In the journey of personal financial management, the tools we use must evolve alongside our goals. There comes a time for many cardholders when a specific piece of plastic—or metal—no longer serves its purpose. Whether you are looking to trim annual fees, consolidate your debt, or simplify your financial life, knowing how to cancel a Chase credit card effectively is a vital skill in modern money management.

Chase is one of the largest credit card issuers in the world, offering everything from the premium Sapphire line to the accessible Freedom cards. However, closing an account with a major institution requires more than just a phone call; it requires a strategic approach to protect your credit score and preserve your earned rewards. This guide explores the “Money” niche of credit management, detailing the technical steps and the financial implications of closing a Chase account.

Essential Pre-Cancellation Checklist: Protecting Your Assets

Before you initiate the cancellation process, you must conduct a thorough audit of your account. Closing a card prematurely can result in the loss of valuable assets and create unnecessary administrative hurdles.

Redeeming Your Chase Ultimate Rewards

The most significant risk when canceling a Chase card is the potential loss of Ultimate Rewards (UR) points. If you have a balance of points on the card you intend to close, you must move or use them before the account is shuttered.

- Transfer to Another Chase Card: If you have another Chase card that earns UR points (like the Chase Freedom Flex or another Sapphire card), you can “Combine Points” via the Chase portal.

- Transfer to Travel Partners: If you hold a Sapphire Preferred, Sapphire Reserve, or Ink Business Preferred, transfer your points to airline or hotel partners like United, Southwest, or Hyatt.

- Cash Back or Gift Cards: If you do not have another Chase card, redeem your points for a statement credit or gift cards to ensure you don’t leave money on the table.

Managing Outstanding Balances and Interest

You cannot effectively close a card if it has a pending balance—at least not without complications. Ideally, your balance should be zero. If you carry a balance, the interest will continue to accrue even after the account is “closed” to new purchases, which can lead to missed payments if you aren’t monitoring the account. If you are struggling with high interest, consider a balance transfer to a 0% APR card before initiating the cancellation.

Updating Automated Payments and Subscriptions

In our digital economy, many of us have “set and forget” subscriptions. Audit your last three months of statements for recurring charges like Netflix, insurance premiums, or gym memberships. If a merchant attempts to charge a canceled card, they may trigger a late fee or a service interruption. Move these payments to a different financial instrument at least one billing cycle before you cancel the Chase card.

The Step-by-Step Methods for Closing Your Chase Account

Chase provides several avenues for account closure, ranging from traditional phone calls to digital messaging. Choosing the right method depends on your preference for a paper trail versus immediate confirmation.

Canceling via Phone: The Human Touch

The most common method is calling the number on the back of your card or Chase’s general customer service line (1-800-432-3117).

- The Script: Be firm but polite. When the automated system asks why you are calling, say “cancel credit card.”

- The Retention Office: You will likely be transferred to a retention specialist. Their job is to keep you as a customer. They may offer to waive an annual fee or provide bonus points to keep the account open. If your goal is purely financial simplification, decline these offers and reiterate your desire to close the account.

- The Confirmation: Always ask for a confirmation number and the name of the representative you spoke with.

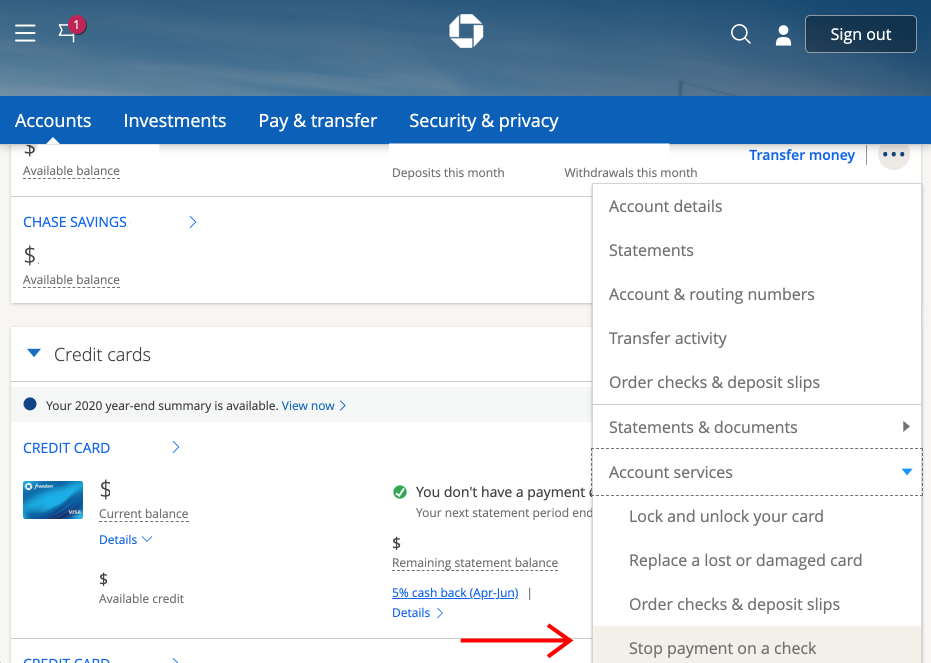

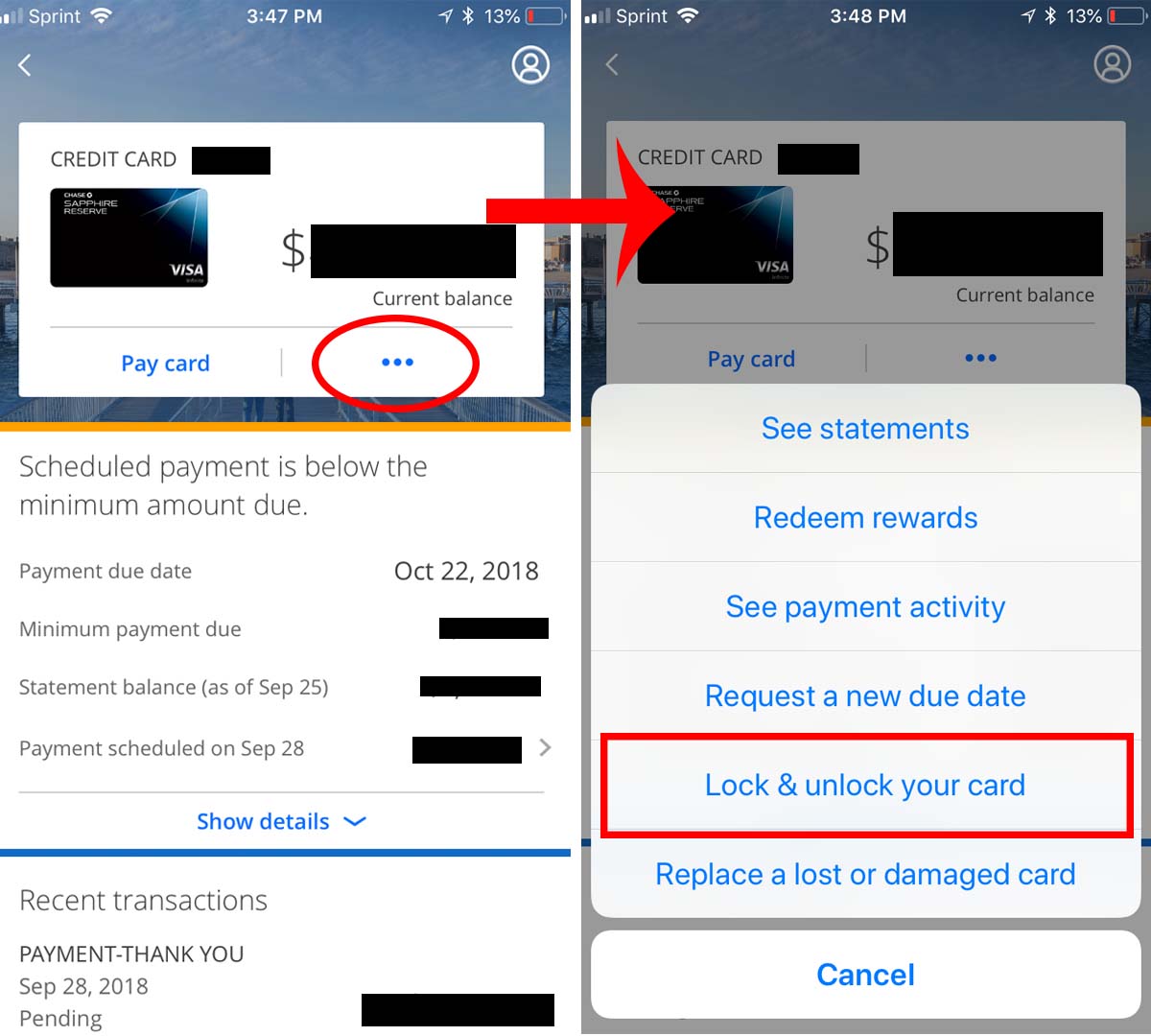

Using the Secure Message Center: The Digital Paper Trail

For those who prefer to avoid the “hard sell” of a retention specialist, the Chase Secure Message Center is an excellent tool.

- Log in to your Chase online banking portal.

- Navigate to the “Secure Message Center.”

- Compose a new message selecting the specific credit card account.

- State clearly that you wish to close the account and that you have already redeemed your rewards.

- Chase will typically respond within 24–48 hours confirming the closure. This provides a written record of your request.

Writing a Formal Cancellation Letter

While less common today, sending a certified letter to Chase’s correspondence address is the most formal way to close an account. This is often reserved for complex business accounts or individuals who want an absolute paper trail for legal or credit-repair reasons. Include your name, address, and the last four digits of the card number (never the full number).

Analyzing the Impact on Your Credit Score and Financial Profile

From a “Money” perspective, the decision to close a credit card isn’t just about the card itself; it’s about the health of your credit report. Closing an account can impact your FICO score in two primary ways.

The Credit Utilization Ratio

Your credit utilization ratio—the amount of credit you are using compared to your total available credit—accounts for 30% of your credit score. When you cancel a Chase card, you are reducing your total available credit. If you have balances on other cards, your utilization percentage will spike, which can cause your credit score to drop.

- Strategy: If the card you are closing has a high limit (e.g., $10,000), ensure your other balances are paid down to near zero to offset the loss of that “buffer.”

The Average Age of Accounts (AAoA)

Length of credit history accounts for 15% of your score. While a closed account in good standing will remain on your credit report for ten years, it eventually falls off. If the Chase card you are closing is your oldest account, its eventual removal could shorten your credit history significantly. For this reason, many financial advisors suggest keeping your oldest, no-fee cards open indefinitely.

Hard Inquiries and Future Applications

If you are canceling a card to make room for a new one, be mindful of the “Chase 5/24 Rule.” This is an unofficial but widely recognized policy where Chase will deny you for a new card if you have opened five or more accounts with any issuer in the past 24 months. Closing a card does not “reset” this count, so plan your applications and cancellations with a long-term timeline in mind.

Strategic Alternatives: Is Closing the Account Your Best Move?

Before you pull the trigger on a cancellation, consider if there is a more efficient way to achieve your financial goal without harming your credit profile.

The “Product Change” Strategy (Downgrading)

If your primary reason for canceling is a high annual fee (such as the $550 on the Sapphire Reserve), consider a “product change.” You can request to downgrade the card to a no-fee version, like the Chase Freedom Unlimited.

- Benefits: You keep your credit line open (helping your utilization), you maintain the account’s age (helping your AAoA), and you avoid the annual fee.

Negotiating for a Retention Offer

Sometimes, the most profitable move is to stay. If you call to cancel, the retention agent might offer a “statement credit” that covers the annual fee or a “spend challenge” for bonus points. If the value of the offer exceeds the cost of the annual fee, it may be financially prudent to keep the card for another year and reassess later.

Post-Cancellation Best Practices

Once the account is officially closed, your financial responsibilities do not end immediately.

Confirming the Account Status

Within 30 days of cancellation, check your credit report (via a free service or AnnualCreditReport.com) to ensure the account is listed as “Closed by Consumer.” This distinction is important; it looks better to future lenders than “Closed by Grantor,” which can imply the bank shut you down for mismanagement.

Physical Disposal of the Card

Modern credit cards, especially the premium Chase Sapphire and United Quest cards, are often made of metal. These cannot be easily shredded in a standard home shredder. You can either return the card to a local Chase branch for secure disposal or request a prepaid envelope from Chase to mail the card back for destruction. If you have a plastic card, use a cross-cut shredder or heavy-duty scissors to destroy the chip and the magnetic strip.

Final Statement Review

Even after a card is closed, keep an eye on your online login for one final billing cycle. Ensure that no “zombie” subscriptions have posted and that your final balance is indeed $0.00.

In the world of personal finance, your credit portfolio should be lean and effective. By following these steps to cancel your Chase credit card, you ensure that you are making a move that benefits your long-term financial health while avoiding the common pitfalls of lost rewards and credit score dips. Whether you are pivoting to a new rewards ecosystem or simply practicing financial minimalism, a calculated cancellation is a sign of a sophisticated and proactive money manager.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.