminish the effects of compounding. Even seemingly small percentage fees can eat away tens of thousands of dollars from your portfolio over decades. Always read the fine print, understand the fee structures of your accounts and investments, and opt for low-cost alternatives whenever possible (e.g., index funds or ETFs with low expense ratios).

Stay Patient and Consistent

Compound interest is a long-term game. There will be market fluctuations, economic downturns, and periods of slower growth. The key is to stay patient, stick to your investment plan, and continue making regular contributions. Emotional reactions to market volatility often lead to poor financial decisions. Consistency over decades, coupled with the relentless power of compounding, is what ultimately leads to significant wealth accumulation. Trust the process, and let time work its magic.

Conclusion

Computing compound interest is more than just a mathematical exercise; it’s a fundamental understanding that empowers individuals to take control of their financial destiny. By grasping how principal, interest rate, compounding frequency, and time interact, you gain the foresight to plan effectively for your financial goals. Whether you’re starting with a modest sum or a substantial investment, the principles remain the same: start early, contribute consistently, reinvest your earnings, and minimize fees. Embrace compound interest as your most reliable ally on the path to financial independence, and watch your wealth grow in ways that simple arithmetic alone could never achieve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.