Navigating the world of insurance can often feel like a complex financial endeavor. From understanding policy terms to managing premiums, every decision has a direct impact on your personal finances. There are various reasons why an individual might consider canceling an insurance policy – perhaps you’ve found a more competitive rate, your circumstances have changed, or you simply no longer require the coverage. Whatever the motivation, the process of canceling an Allstate policy, or any insurance policy for that matter, is a financial transaction that requires careful attention to detail to ensure a smooth transition and avoid unnecessary financial pitfalls.

This guide will walk you through the financial implications and practical steps involved in canceling your Allstate policy, ensuring you manage this crucial aspect of your personal finance with confidence and clarity. We’ll delve into the financial considerations, outline a step-by-step process, and offer insights into common scenarios to help you make informed decisions that protect your financial well-being.

Understanding Your Allstate Policy and Financial Implications

Before you even initiate the cancellation process, a thorough understanding of your current Allstate policy and its financial terms is paramount. This initial review sets the stage for a financially sound cancellation, helping you anticipate potential costs or refunds.

Reviewing Your Policy Documents for Financial Details

Your Allstate policy documents are not just legal agreements; they are critical financial blueprints. Before making any moves, pull out your policy declaration page, the full policy booklet, and any recent billing statements. Look specifically for sections pertaining to cancellation, refunds, and premium structures.

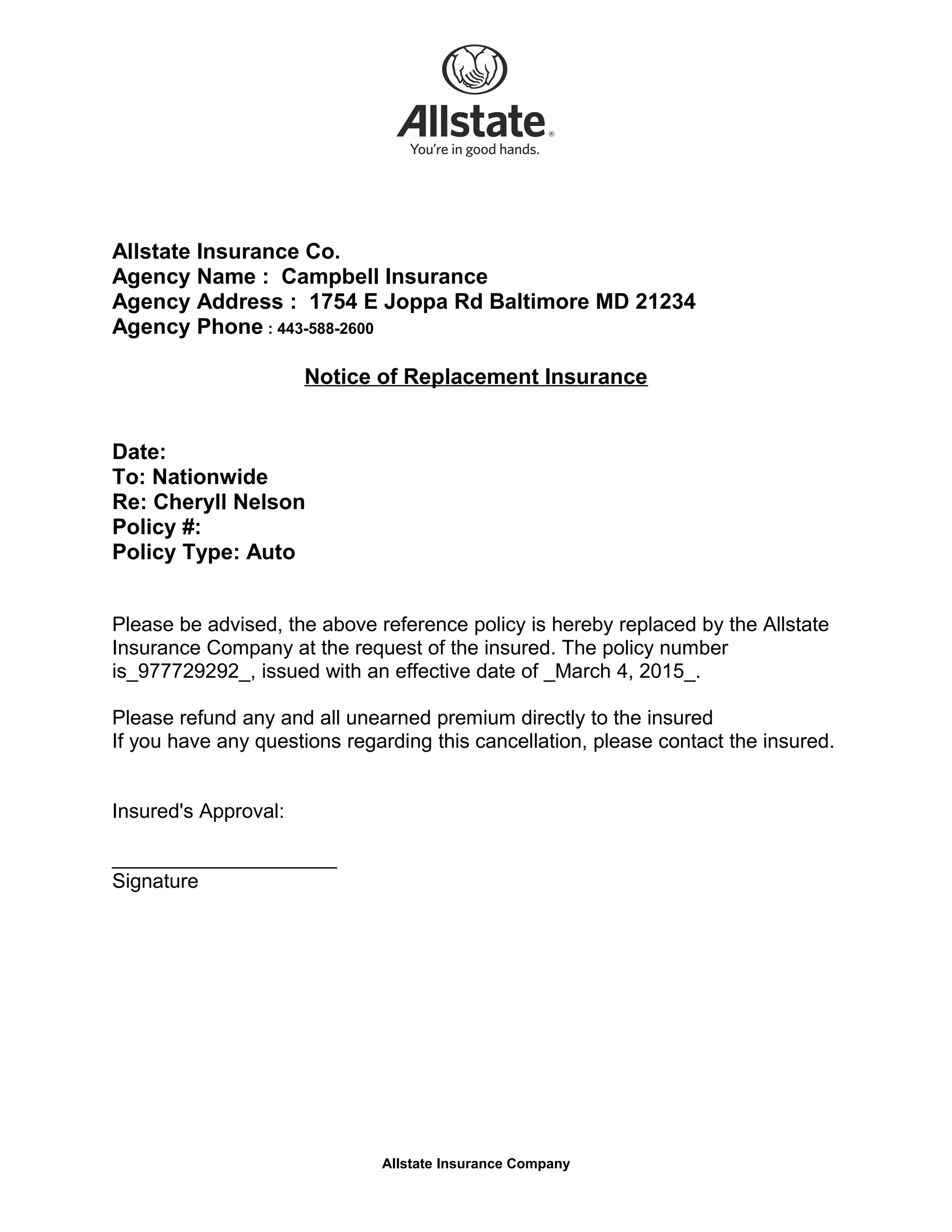

- Cancellation Clause: This section will detail Allstate’s specific procedures for policy termination, including any required notice periods or forms. Crucially, it will also outline any potential fees or penalties for early cancellation, often referred to as a “short-rate penalty.” Understanding these fees beforehand allows you to budget for them or factor them into your decision-making process.

- Premium Structure: Confirm whether your premiums are paid monthly, quarterly, or annually, and if they are paid in advance or arrears. This affects how any prorated refund will be calculated. For instance, if you’ve paid for a full year upfront, you’ll likely be due a refund for the unused portion of the premium.

- Effective Dates: Note the exact start and end dates of your current policy term. This is vital for calculating prorated refunds and ensuring there are no gaps in coverage when you transition to a new policy.

- Auto-Renewal & Payment Terms: Check if your policy is set for automatic renewal and if your payments are automatically debited from your account. You’ll need to explicitly stop these to prevent future charges post-cancellation.

Assessing the Financial Impact of Cancellation

Canceling an insurance policy isn’t just about stopping a payment; it’s a financial decision with several potential outcomes.

- Refunds vs. Additional Charges: The most common financial consideration is whether you will receive a refund or owe additional money. If you cancel mid-term and have paid premiums in advance, you are typically entitled to a prorated refund for the unused portion of your coverage. However, if your policy includes a short-rate penalty, this amount will be deducted from your refund. In some cases, if you have outstanding balances or specific policy conditions, you might even owe Allstate money.

- Lapse in Coverage: A critical financial risk is a lapse in coverage. If you cancel your Allstate policy before a new policy is active, you could face significant financial exposure. For auto insurance, driving without coverage is illegal and can lead to hefty fines, license suspension, and personal liability in an accident. For home insurance, a lapse leaves your property uninsured against damages, a potentially catastrophic financial blow. Always ensure your new policy starts before your old one ends.

- New Policy Costs: When considering cancellation, you are likely doing so because you’re switching to a new insurer or no longer need the specific coverage. Factor in the cost of your new policy. While it might be cheaper, ensure it provides adequate coverage to protect your financial assets. Sometimes, a slightly higher premium is worth the enhanced protection.

Step-by-Step Financial Process for Canceling Your Allstate Policy

Once you’ve done your due diligence and understand the financial implications, the next step is to initiate the cancellation process. Approaching this systematically helps ensure all financial loose ends are tied up.

Preparing Necessary Financial Information

Before contacting Allstate, gather all relevant information. This streamlines the process and ensures you have all details readily available for financial verification.

- Policy Number(s): Have the exact policy number for each Allstate policy you wish to cancel (e.g., auto, home, life).

- Account Holder Information: Your full name, address, phone number, and date of birth as registered with Allstate.

- Effective Cancellation Date: Be clear about the precise date you want your coverage to end. This date will be used for all prorated calculations. It’s highly recommended to align this with the start date of any new policy to prevent financial exposure from coverage gaps.

- Reason for Cancellation: While not always required, having a clear reason can sometimes expedite the process or help customer service provide relevant information regarding potential financial impacts.

- Payment Details: Be ready to confirm your last payment amount and date. This helps reconcile any potential refunds or outstanding balances.

Contacting Allstate for Cancellation: Options and Best Practices

Allstate offers several avenues for policy cancellation. While some methods might be quicker, it’s crucial to choose one that allows for clear communication and documented proof, especially when financial transactions are involved.

- Contacting Your Local Allstate Agent (Recommended for Financial Clarity): If you have a dedicated local agent, this is often the best first point of contact. Agents can provide personalized financial advice regarding your specific policy, calculate potential refunds or fees, and guide you through the precise steps. They can also often help facilitate the cancellation and provide immediate confirmation.

- Calling Allstate Customer Service: You can call Allstate’s general customer service line. Be prepared for a potentially longer wait time. When speaking to a representative, clearly state your intent to cancel and confirm all financial details.

- Best Practice: Always ask for a confirmation number or email verifying your cancellation request. Note down the representative’s name, the date, and time of the call.

- Online Portal/Mobile App (Limited for Cancellation): While Allstate’s online portal and mobile app are great for managing policies and making payments, direct cancellation functionality might be limited for certain policy types or in specific states. You might be able to initiate a request or find forms, but often a direct conversation or written request is still required to finalize.

- Written Request (For Documentation): For absolute financial security and documentation, you can send a written cancellation request via certified mail with a return receipt. This provides irrefutable proof that you initiated the cancellation and on what date. Include all your policy details, the desired cancellation date, and your signature. This method is particularly useful if there are complex financial aspects or if you anticipate any disputes.

Verifying Cancellation and Financial Settlement

The process isn’t over until you have official confirmation and your finances are reconciled.

- Obtain Written Confirmation: Insist on receiving a written confirmation of your policy cancellation from Allstate. This document should state the effective cancellation date and confirm that the policy is no longer active. Keep this with your financial records.

- Monitor for Refund Processing: If you are due a refund, ask about the expected timeframe for processing and delivery. Typically, refunds are issued within a few weeks.

- Check Your Bank Statements: Carefully monitor your bank or credit card statements to ensure that no further premiums are debited after your cancellation date and that any expected refunds are deposited correctly. If you notice any discrepancies, contact Allstate immediately with your confirmation details.

Navigating Common Financial Scenarios When Canceling

Understanding how different scenarios affect your finances during cancellation is crucial for sound financial management.

Cancelling Mid-Term vs. At Renewal: Financial Considerations

The timing of your cancellation can significantly impact the financial outcome.

- Mid-Term Cancellation: If you cancel your policy before its natural expiration date, you are subject to the terms of your policy’s cancellation clause. As mentioned, this often involves a prorated refund (for the unused portion of your premium) minus any short-rate penalty. A short-rate penalty is a fee charged by the insurer for early termination, effectively reducing your refund. This is a crucial financial detail to confirm with Allstate before canceling. For example, if you paid for a year of coverage but cancel after six months, you would typically get back six months’ worth of premiums, minus any applicable fees.

- Cancellation at Renewal: If you choose to cancel at the end of your policy term, often because you’re switching insurers, the financial process is usually simpler. There are typically no short-rate penalties, and your policy simply won’t renew. You just need to ensure you notify Allstate before the renewal date to avoid auto-renewal and subsequent automatic debits. This is the most financially straightforward method of cancellation.

Avoiding Gaps in Coverage: A Financial Prudence Imperative

The financial consequences of a lapse in coverage can be severe. It is absolutely essential to avoid this.

- Overlap Your Policies: The safest financial strategy is to have your new policy effective date precede or be the exact same day as your Allstate policy’s cancellation date. For instance, if your new policy starts on October 1st, set your Allstate cancellation for October 1st. This ensures continuous protection and peace of mind, mitigating financial risk from accidents or unforeseen events during an uninsured period.

- Proof of New Coverage: Some states or financial institutions (like mortgage lenders for home insurance) may require proof of new coverage before allowing you to cancel an existing policy. Have your new policy declaration page ready as evidence.

Dealing with Auto-Renewals and Payment Holds

Modern insurance policies often include auto-renewal clauses to ensure continuous coverage. While convenient, this can complicate cancellation if not managed properly.

- Explicitly Stop Auto-Renewals: When you communicate your intent to cancel, explicitly ask Allstate to ensure that auto-renewal is disabled and that no further automatic payments will be processed.

- Monitor Bank Debits: Even after cancellation confirmation, remain vigilant. Check your bank or credit card statements for at least one to two billing cycles after the cancellation date to ensure no unauthorized debits occur. If they do, contact Allstate immediately and provide your cancellation confirmation. You may need to work with your bank to dispute the charge if Allstate is unresponsive.

Financial Smart Practices Post-Cancellation

The cancellation process doesn’t end with a confirmation email; there are crucial financial practices to implement afterward to protect your interests and optimize your future financial planning.

Documenting Everything for Your Financial Records

Maintaining meticulous records is a cornerstone of responsible financial management.

- Keep a Dedicated File: Create a physical or digital file for your canceled Allstate policy. This file should contain:

- Your original policy documents.

- All correspondence related to the cancellation (emails, letters, call notes).

- The official cancellation confirmation from Allstate.

- Evidence of any refunds received (bank statements, copies of checks).

- Any new policy documents from your new insurer.

- Importance of Records: These records serve as proof of your actions in case of any future disputes, billing errors, or audits. They are invaluable for confirming dates, amounts, and agreements, protecting you from potential financial liabilities.

Reinvesting or Reallocating Refunded Premiums

If you receive a refund, consider how you can best utilize these funds within your overall financial strategy.

- Emergency Fund: If you don’t have a fully funded emergency savings account, directing your refund there is a financially prudent move.

- Debt Reduction: Use the refund to pay down high-interest debt, such as credit card balances, to improve your overall financial health.

- Savings/Investments: If your emergency fund is healthy and debt is under control, consider putting the money into a savings account or investment vehicle to grow your wealth.

- Offsetting New Policy Costs: If your new policy is more expensive, the refund can help offset the initial premium increase, easing the financial transition.

Evaluating Future Insurance Needs and Budgeting

Canceling a policy provides an opportunity to reassess your overall insurance portfolio and how it fits into your long-term financial planning.

- Regular Reviews: Make it a habit to review all your insurance policies annually. Your life circumstances (marriage, children, new home, career changes) evolve, and your insurance needs should evolve with them.

- Budgeting for Premiums: Ensure that your new insurance premiums fit comfortably within your monthly or annual budget. Insurance is a recurring expense, and proper budgeting prevents financial strain.

- Comparison Shopping: Don’t hesitate to compare quotes from multiple providers regularly. The insurance market is competitive, and loyalty discounts from one insurer might not always outweigh better rates and coverage from another. Utilize online comparison tools and speak with independent agents who can shop around for you.

- Bundling Opportunities: Explore bundling options with your new insurer (e.g., auto and home insurance with the same company) as this can often lead to significant financial savings.

Canceling an Allstate policy, or any insurance policy, is more than just an administrative task; it’s a financial decision that requires careful consideration and meticulous execution. By understanding your policy’s financial terms, following a structured cancellation process, and diligently managing post-cancellation finances, you can navigate this transition smoothly and confidently. This proactive approach ensures you maintain continuous coverage, avoid unnecessary costs, and ultimately safeguard your financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.