In the landscape of personal finance, managing credit is as much about subtraction as it is about addition. While the “Chase Trifecta” or a high-limit Sapphire Reserve card might have served your financial goals three years ago, your current lifestyle, spending habits, or debt management strategy may require a change. Deciding to close a credit card is a significant financial move that requires more than just a phone call; it requires a strategic approach to protect your credit score and preserve your hard-earned rewards.

This guide explores the multifaceted process of closing a Chase credit card, ensuring you navigate the nuances of the “Money” niche—from credit utilization ratios to the intricacies of the Chase Ultimate Rewards ecosystem.

Before You Close: Strategic Financial Considerations

Before you pick up the phone or log into the Chase portal, you must conduct a thorough audit of the card’s place in your financial ecosystem. Closing an account is a permanent action that can have immediate and long-term effects on your credit profile.

Assessing the Impact on Your Credit Score

Your credit score is built on several pillars, two of the most important being the length of credit history and the credit utilization ratio. When you close a Chase account, you are effectively reducing your total available credit. If you carry balances on other cards, your utilization ratio—the percentage of available credit you are using—will increase, which could lead to a dip in your score.

Furthermore, while the account will remain on your credit report for ten years if closed in good standing, you stop the clock on the “age” of that specific line of credit. If the card you are closing is one of your oldest accounts, the long-term impact on your average age of accounts can be detrimental.

Redeeming Your Chase Ultimate Rewards Points

One of the most common mistakes in the “Money” sphere is forfeiting valuable rewards. Chase Ultimate Rewards (UR) points are among the most flexible and valuable digital currencies available. However, if you close your only UR-earning account (such as a Sapphire or Ink card) without moving the points first, those points will vanish.

Before initiating a closure, you should:

- Transfer points to another Chase card you own.

- Transfer points to a travel partner (like United or Hyatt) if you have a premium card.

- Redeem for statement credit or gift cards as a last resort.

Managing Recurring Payments and Outstanding Balances

A “ghost” charge can cause a closed account to go into delinquency. Review your last three months of statements to identify recurring subscriptions—Netflix, gym memberships, or insurance premiums—and move them to a different payment method. Additionally, ensure the balance is zero. While you can close a card with a balance, you will still be responsible for payments and interest, and the process becomes significantly more cumbersome.

The Step-by-Step Process to Closing Your Chase Account

Chase provides several avenues for account closure, ranging from digital self-service to direct human interaction. Each has its own set of pros and cons depending on how much you want to avoid a “retention pitch.”

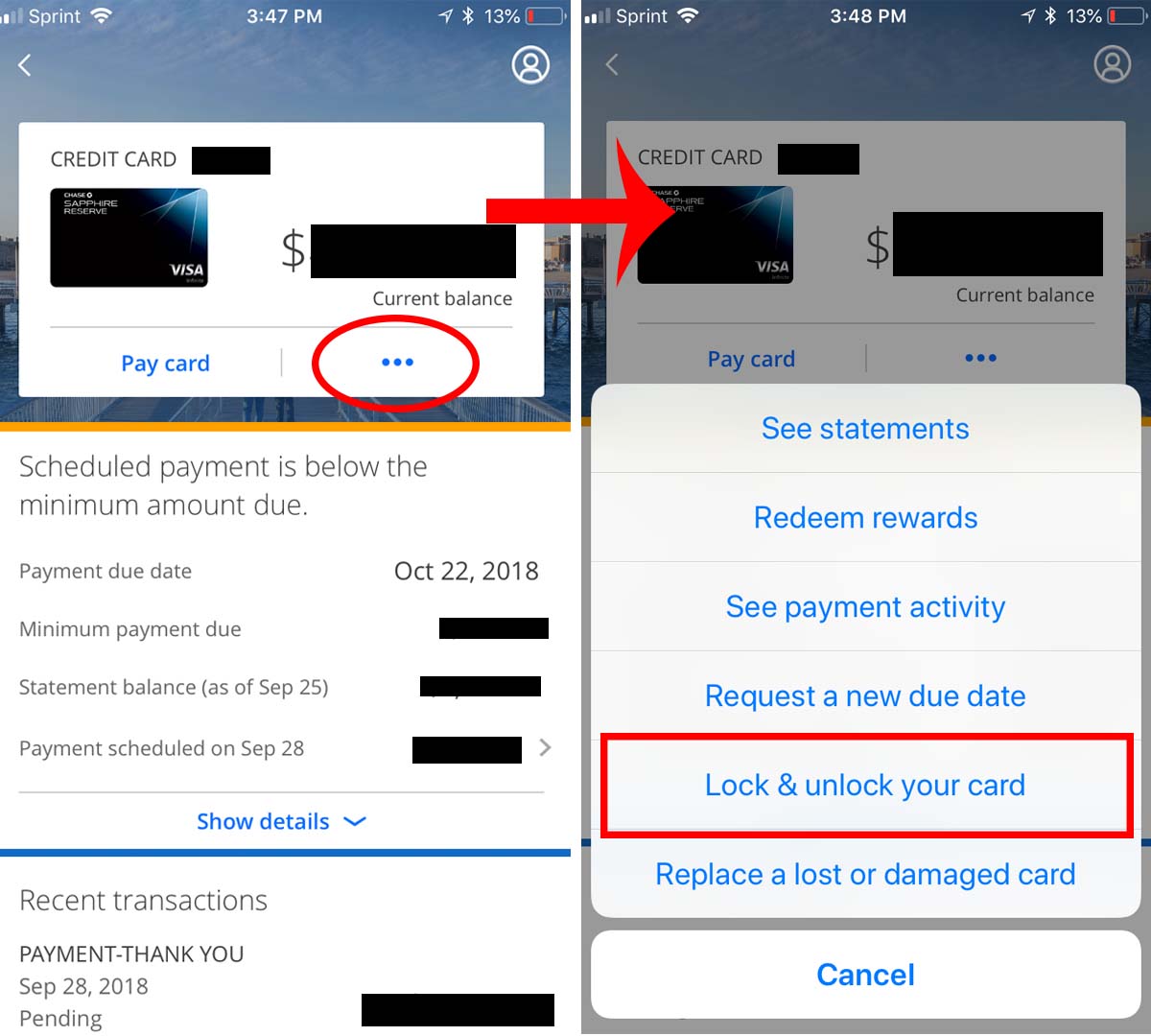

Method 1: Closing via the Chase Mobile App or Website

For those who prefer a paper trail without the pressure of a phone conversation, the Secure Message Center is the most efficient tool.

- Log in to your Chase account online.

- Navigate to the Secure Message Center (found under the “Menu” or “Account Services” tab).

- Select “New Message” and choose the category related to “Account Inquiry” or “Closing an Account.”

- State clearly that you wish to close the specific card (list the last four digits) and confirm that you have already redeemed your rewards.

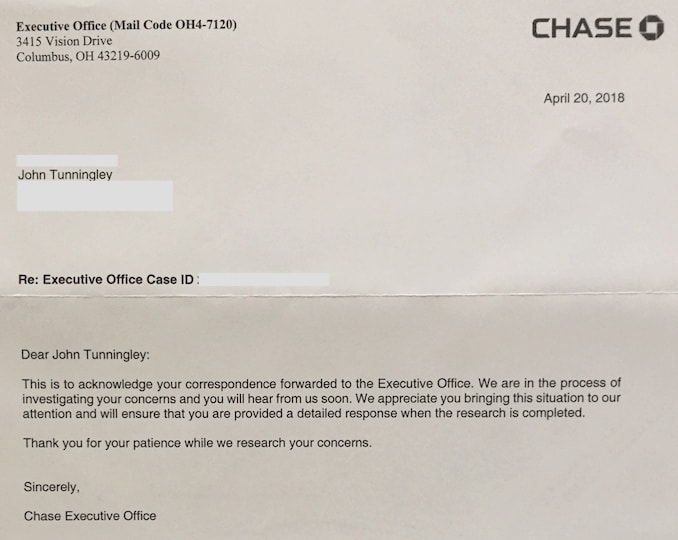

Method 2: Phone Support and the Retention Department

Calling the number on the back of your card is the fastest way to close an account, but it requires you to speak with a representative. This is the traditional route where you will likely be transferred to a “Retention Specialist.” Their job is to keep you as a customer. If you are firm in your decision, simply repeat: “I appreciate the offer, but I would like to close this account for personal financial reasons.”

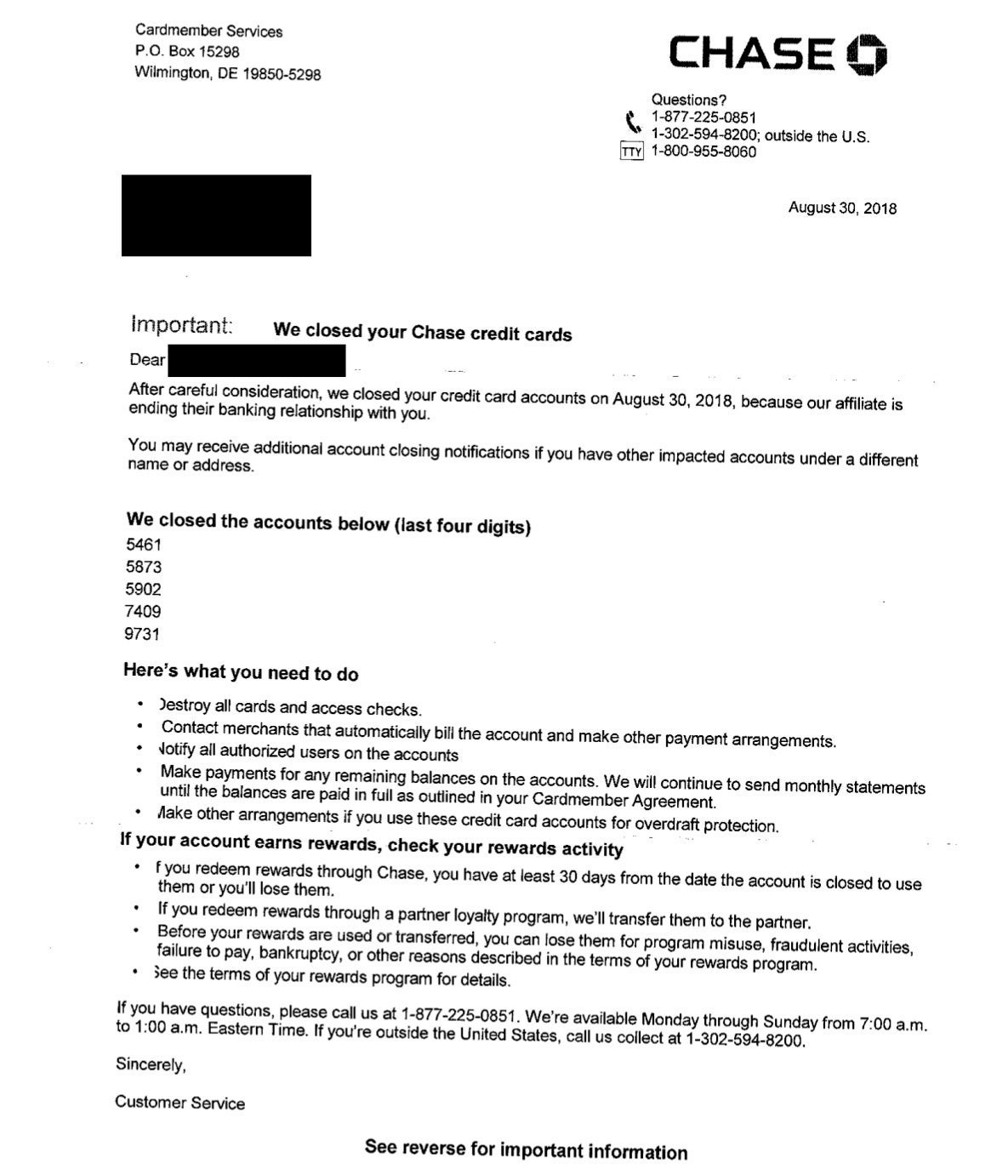

Method 3: Written Request via Mail

While antiquated, sending a certified letter to Chase’s correspondence address is a bulletproof way to ensure your request is documented. This is rarely necessary unless you are dealing with a complex estate matter or a disputed account, but it remains a legal right for consumers.

Navigating the Chase Retention Department

In the world of personal finance, everything is a negotiation. When you call to close a card—especially a premium one with a high annual fee—Chase may try to keep you. Understanding this process can actually result in a “win” for your wallet.

Understanding Retention Offers

A retention offer is an incentive provided by the bank to prevent you from closing your account. This might include:

- A waiver of the annual fee for the current year.

- A “spend-to-get” offer (e.g., “Spend $2,000 in the next three months to receive 20,000 bonus points”).

- A statement credit with no strings attached.

If the only reason you are closing the card is the annual fee, it is worth asking: “Are there any retention offers or fee waivers available on my account at this time?”

When to Stand Your Ground

If the card no longer fits your spending profile—for instance, if you have moved away from a United Airlines hub and no longer need the United Explorer card—a retention offer might just be a distraction. In this case, professional financial management dictates that you should stick to your plan. Do not let a small bonus lure you into keeping an account that complicates your financial life or encourages unnecessary spending.

Post-Closure Steps for Financial Hygiene

The work isn’t finished just because the representative said the account is closed. Professional financial management requires a follow-up to ensure the “ghost of credit past” doesn’t haunt your future reports.

Verifying the Account Status

Wait approximately 30 days and then check your Chase online portal. The account should be listed as “Closed.” It is also wise to download your final 12 months of statements for your personal records, as you may lose digital access to these documents once the account is fully purged from the system.

Safe Physical Disposal of the Card

Most modern Chase cards, particularly the Sapphire and Business Ink series, contain metal. You cannot simply shred these at home with a standard paper shredder. You can either:

- Mail the card back to Chase (they often provide a pre-paid envelope for this).

- Bring it to a local Chase branch for secure destruction.

- Use heavy-duty shears to cut through the chip and the magnetic strip before disposing of the pieces in separate bins.

Monitoring Your Credit Report for Accuracy

Check your credit report (via AnnualCreditReport.com or a monitoring service) about 45 to 60 days after closure. The account should be marked as “Closed by Grantor” or “Closed at Consumer’s Request.” The latter is preferable, though both are generally neutral. If the account still shows as open, you will need to file a dispute with the credit bureaus using your Secure Message confirmation as evidence.

Alternatives to Closing: Downgrading and Product Changes

In many cases, closing a card is actually the wrong financial move. The “Money” niche often highlights the “Product Change” as a superior strategy for long-term credit health.

The Benefits of a Product Change

A product change (or “downgrade”) allows you to swap your current card for a different one within the same “family” of cards without closing the line of credit. For example, if you have a Chase Sapphire Preferred with a $95 annual fee that you no longer want to pay, you can request a downgrade to the Chase Freedom Unlimited, which has a $0 annual fee.

The advantages are significant:

- You keep your credit limit: Your total available credit remains the same, protecting your utilization ratio.

- You keep your account age: The “opened on” date remains the same, protecting your credit history.

- No hard pull: Unlike applying for a new card, a product change does not involve a hard inquiry on your credit report.

Keeping Your Average Age of Accounts Intact

By downgrading to a no-fee card and putting it in a drawer (the “sock drawer strategy”), you allow that account to continue aging and contributing positively to your credit score for decades. This is often the most sophisticated move for a person looking to optimize their financial standing while reducing the “noise” of unwanted annual fees.

Final Thoughts

Closing a Chase credit card is a powerful tool in your financial toolkit, but it must be wielded with precision. Whether you are streamlining your finances to prepare for a mortgage application or simply moving away from a specific rewards ecosystem, following these steps ensures that your “Money” moves are both professional and protected. By considering the impact on your credit, redeeming your rewards, and weighing the benefits of a product change, you transform a simple administrative task into a strategic financial win.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.